President Donald Trump has revived an idea he first floated during his earlier administration: doing away with quarterly reporting requirements for U.S. public companies. This move aligns with President Trump’s vision of reducing bureaucratic hurdles and fostering a business environment that prioritizes innovation and growth.

Quarterly Filings? Boring! We’ll Do Reporting Like the Smart Foreigners

Under the proposal, companies would no longer need to file Form 10-Q every three months. Instead, they would be required to submit an annual report (Form 10-K) and a semi-annual report, similar to what foreign private issuers file when they use Forms 20-F or 6-K, which would align U.S. reporting requirements with established international practices. For example, in the United Kingdom, the Financial Conduct Authority (FCA) requires listed companies to publish half-yearly financial reports within three months of the period end, consisting of condensed financial statements, an interim management report, and responsibility statements. Similarly, the European Union’s Transparency Directive allows member states to require only semi-annual reporting, though some countries maintain quarterly requirements. Australia and New Zealand also operate under a semi-annual reporting framework.

Under the proposal, companies would no longer need to file Form 10-Q every three months. Instead, they would be required to submit an annual report (Form 10-K) and a semi-annual report, similar to what foreign private issuers file when they use Forms 20-F or 6-K, which would align U.S. reporting requirements with established international practices. For example, in the United Kingdom, the Financial Conduct Authority (FCA) requires listed companies to publish half-yearly financial reports within three months of the period end, consisting of condensed financial statements, an interim management report, and responsibility statements. Similarly, the European Union’s Transparency Directive allows member states to require only semi-annual reporting, though some countries maintain quarterly requirements. Australia and New Zealand also operate under a semi-annual reporting framework.

Quarterly Reports? Total Disaster! Semi-Annual is Tremendous

The push for this change comes from long-standing concerns among business leaders and policymakers that quarterly reporting encourages “short-termism.” Executives often face intense pressure to hit earnings targets every three months, which some argue leads to cost-cutting, underinvestment in innovation, and strategies that prioritize short-term stock performance over long-term value creation. By reducing the frequency of required financial reports, Trump and his supporters argue, companies could focus more on sustainable growth and less on the relentless quarterly cycle. Critics, however, warn that fewer reports could mean less transparency and greater risk for investors.

The push for this change comes from long-standing concerns among business leaders and policymakers that quarterly reporting encourages “short-termism.” Executives often face intense pressure to hit earnings targets every three months, which some argue leads to cost-cutting, underinvestment in innovation, and strategies that prioritize short-term stock performance over long-term value creation. By reducing the frequency of required financial reports, Trump and his supporters argue, companies could focus more on sustainable growth and less on the relentless quarterly cycle. Critics, however, warn that fewer reports could mean less transparency and greater risk for investors.

Saving Companies YUGE Time and Money: The End of the 10-Q Hoax

Trump has proposed that U.S. public companies no longer be required to file quarterly financial reports (10‑Qs) with the SEC; instead, companies would report only semi‑annually (every six months). Under the proposal, issuers would still be required to file an annual report (Form 10‑K) and a semi‑annual report (similar to the model used by foreign private issuers filing Form 20‑F or 6‑K). Additionally, companies would still be required to file Form 8-Ks to report material events in a timely manner. This means that while the cadence of regular financial reporting would be reduced, the obligation to disclose significant corporate events would remain in place.

Trump argues that this would save money and free up management to focus more on running their businesses rather than chasing short‑term quarterly performance metrics.

Investors Will Love It. The Best Reporting Schedule Ever. Everyone Says So

If 10‑Qs are reduced or removed, a lot of attention falls on other disclosure tools—especially Form 8‑K. Here’s a refresher on how 8‑K works and what it requires.

If 10‑Qs are reduced or removed, a lot of attention falls on other disclosure tools—especially Form 8‑K. Here’s a refresher on how 8‑K works and what it requires.

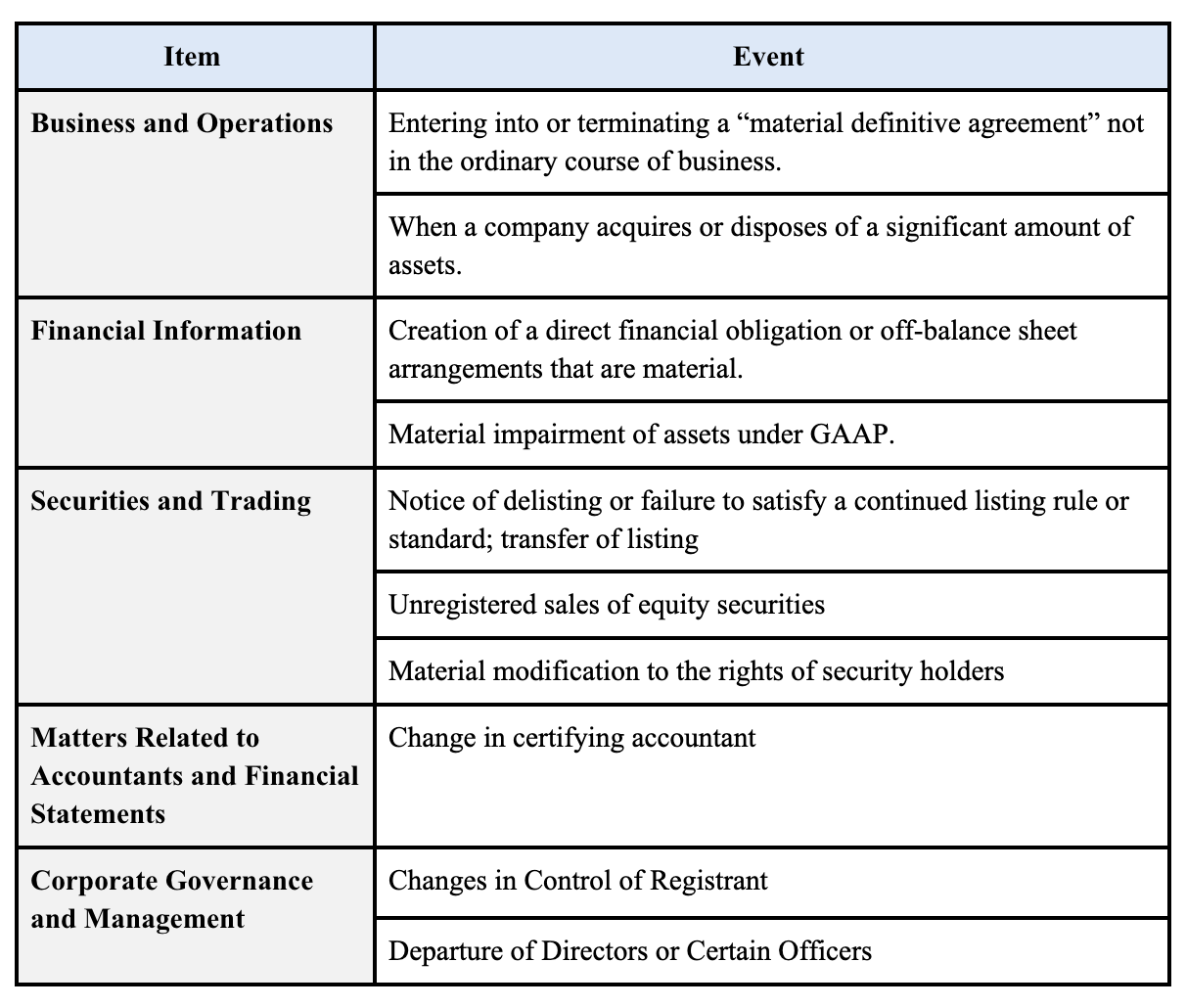

What is an 8K

- Form 8‑K is the “current report” that public companies file with the SEC to disclose material events (major corporate events or occurrences) that shareholders and the public should know about on a timely basis.

- It is not a periodic financial statement like the 10‑Q or 10‑K. Instead, it reports triggering events such as acquisitions, changes in control, changes in directors or auditors, bankruptcy, material agreements, and material obligations, among others.

Timing and Triggering Events

Most 8‑K items must be filed within four business days of the occurrence of a triggering event. Some of the main “Triggering events” include:

There are also some special rules for exhibits or financial statements under certain items (for example, for acquisitions or dispositions, or when acquiring businesses), which may require pro forma financials or updated audited statements.

If quarterly reporting is replaced with semiannual reporting, Form 8-K filings would likely need to play a more significant role, with investors relying more on 8-Ks to provide updates between less frequent periodic reports.

Limitations of 8‑K

- 8‑K does not provide regular, detailed interim financial updates like the 10‑Q does (revenues, income, cash flow, balance sheet changes, etc, every quarter). It only covers events that are material and meet the triggering criteria.

- Because events may not occur evenly, there may be long stretches without any 8‑K disclosures that cover business performance.

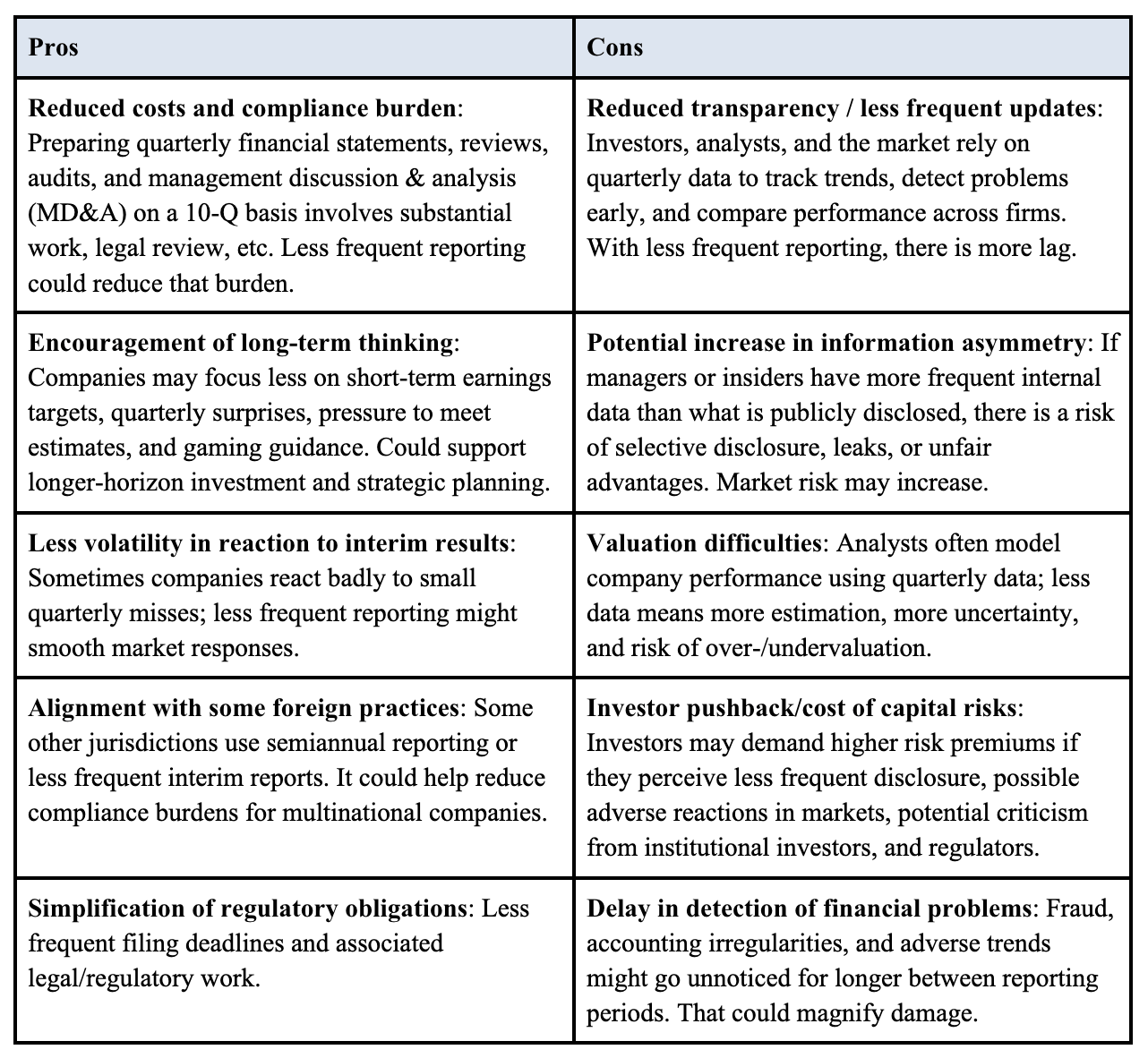

Pros and Cons

Here are arguments for and against doing away with mandatory 10‑Qs:

Legal / Practical Hurdles

To eliminate or reduce the 10‑Q requirement would require changes to SEC rules. That means rulemaking: drafting a proposed rule, public comment, possibly judicial review, etc. You can’t simply change by executive order — though the executive branch can direct the SEC to propose changes.

Companies may need to adjust internal systems (financial reporting, forecasting, investor relations) to accommodate the change.

Some investors, rating agencies, and lenders may experience a reduced frequency of unfavorable reporting.

Conclusion

Trump’s proposal to end mandatory quarterly 10-Q filings in favor of semiannual reporting would represent a significant shift in financial disclosures in the U.S. It would likely reduce costs and administrative burdens for companies, while encouraging a longer-term strategic focus among management, but at the price of less frequent information for investors and possibly a greater risk of information gaps or asymmetry.

If you have questions about SEC reporting requirements or would like to speak with a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets. Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com