Initial listing requirements are the gatekeepers of the public markets. They calibrate who may access exchange‑based liquidity by aligning financial strength, shareholder distribution, and governance maturity with the expectations of institutional and retail investors. Although every issuer’s profile is unique, the logic of these standards is consistent: prove durability, prove breadth of ownership, and prove the capacity to operate as a public company from day one.

This article explains how companies can translate financial statements, capitalization plans, and board composition into an executable path to the NYSE or Nasdaq.

Because pricing and offering mechanics influence many tests, the listing plan should be built into the transaction model—well before a registration statement is filed with the SEC. A practical plan links corporate governance build‑out, distribution strategy, and auditing timelines to the expected market tier, and it anticipates where a company will most credibly meet the standard: via income, cash flow, stockholders’ equity, or market value of publicly held shares. Issuers that have progressed through alternative routes to market should resist the temptation to rely on bare minimums; building buffers above thresholds is the simplest way to avoid deficiency notices in the first quarters after listing.

Financial Yardsticks and How to Choose Among Them

Most issuers can qualify under more than one quantitative path. A late‑stage software company with high gross margins but modest current‑period income may favor a market‑value‑of‑publicly‑held‑shares test; a profitable specialty manufacturer may fit better under an earnings or cash‑flow test. The offer size, price range, and overallotment determine where the issuer lands—and small adjustments to the float can be the difference between meeting or missing a tier.

Working examples help: imagine a company that targets a $18–$22 range and needs to ensure it clears the minimum bid price with room to spare. If the market weakens into pricing, it can either right‑size the deal (reduce shares and lean on secondary liquidity post‑listing) or adjust proceeds with a parallel debt facility. Either way, the CFO should run sensitivity tables that preserve compliance across multiple scenarios.

Distribution, Liquidity, and Why It’s Operational (Not Just Legal)

Distribution tests measure whether an issuer’s shareholder base is broad enough to sustain two‑sided trading. Minimums for round‑lot holders and publicly held shares are designed to prevent illiquidity and excessive concentration. These thresholds are operational because they depend on transfer‑agent records, broker acceptance, and investor‑relations outreach—workstreams that require months of preparation.

Teams coming from private markets or alternative trading venues frequently underestimate this step. Building a compliant float means structuring investor communications that convert interest into eligible holders while preserving long‑term alignment.

Governance and the ‘Public Company Operating System’

Exchanges expect a majority‑independent board, fully chartered committees, and a compensation framework capable of weathering public scrutiny. Disclosure controls and procedures must function in parallel with internal control over financial reporting. Director and officer biographies should reflect depth and independence, and related‑party transaction policies should be tested against real scenarios. For drafting discipline around leadership disclosures, many issuers revisit officer and director disclosure principles to ensure biographies, independence determinations, and committee assignments are fully supported.

Documentation, Calendaring, and Transaction Mechanics

Listing applications run alongside registration on Form S‑1 (or F‑1 for foreign private issuers). The critical path is calendar management: synchronize audit completion, pro forma builds, and board appointments so that no financial statement goes stale during review. If shareholder approval is necessary for equity issuance thresholds or corporate charter changes, align proxy timelines with the listing window. And where approval isn’t required, information statements still demand precision in timing and notice.

Issuers evaluating capital‑raising alternatives sometimes compare traditional underwriting to other paths. Thoughtful teams map the trade‑offs in advance, including how those choices affect listing eligibility and investor expectations.

Reporting Readiness from Day One

Initial listing is not the finish line; it is the starting line for sustained compliance. Management teams should rehearse disclosure cycles for 8‑Ks, 10‑Qs, and 10‑Ks, and pressure‑test close calendars against headcount and systems. Consistent guidance policies and investor‑relations materials reduce the risk of selective disclosure. A concise refresher on periodic obligations remains invaluable to new public companies.

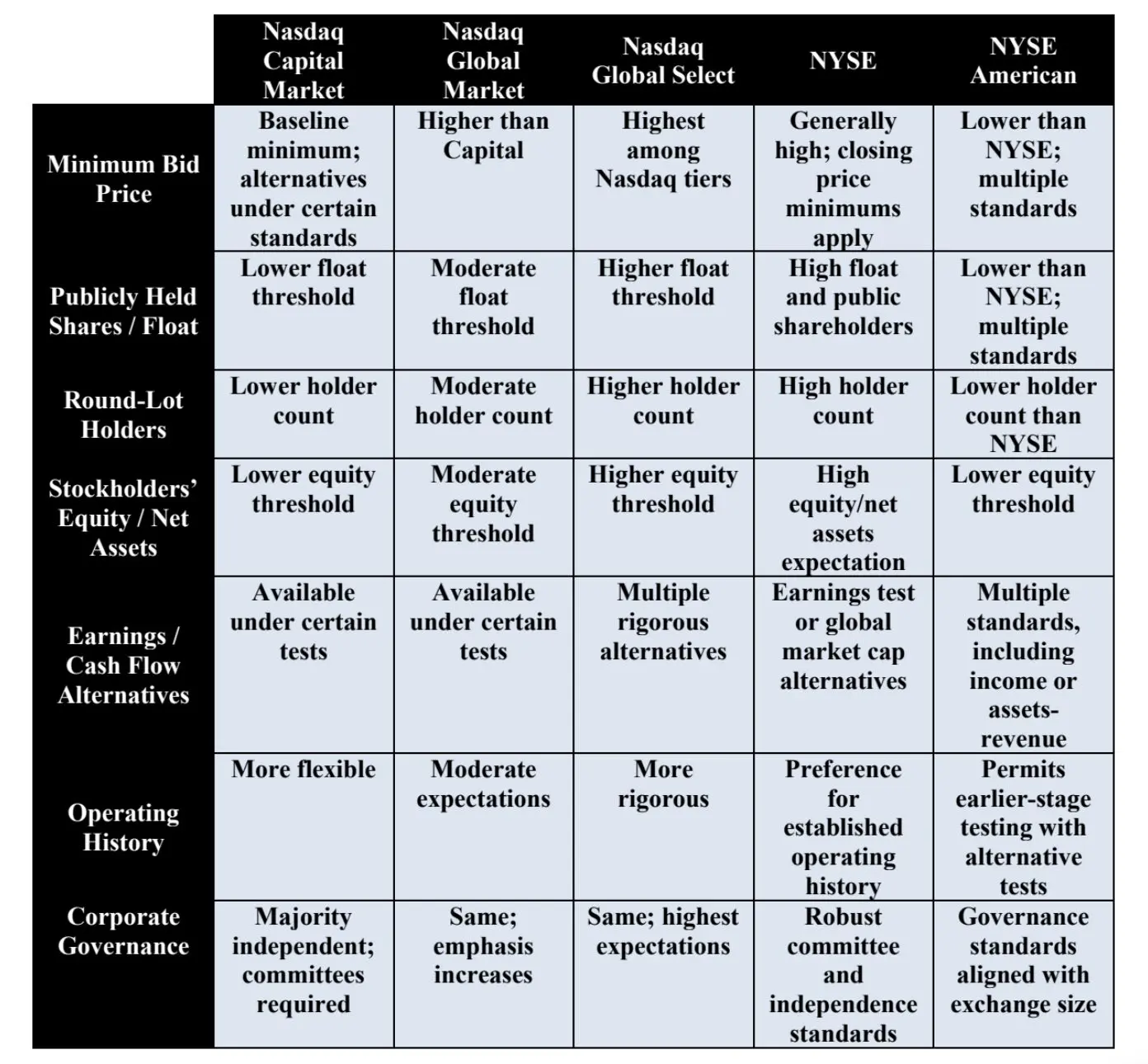

Comparison Chart: Initial Listing Requirements by Exchange/Tier

The table below summarizes the core dimensions that exchanges evaluate at initial listing. Specific numeric thresholds can change; issuers should validate current figures against official exchange materials when finalizing a filing and pricing plan.

Putting It All Together: A Listing Readiness Playbook

- Start with a sober assessment of financials across multiple standards, then overlay realistic assumptions about pricing and demand.

- Draft governance documents and board committee charters before the filing goes live, and recruit independent directors early enough to onboard them into audit readiness.

- Inventory every related‑party arrangement and resolve gray areas while there is time to restructure or disclose fully.

- Conduct a dry‑run close to test how quickly the finance team can move from operations to reporting.

- Coordinate the transfer agent, underwriters (or placement agents), and the IR firm on distribution and communications.

- Above all, treat listing as a systems challenge—people, process, and data—not a discrete legal filing.

Conclusion

Navigating the initial listing requirements for Nasdaq or NYSE demands meticulous preparation and strategic foresight. By aligning financial metrics, shareholder distributions, and governance practices with exchange standards, companies can not only achieve a successful listing but also lay a strong foundation for long-term success in the public market. Ultimately, viewing this process as an opportunity to enhance operational resilience will better position issuers to thrive amid investor scrutiny and market volatility.

If you have any questions about taking your company public on the Nasdaq or NYSE or would like to speak to a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets. Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com