Understanding Regulation S-K Item 401: Officer and Director Disclosure Requirements

Regulation S-K Item 401 is an SEC requirement designed to provide investors with essential background information on the individuals leading a company.…

Read MoreBlog

Insights on securities law, exchange listings, going public, SEC reporting, and market regulation. Stay updated with our latest articles on capital markets compliance, regulatory developments, and strategic guidance for public and private companies.

Regulation S-K Item 401 is an SEC requirement designed to provide investors with essential background information on the individuals leading a company.…

Read MoreA restrictive legend on a stock certificate acts as a practical trading freeze, signaling that shares cannot be sold unless registered under…

Read MoreIn the world of SEC reporting, Section 16a compliance is often viewed as a routine administrative task. However, treat it too lightly,…

Read MoreDirector independence is a core corporate governance requirement for a Nasdaq listing. It affects whether the board can satisfy the majority independent…

Read More“Testing the waters” (TTW) communications let an issuer conducting an IPO, and anyone acting on its behalf, such as its underwriters, gauge…

Read MoreMessage boards and social platforms can move thinly traded and microcap stocks quickly. That speed is exactly why the U.S. Securities and…

Read MoreOn September 30, 2025, we explored how deep-sea mining companies raising capital must treat regulatory uncertainty, international conflict, and expected challenges as…

Read MoreA free writing prospectus, commonly called an FWP, is a written offering communication used in a registered securities offering that is…

Read MoreOver the past several months, the Securities and Exchange Commission (SEC) has been sending a clear message: social media-driven stock promotions involving…

Read MoreThe United States Supreme Court is once again poised to reshape the securities enforcement landscape. With its agreement to hear a case…

Read MoreSEC Whistleblower referrals tend to move faster when a submission aligns with the SEC’s publicly stated enforcement and examination priorities—especially where the…

Read MorePractical guidance on Rule 144 legal opinions, restrictive legend removal, and transfer agent processing, including shell company and 144 legal opinion considerations.

Read MoreOfficers, directors, and other insiders try to “control” the flow of public sales - sometimes under the banner of Rule 144 -…

Read MoreThe National Oceanic and Atmospheric Administration (NOAA) has taken a major step to modernize U.S. rules for deep-seabed mining. This update…

Read MoreThe digital transformation of finance has blurred the line between investor communication and viral marketing. In the past decade, social media platforms…

Read MoreSection 16(a) reporting requirements to directors and executive officers of foreign private issuers marks a significant evolution in U.S. securities regulation. The…

Read MoreChoosing the right exchange is one of the most important strategic decisions a company makes when going public. The New York Stock…

Read MoreA Nasdaq direct listing allows an issuer to list its common equity on the exchange without the traditional underwritten initial public offering…

Read MoreGoing public is about raising capital and gaining prestige. An exchange listing provides companies access to institutional capital, enhances liquidity for…

Read MoreThe U.S. Supreme Court has agreed to hear a case that could significantly limit the Securities and Exchange Commission’s (SEC) ability to…

Read MoreGoing public doesn’t just change how you raise capital; it changes how you talk. From the moment a company seriously starts down…

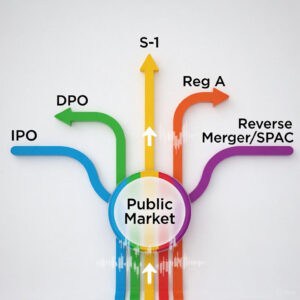

Read MoreCompanies seeking access to capital, liquidity, and market visibility have several pathways to becoming publicly traded. The most common methods include…

Read MoreA Form S-1 registration statement is the primary disclosure document used by companies seeking to go public in the United States. Whether…

Read MoreA reverse merger can be a viable path for a private company to gain a public listing, offering speed, cost efficiency, and…

Read MoreFINRA Rule 6490 authorizes the Financial Industry Regulatory Authority (FINRA) to review, delay, or refuse to process corporate actions for companies…

Read MoreFor issuers seeking to have their securities quoted on the OTC Markets, the submission and clearance of Form 211 by a…

Read MoreThis article details the Supreme Court petition in Xeriant, Inc. v. Auctus Fund, LLC, which challenges a Second Circuit opinion regarding Section…

Read MoreInitial listing requirements are the gatekeepers of the public markets. They calibrate who may access exchange‑based liquidity by aligning financial strength,…

Read MoreThe critical role of OTC Markets in facilitating secondary offerings and resales of restricted and control securities under SEC Rule 144. This…

Read MoreThis question-and-answer guide covers the legal and regulatory requirements for Nasdaq-listed companies holding their annual stockholder meetings. The article focuses on the…

Read MoreExplore our curated collection of external resources and industry links that complement our blog content. These hand-picked links provide additional perspectives on securities law, market regulations, and business compliance.