FINRA Rule 6490 authorizes the Financial Industry Regulatory Authority (FINRA) to review, delay, or refuse to process corporate actions for companies whose securities are quoted on the Over-the-Counter (OTC) markets.

The rule protects investors and market integrity by ensuring that actions such as name changes, reverse stock splits, dividends, or spin-offs are implemented only after the issuer provides complete, accurate, and verifiable documentation.

For OTC issuers, a FINRA refusal can be devastating. Without FINRA’s processing, the action is not recognized in public markets—transfer agents, DTC, brokers, and data vendors will not update share counts, tickers, or capitalization tables.

The Purpose and Scope of Rule 6490

FINRA Rule 6490 applies to every Company-Related Action Notification filed through the FINRA Gateway by issuers of OTC-traded securities. Actions subject to review include:

- Corporate name or ticker-symbol changes

- Reverse or forward stock splits

- Stock and cash dividends

- Spin-offs, mergers, and reorganizations

- Changes in par value or state of domicile

Under Rule 6490(a), FINRA may conduct an information review to verify that all materials are accurate and compliant with federal and state securities laws.

Under Rule 6490(d), FINRA may refuse to process any action it deems incomplete, misleading, or unsupported by adequate disclosure.

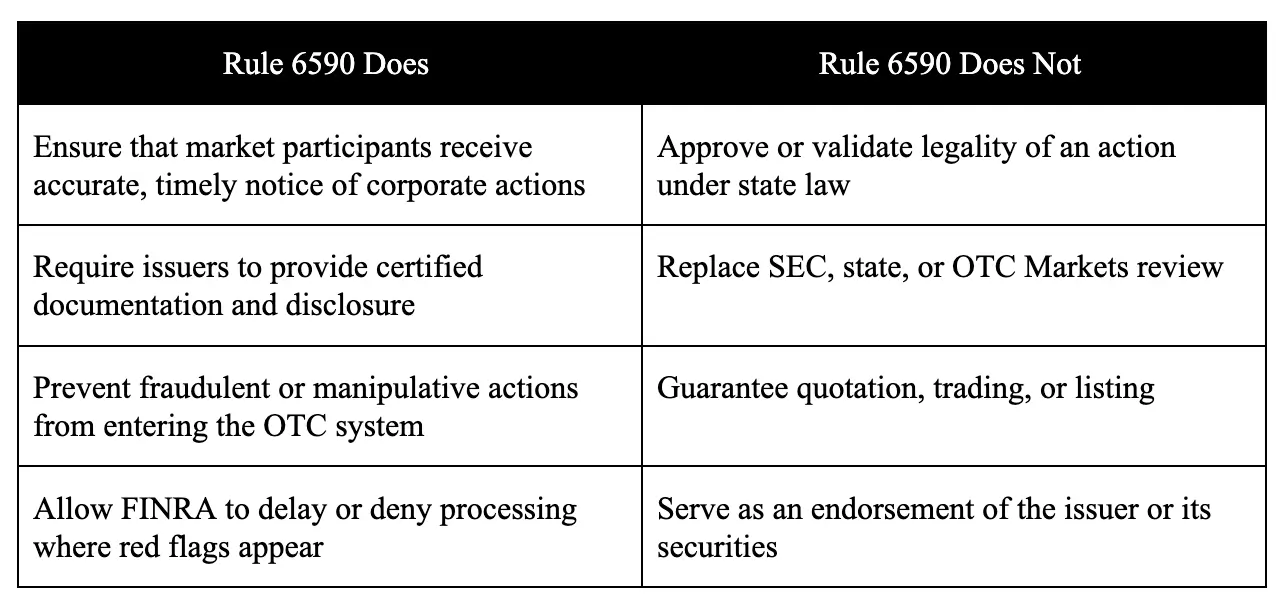

FINRA’s Gatekeeping Role

Rule 6490 functions as a market-integrity checkpoint, not an endorsement mechanism. The table below summarizes what the rule does —and does not—do.

FINRA’s responsibility is operational and protective. When information is inconsistent, outdated, or raises suspicion, FINRA may delay or refuse processing until the issues are resolved.

Common Reasons FINRA Refuses to Process Corporate Actions

FINRA refusals typically stem from one or more of the deficiencies below.

1. Delinquent SEC Filings or Non-Current Reporting Status

The leading cause of refusal is delinquency in SEC filings. FINRA will not process actions for issuers that are not current in reporting under the Securities Exchange Act of 1934.

Examples include:

- Failure to file the latest Form 10-K or Form 10-Q;

- Registration on Form 10 or Form 8-A followed by non-filing of periodic reports;

- Claiming “current information” on OTC Markets without maintaining SEC compliance.

FINRA’s position: No corporate action proceeds until all missing filings appear as accepted on the SEC EDGAR system.

2. Failure to Comply with Prior SEC Reporting Obligations

Even if current filings are up to date, FINRA also evaluates an issuer’s historical compliance. It may decline to process when:

- A predecessor or shell entity was a delinquent SEC filer or subject to revocation;

- The issuer previously registered under the Exchange Act but ceased reporting; or

- Corporate reorganizations appear designed to obscure a prior enforcement action.

FINRA interprets these patterns as attempts to evade transparency. Without documentation clarifying the corporate lineage, Rule 6490 authorizes refusal.

3. Failure to Provide Corporate Documents for Officers, Directors, and Control Changes

FINRA requires proof of a corporation’s legitimate authority. Issuers must submit:

- Appointment and resignation letters for all officers and directors;

- Board and shareholder resolutions approving the action;

- Control-change agreements and stock-purchase documentation;

- Updated shareholder ledgers and beneficial-ownership tables.

If gaps appear—missing minutes, unsigned consents, or unexplained ownership changes—FINRA may conclude that management lacks lawful authority, resulting in a refusal.

4. Incomplete or Inconsistent State Corporate Filings

FINRA cross-checks all state-level filings (e.g., amendments, mergers, or conversions). Processing stops if:

- Documents are uncertified or unsigned;

- State filings conflict with resolutions;

- Multiple active entities exist under the same name; and

- The filing has not been accepted by the Secretary of State.

Only certified, date-stamped documents establishing corporate authority will satisfy FINRA.

5. Evidence of Fraud, Manipulation, or Promotional Abuse

FINRA also refuses actions showing potential market manipulation or investor deception, such as:

- Repeated or extreme reverse splits to maintain artificial prices;

- Social-media or newsletter promotions that are inconsistent with filings;

- Unauthorized share issuances or conversions;

- False or exaggerated press releases; or

- Use of an unregistered transfer agent.

Suspect matters may be referred to the SEC Division of Enforcement or FINRA’s Market Regulation Department.

The Rule 6490 Review Process

The process unfolds in five stages:

- Submission – The issuer files a Company-Related Action Notification Form through the FINRA Gateway at least ten calendar days before the proposed effective date.

- Initial Review – FINRA verifies completeness and cross-checks SEC and state records.

- Information Requests – FINRA may request supplemental evidence (board minutes, filings, transfer-agent confirmations).

- Processing or Refusal – If complete, the action is published on FINRA’s Daily List; if not, a Refusal-to-Process Notice is issued citing Rule 6490(a)(5).

- Resubmission – The issuer may correct deficiencies and refile, but FINRA retains absolute discretion.

Typical review time ranges from ten to thirty days, depending on complexity and responsiveness.

Consequences of a Refusal

When FINRA refuses to process:

- The corporate action is void for market purposes—no new CUSIP, ticker, or share adjustment occurs.

- DTC and transfer agents freeze implementation pending FINRA clearance.

- OTC Markets Group will not update issuer profiles or market tiers.

- Investor confidence and financing prospects often decline sharply.

- Persistent deficiencies may trigger SEC enforcement or trading suspension.

A refusal is therefore not merely administrative; it can halt an issuer’s ability to raise capital or restructure.

How Issuers Can Avoid Rule 6490 Refusals

Preventing problems begins long before the filing.

Maintain Current SEC Filings

- All Forms 10-K, 10-Q, and 8-K must be current and accepted on EDGAR before a corporate action is requested.

Keep a Complete Corporate Record

- Maintain organized minutes, officer/director appointment and resignation documents, and shareholder approvals dating back to inception.

Submit Certified State Documents

- Provide only certified, state-filed amendments or mergers—drafts or screenshots are insufficient.

Disclose Control and Ownership Changes

- Every control shift, merger, or large issuance should be publicly reported through SEC filings or OTC Markets disclosures.

Engage Experienced Securities Counsel

- An attorney versed in FINRA Rule 6490, Rule 15c2-11, and OTC Markets requirements can ensure submissions are accurate and defensible.

Respond Promptly to FINRA Requests

- Transparent, timely communication minimizes delays and demonstrates good faith.

FINRA’s Broader Role in Market Integrity

Rule 6490 serves as the primary investor-protection barrier within the OTC market structure. It prevents dormant shells, delinquent filers, and illegitimate operators from manipulating corporate identity through serial name changes, recapitalizations, or promotional rebranding.

By demanding consistent disclosure and verified documentation, FINRA reinforces confidence in the OTC Markets Group’s OTCQX, OTCQB, and Expert Market tiers. This gatekeeping function complements the SEC’s disclosure regime and supports fair, orderly markets.

Conclusion

FINRA Rule 6490 is far more than a procedural checkpoint—it is a safeguard ensuring that only legitimate, transparent, and well-documented corporate actions reach investors.

FINRA routinely refuses or delays processing when issuers:

- Are delinquent in SEC reporting;

- Have unremedied historical compliance failures; or

- Cannot produce valid corporate records evidencing proper authority and control.

For every OTC issuer, the mandate is clear: full transparency, current reporting, and complete documentation are prerequisites for FINRA processing. Without them, even a lawful action cannot take effect in public markets.

About Hamilton & Associates Law Group, P.A.

Brenda Hamilton, Securities Attorney, represents public and private companies in matters involving FINRA Rule 6490, SEC registration statements, Rule 144 resales, and OTC Markets compliance.

Contact:

Hamilton & Associates Law Group, P.A.

101 Plaza Real South, Suite 202 North

Boca Raton, Florida 33432

Telephone (561) 416-8956 | Facsimile (561) 416-2855

Email [email protected]

Website www.SecuritiesLawyer101.com