In securities law, determining whether someone is an affiliate can impact everything from the resale of shares to a company’s qualification for certain SEC filings. In other words, “affiliate” status isn’t just a label—it’s a regulatory ripple effect.

Let’s break it down.

The Official Definition: Straight from the SEC’s Playbook

Rule 405 of the Securities Act of 1933 defines an affiliate as:

Rule 405 of the Securities Act of 1933 defines an affiliate as:

“A person that directly, or indirectly through one or more intermediaries, controls, or is controlled by, or is under common control with, the person specified.”

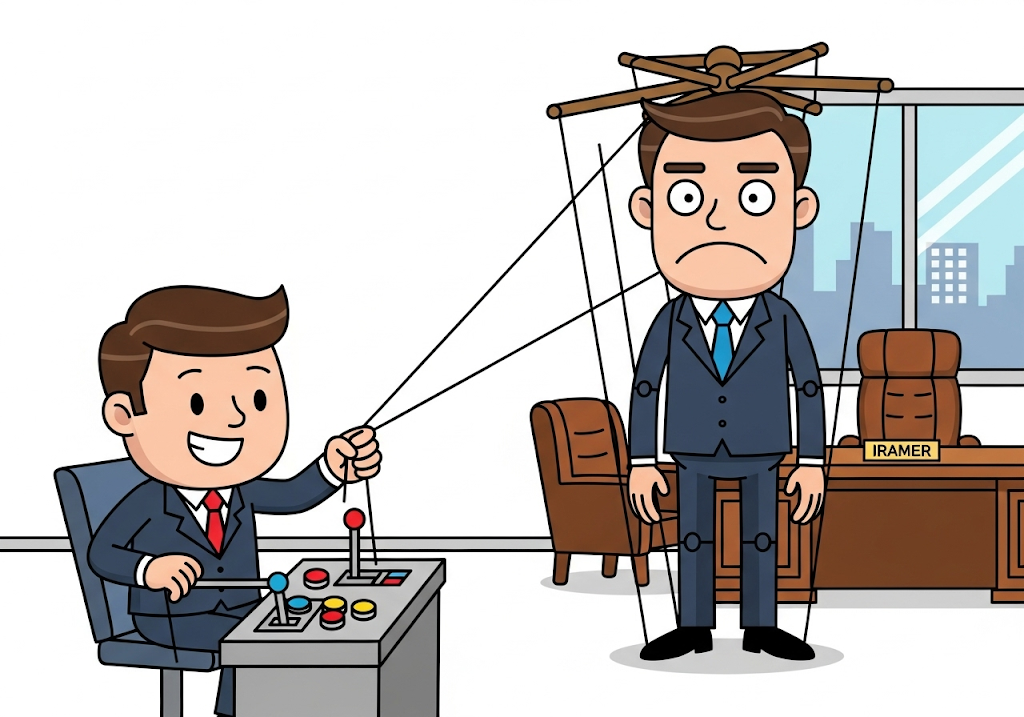

Clear as mud, right? Essentially, the SEC wants to know who’s really pulling the strings in a company. Control doesn’t always mean owning more than 50% of the stock—it can also mean influence over management, operations, or other stakeholders.

Think of it this way: if you own half the pizza, you clearly have control over the toppings. But if you don’t own half, but you still get to decide the toppings, the SEC might still call you an affiliate.

Control: It’s Complicated

Determining “control” is less about a bright-line rule and more about context. Here are some factors the SEC and courts look at:

- Share ownership: Majority ownership is a strong sign, but not required.

- Voting influence: Being able to sway shareholder votes counts.

- Management roles: Officers and directors are usually affiliates, but not always.

- Relationships: Family, business, or even social ties can tip the scales.

- Financial ties: Creditors with significant leverage over a company can sometimes be considered affiliates.

- Founders: If you built the sandbox, you probably still control how the toys are shared.

Bottom line: it’s not just about numbers; it’s about power and influence.

Why Affiliate Status Matters: The Resale Rules

If you’re holding restricted securities, your ability to resell them depends heavily on whether you’re an affiliate.

If you’re holding restricted securities, your ability to resell them depends heavily on whether you’re an affiliate.

- Rule 144: The most common “safe harbor” for resales. Affiliates face volume and timing limitations, as well as filing requirements. Non-affiliates? Much smoother sailing after six months to a year.

- Section 4(a)(1): This exemption doesn’t apply to affiliates, who are presumed to be acting like underwriters.

- Section 4(a)(7): Created under the FAST Act, it lets affiliates resell privately under certain conditions—though they must disclose their affiliation.

Translation: if you’re an affiliate, you can’t just unload your stock on the open market like you’re selling old furniture on Craigslist.

Does 10% Ownership Automatically Make You an Affiliate?

A common misconception is that owning 10% of a company’s shares automatically makes you an affiliate. The truth? Not necessarily.

A common misconception is that owning 10% of a company’s shares automatically makes you an affiliate. The truth? Not necessarily.

The SEC has repeatedly said that being an officer, director, or a 10% shareholder may indicate control, but those factors alone don’t seal the deal. Instead, it’s about the bigger picture:

- 10% ownership + influence (such as shaping management decisions or swaying other shareholders) → likely affiliate.

- 10% ownership, but passive (just collecting dividends and minding your business) → not automatically an affiliate.

That’s why you’ll often see investors distinguish themselves in SEC filings:

- Schedule 13D filers usually signal they want a say in how things run (hint: potential affiliate).

- Schedule 13G filers declare themselves as “passive investors” (less likely to be affiliates).

So, think of the 10% rule as more of a yellow flag than a red card. It raises the SEC’s eyebrow, but it doesn’t put you in the affiliate penalty box all by itself.

Special Rules for 10% Beneficial Owners

If you own more than 10% of a company’s registered class of equity securities, congratulations—you’ve earned a new title: “Section 16 insider.” Along with this fancy label comes some very real restrictions:

- Short-Swing Profit Rule (Section 16(b))

Any profit you make from buying and selling (or selling and buying) the company’s stock within a six-month window is recoverable by the company. In plain English: if you try to trade in and out quickly, the SEC says, “Nice try, but hand back those gains.” - Reporting Obligations

10% beneficial owners must file: - Form 3 when they first cross the 10% threshold,

- Form 4 within two business days of most transactions, and

- Form 5 for certain annual disclosures.

So yes, it’s paperwork city—but the SEC likes to keep tabs on insider trading activity.

- Rule 144 Resale Restrictions

Affiliates—including 10% beneficial owners—can sell their shares under Rule 144, but with strings attached: - Volume limits:

- 1% of the company’s outstanding shares during any 90-day period, or

- The average weekly trading volume of the securities during the four weeks prior to the sale (for exchange-listed companies).

- Current public information about the company must be available.

- Sales must usually go through brokers or market makers.

- A Form 144 must be filed if the sale exceeds 5,000 shares or $50,000 in any 3-month period.

- Volume limits:

Non-affiliates don’t face these same restrictions, which is why being classified as an “affiliate” (and especially as a 10% beneficial owner) makes a world of difference in how you can sell your stock.

Affiliates and Securities Offerings

Affiliate status also plays a starring role in how offerings are categorized:

- Primary offerings: Shares sold directly by the company.

- Secondary offerings: Shares sold by non-affiliate shareholders.

- Indirect primary offerings: When affiliates sell shares, but the SEC treats it as if the company itself were selling.

This categorization matters for pricing flexibility, underwriter liability, and how the offering can be structured. Get it wrong, and suddenly your “secondary” offering is treated like a primary one—complete with extra obligations.

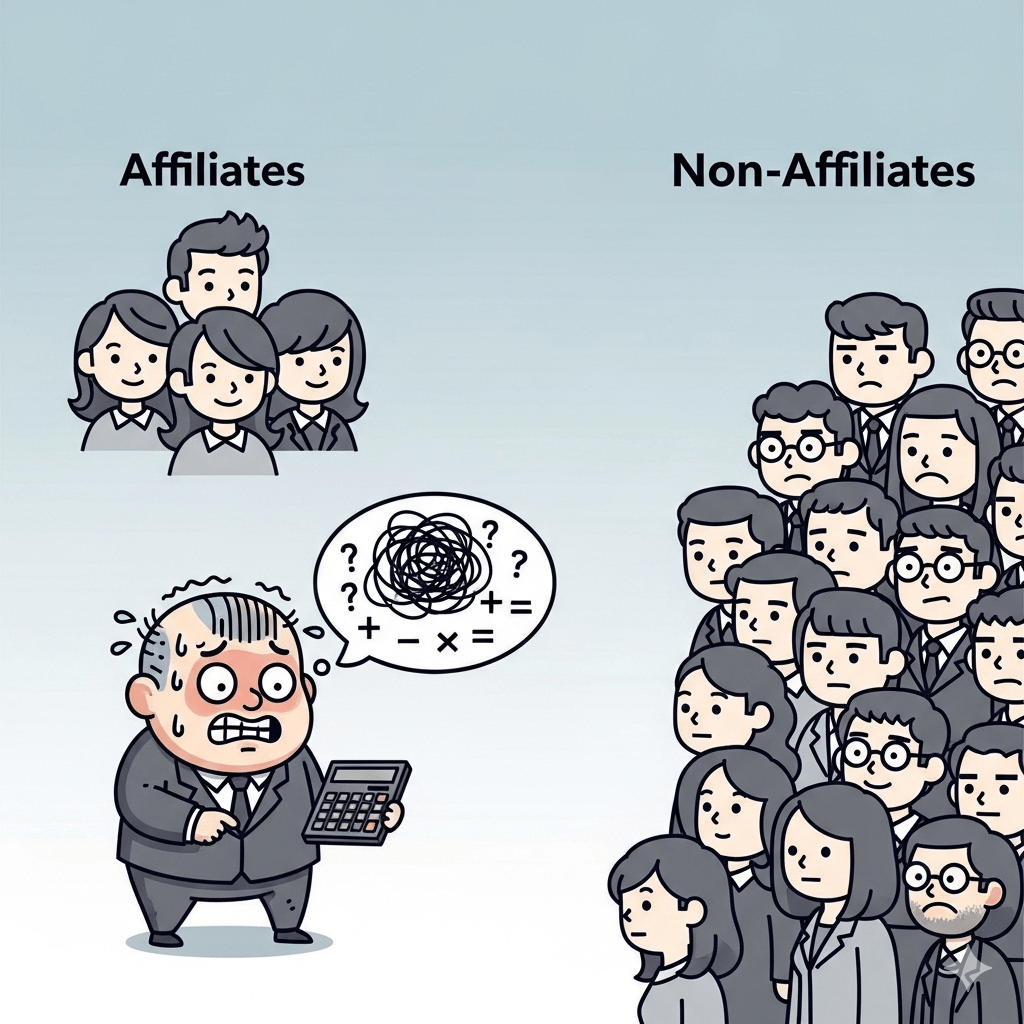

SEC Filing Status: Why Affiliates Are Counted Differently

Public companies are slotted into categories like large accelerated filer, accelerated filer, or smaller reporting company. The math behind these designations depends on how much stock is held by non-affiliates.

Public companies are slotted into categories like large accelerated filer, accelerated filer, or smaller reporting company. The math behind these designations depends on how much stock is held by non-affiliates.

For example:

- Large accelerated filers need $700M+ in non-affiliate float.

- Accelerated filers need between $75M and $700M.

- Smaller reporting companies have less than $250 million in non-affiliate float or less than $100 million in revenue.

If affiliates are misclassified, the company may end up filing incorrect reports, missing deadlines, or incurring significantly more expenses on compliance than necessary.

Why This All Matters

Affiliate status isn’t just a box to check—it impacts:

- How and when shares can be resold

- Which exemptions or safe harbors apply

- The category of offering (primary vs. secondary)

- The company’s reporting obligations and costs

In short, affiliate status is like the fine print in your cell phone contract—ignore it at your own peril.

Final Thoughts

Securities law loves its definitions, and “affiliate” is one of the trickier ones. Influence comes in many flavors—sometimes it’s about money, sometimes it’s about family ties, and sometimes it’s about who gets to pick the pizza toppings.

So, if you’re a shareholder, executive, or company counsel, pay attention to how “affiliate” applies to you. Because in the eyes of the SEC, being an affiliate can either open doors… or lock you out of the resale party.

If you have questions about affiliate status or would like to speak with a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets. Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com