For many emerging public companies, the OTC Markets represent the first rung on the ladder toward accessing institutional capital. But for issuers seeking broader exposure, deeper liquidity, and valuation credibility, the ultimate objective is an uplisting to a national securities exchange — the Nasdaq Stock Market (Nasdaq) or the New York Stock Exchange (NYSE).

The uplisting process involves far more than meeting a checklist of numerical requirements. It demands strategic planning, corporate governance reform, enhanced financial reporting, and proactive regulatory engagement with the SEC, FINRA, and the target exchange.

An uplisting can be transformative — but only for companies prepared to meet the heightened expectations of the public markets.

Why Uplisting Matters

Remaining on the OTC Markets can limit growth and investor access. The OTC system provides liquidity, but its investor base is largely retail. Institutional investors, index funds, and many investment banks are restricted by policy or regulation from trading OTC securities.

Uplisting delivers:

- Institutional credibility — attracting analysts, underwriters, and long-term investors;

- Enhanced liquidity and market depth;

- Higher valuation multiples and improved perception of stability;

- Eligibility for inclusion in ETFs and market indices; and

- Expanded access to follow-on offerings and PIPE financings under Form S-3 eligibility.

For many companies, uplisting marks the transition from a speculative microcap to a sustainable public enterprise.

Planning the Uplisting: Readiness Assessment

A successful uplisting begins long before an exchange application is filed. We encourage issuers to begin a readiness assessment at least 12 months in advance.

Financial and Capital Structure Review

Issuers must provide audited financial statements prepared by a PCAOB-registered accounting firm. The exchange will scrutinize consistency, audit quality, and any “going concern” opinions.

Companies must also evaluate:

- Equity capitalization (convertible notes and warrants often create dilution issues);

- Public float concentration;

- Bid-price stability; and

- Operating revenue growth sufficient to meet listing thresholds.

Issuers with complex capital structures may need to complete reverse stock splits, retire toxic convertible debt, or restructure outstanding preferred shares to meet quantitative criteria.

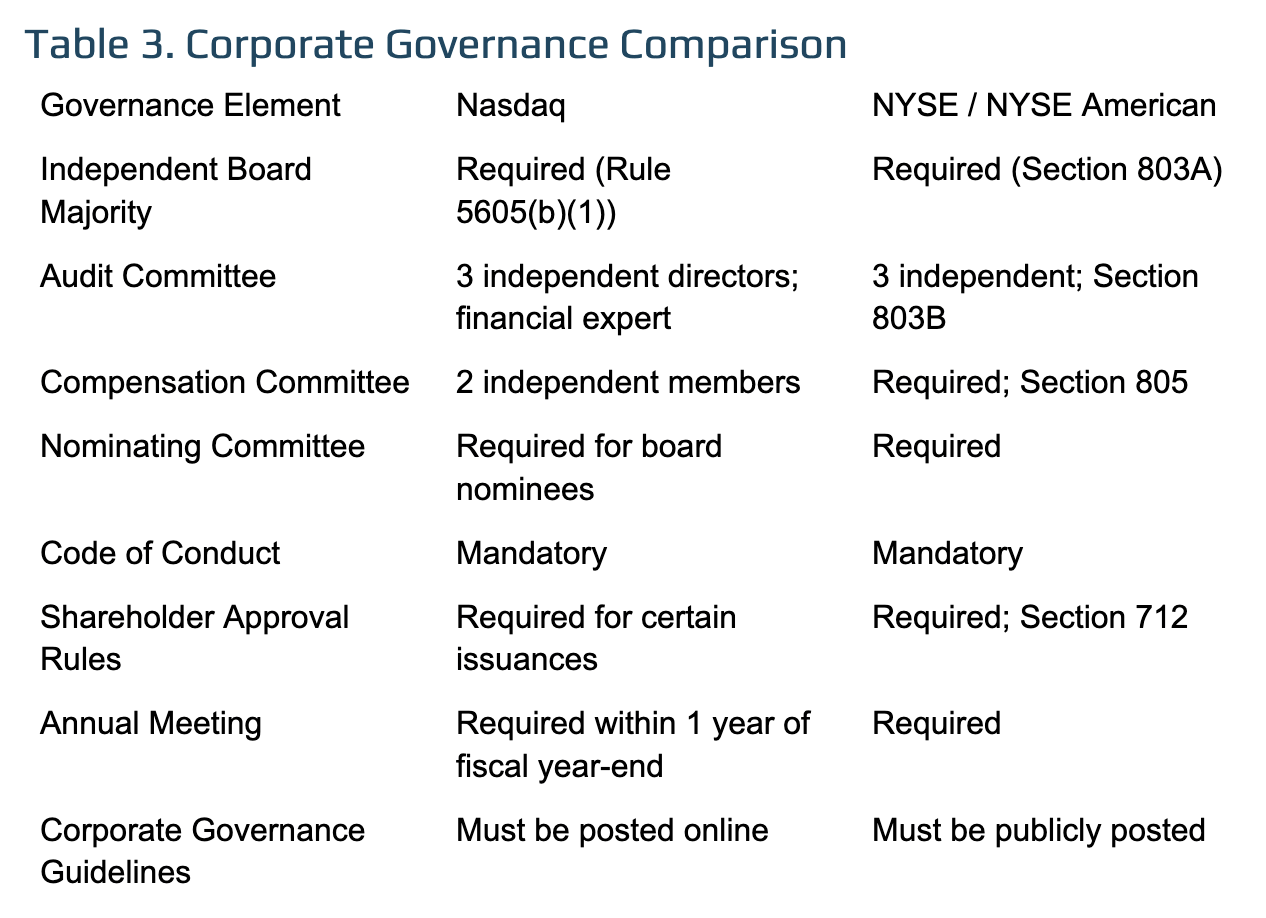

Governance and Board Composition

Nasdaq and NYSE both require a majority-independent board, an audit committee of independent directors, and functioning compensation and nominating committees.

Companies transitioning from OTCQX or OTCQB should start recruiting experienced independent directors early, ideally with expertise in audit, finance, and industry.

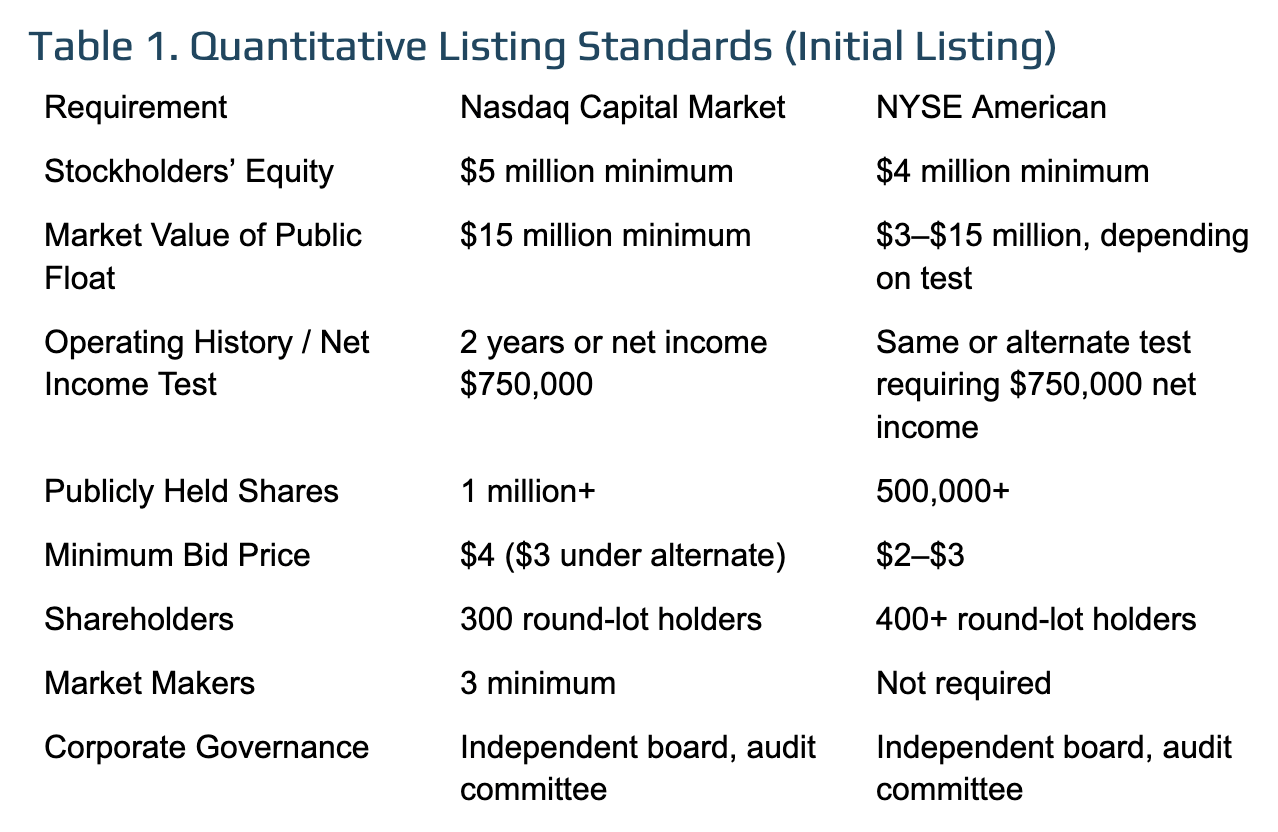

Quantitative Listing Standards

While exact requirements differ between exchanges, issuers typically qualify under one of three financial standards:

| Requirement | Nasdaq Capital Market | NYSE American |

|---|---|---|

| Stockholders’ Equity | $5 million minimum | $4 million minimum |

| Publicly Held Shares | 1 million+ | 500,000+ |

| Market Value of Public Float | $15 million minimum | $3–15 million, depending on test |

| Bid Price | $4 per share ($3 under alternate) | $2–$3 per share |

| Shareholders | 300 round-lot holders | 400+ round-lot holders |

| Market Makers | 3 minimum | Not required |

Detailed comparison: Nasdaq Listing Requirements

Issuers must meet at least one of the applicable standards and demonstrate a sustainable business plan and public-interest suitability.

Qualitative Standards and “Public Interest” Review

Quantitative compliance alone is not enough. Both Nasdaq and NYSE apply discretionary review powers under their public interest authority — a critical step that surprises many OTC issuers.

Nasdaq Rule 5101 and NYSE Section 802.01D authorize exchanges to deny or suspend listings if:

- The issuer or its management has a regulatory history;

- The company engaged in misleading promotions or manipulative trading;

- There are unresolved SEC or FINRA enforcement matters; or

- Corporate governance is inadequate to protect investors.

At Hamilton & Associates, we emphasize proactive disclosure of any prior securities issues, late filings, or enforcement inquiries. Early transparency allows issuers to demonstrate remediation — a key factor in public-interest determinations.

Preparing for Application: The Corporate Cleanup

Issuers should anticipate a comprehensive legal and financial audit of their corporate history before uplisting.

Typical cleanup actions include:

- Reverse stock split to meet minimum bid price;

- Amendment of Articles and Bylaws to conform with exchange governance requirements;

- Resignation of legacy insiders or promoters who may raise reputational concerns;

- Consolidation of share classes and elimination of preferred rights inconsistent with exchange rules;

- Retention of independent transfer agent and PCAOB-registered audit firm.

These steps send a clear message to regulators and investors that the company is serious about compliance and transparency.

Filing the Application

Once the issuer satisfies financial and governance prerequisites, it may submit a formal listing application to the target exchange.

The process typically involves:

- Pre-application consultation with exchange staff;

- Submission of detailed questionnaire covering financials, governance, and legal matters;

- Payment of initial application fees (typically $25,000–$75,000 depending on exchange and market tier);

- Background checks on directors, officers, and significant shareholders; and

- Exchange due diligence calls to verify responses and discuss potential issues.

The exchange’s review process generally lasts six to ten weeks, but timelines vary based on complexity and workload.

SEC and FINRA Coordination

Parallel to the exchange review, companies must coordinate with:

- The SEC’s Division of Corporation Finance, particularly if a Form S-1, S-3, or F-1 registration statement is being used for concurrent fundraising.

- FINRA’s Corporate Actions Department under Rule 6490 which reviews name changes, stock splits, and symbol changes.

FINRA’s review ensures that any corporate restructuring or symbol migration complies with securities regulations and prevents potential market confusion.

Case Study 1 — Small-Cap Technology Company

A technology issuer trading on OTCQB sought to uplist to the Nasdaq Capital Market. The company restructured $5 million in convertible debt, implemented a 1-for-10 reverse split, and added two independent directors with audit expertise. Within six months, it met all listing standards and completed a $20 million follow-on offering concurrent with uplisting.

Case Study 2 — Foreign Private Issuer

An international renewable-energy firm trading on OTCQX completed PCAOB audits under IFRS, engaged a U.S. transfer agent, and retained a Principal American Liaison (PAL). Upon meeting shareholder and governance criteria, the issuer successfully transitioned to Nasdaq Global Market status, gaining substantial U.S. institutional participation.

These examples illustrate how deliberate planning and legal strategy can transform an OTC company into a credible exchange-listed issuer.

Common Obstacles and Exchange Red Flags

- Low Bid Price and Market Volatility — Persistent sub-$4 trading levels often require reverse splits, which can depress liquidity if poorly communicated.

- Concentrated Insider Ownership — Exchanges require a minimum public float; concentrated control can delay approval.

- Toxic or Variable-Priced Debt — Convertible notes that reset conversion prices signal potential manipulation and are heavily scrutinized.

- Promotional History — Past “paid promotion” campaigns trigger exchange concerns about market integrity.

- Delayed SEC Filings — Any late Form 10-K or 10-Q filings may reset review timelines.

Exchanges maintain broad discretion under their “public interest” mandates. Early consultation with securities counsel can identify and mitigate these risks before filing.

The Role of the Board and Management

Strong governance is central to uplisting success. Exchanges evaluate not only compliance but also leadership credibility.

Issuers should ensure:

- The CEO and CFO have verifiable experience managing public-company reporting;

- Audit committees meet at least quarterly and maintain minutes;

- Internal controls under SOX Section 404(b) are documented; and

- Related-party transactions are disclosed under Regulation S-K Item 404.

Directors and officers should also complete annual questionnaires and background certifications verifying compliance with exchange and SEC rules.

Marketing, Investor Relations, and Post-Uplist Communication

A newly uplisted company must manage investor expectations carefully. The transition often draws heightened media attention, new retail participation, and increased regulatory visibility.

Best practices include:

- Establishing a Regulation FD policy to govern all investor communications;

- Issuing press releases that clearly distinguish between promotional content and factual updates;

- Maintaining an IR website with archived SEC filings and governance materials; and

- Preparing management for analyst calls and conference participation.

See: Investor Relations for Uplisted Companies

Nasdaq and NYSE both monitor issuer communications for compliance with anti-manipulation and disclosure rules.

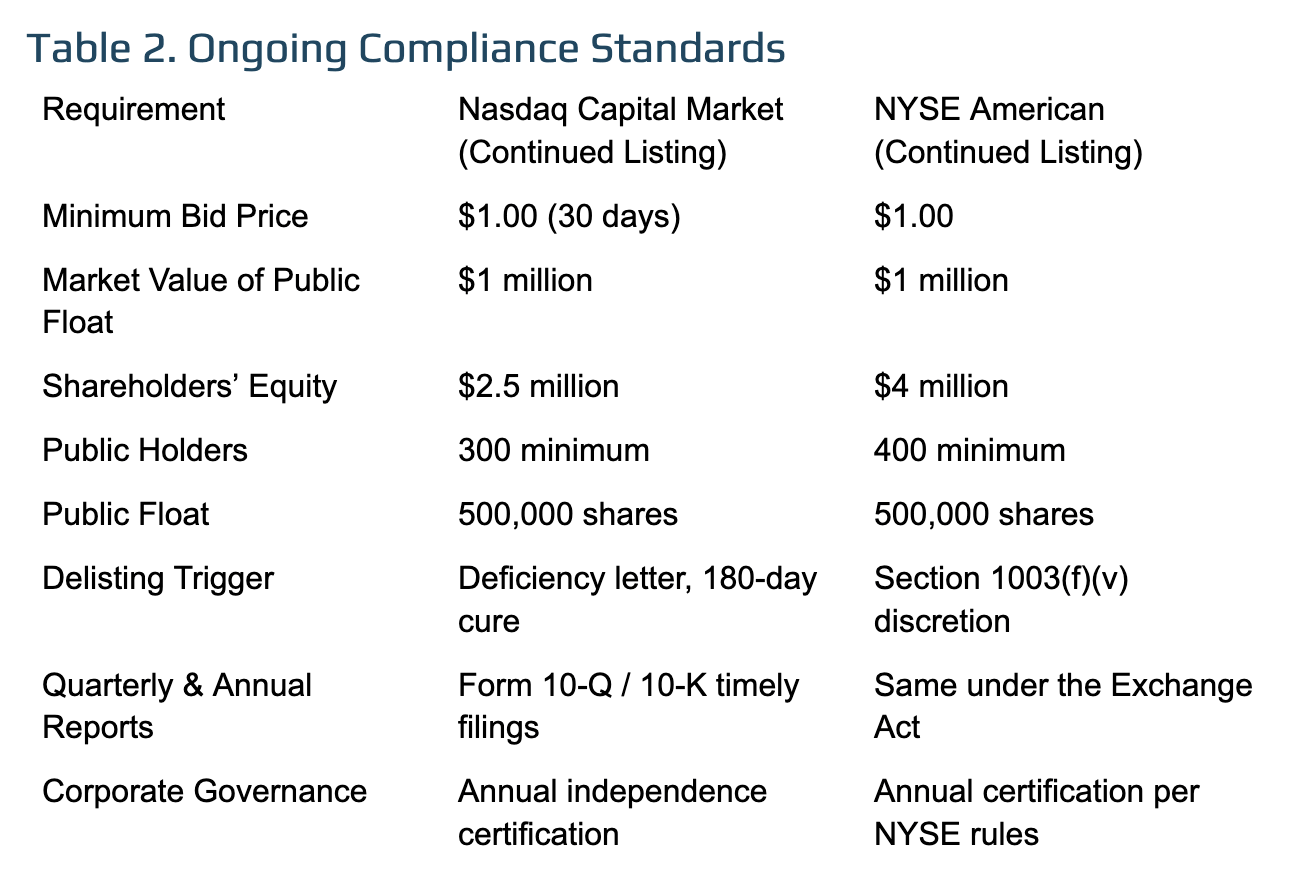

Post-Uplisting Obligations and Compliance

Once listed, the company must remain vigilant. Ongoing requirements include:

- Quarterly (10-Q) and Annual (10-K) filings under the Exchange Act;

- Form 8-K disclosures for material events within four business days;

- Annual certifications confirming continued compliance;

- Market surveillance cooperation with exchange staff; and

- Periodic governance reviews to ensure the continued independence of committees.

Issuers that fail to maintain minimum bid prices or file timely reports may face deficiency letters and eventual delisting proceedings.

Timeline and Milestone Expectations

| Milestone | Estimated Duration |

|---|---|

| Uplisting readiness assessment | 1–3 months |

| Corporate cleanup & audit completion | 3–6 months |

| Application review (Exchange & FINRA) | 2–3 months |

| SEC comment resolution (if applicable) | 1–2 months |

| Listing approval & trading commencement | 1–2 weeks post-approval |

Average total timeline: 8–12 months, depending on corporate complexity, audit readiness, and market conditions.

Our Approach

At Hamilton & Associates Law Group, P.A., we assist clients with:

- Uplisting strategy from OTCID, OTCQB, or OTCQX to Nasdaq or NYSE;

- Preparation of listing applications and exchange responses;

- Corporate restructuring and governance planning;

- SEC registration statements (Form S-1, S-3, or F-1); and

- Coordination with FINRA and transfer agents.

Our firm’s experience with public companies and exchange interactions ensures that clients anticipate — rather than react to — regulatory expectations.

Conclusion

Uplisting from OTC to a national exchange is demanding, but it remains one of the most rewarding steps an emerging public company can take. Nasdaq and NYSE listings are symbols of transparency, governance maturity, and market legitimacy.

With careful planning, disciplined reporting, and experienced legal guidance, companies can navigate the uplisting process successfully — transforming their market profile and unlocking broader capital opportunities.

For issuers seeking to begin the process, early consultation is critical. The difference between delay and approval often lies in preparation, governance integrity, and a clear understanding of exchange expectations.

Expanded Comparative Charts: Nasdaq vs NYSE Listing Requirements

If you have questions about uplisting your company to a national exchange or would like to speak with a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets. Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com