Annual and Quarterly Reporting Under the OTC Markets Alternative Reporting Standard

Posted on

The OTC Markets Alternative Reporting Standard provides a disclosure framework for companies that are not required to file reports with the SEC. Under this standard, issuers post financial and corporate information to the OTCIQ disclosure portal to satisfy the public information requirements of Rule 15c2-11. To maintain Current Information status, issuers must publish annual and quarterly reports, officer certifications, and a Manager’s Certification with Respect to Current Information.

Who Must Comply With the Alternative Reporting Standard

The standard applies to non-SEC-reporting issuers quoted on OTCID (Current Information) or OTCQB, certain foreign private issuers not filing Form 20-F or 6-K, and private companies seeking quotation under Rule 15c2-11. Failure to post required disclosures leads to a downgrade or suspension.

Understanding Rule 15c2-11 Current Information Standard

Posted on

For companies quoted on the OTC Markets, maintaining “Current Information” status is essential to avoid downgrade or suspension. Under SEC Rule 15c2-11, broker-dealers may publish or maintain quotations only when an issuer’s disclosures are accurate, complete, and publicly available. OTC Markets evaluates whether the information posted by an issuer meets this standard, and failure to comply may lead to placement on the Expert Market. Read More

How the OTC Markets Expert Market Works – Securities Lawyer 101

Posted on

The 2021 amendments to SEC Rule 15c2-11 reshaped how broker-dealers publish quotations for OTC securities. Under the new framework, only issuers with current, publicly available information can maintain quotations. Issuers that fail to meet disclosure requirements are moved to the OTC Markets Expert Market, where trading is limited to broker-dealers and qualified institutions.

What Is the OTC Markets Expert Market?

The Expert Market is the lowest OTC Markets tier and serves as a restricted venue for institutional participants. It replaces the former ‘No Information’ category, limiting access to professional investors only.

- No public quotation visibility for retail investors.

- Only broker-dealers and qualified institutions can trade.

- Quotations are limited to unsolicited broker-dealer transactions.

- Effective since September 28, 2021, under Rule 15c2-11.

SEC and FINRA Enforcement Trends in the OTC Market

Posted on

Over the past several years, both the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) have intensified enforcement in the OTC Markets. The focus has shifted sharply toward broker-dealer gatekeeper obligations, fraudulent stock promotions, and manipulative trading. Read More

Promotional Activity & Investor Relations Rules on OTC Markets

Posted on

Promotional activity has long been part of investor relations for smaller public companies. However, on the OTC Markets, stock promotion presents heightened regulatory risk because it can easily cross into manipulative or misleading activity. To protect investors, OTC Markets Group and regulators such as the SEC and FINRA have established strict rules governing how issuers, promoters, and investor-relations firms may disseminate information. The goal is transparency—so that investors understand who paid for promotional content, how it was distributed, and whether it is independent or sponsored. Read More

OTC Markets Direct – Bypassing the Sponsoring Market Maker Under SEC Rule 15c2-11

Posted on

In September 2021, the Securities and Exchange Commission (“SEC”) adopted amendments to Exchange Act Rule 15c2-11, reshaping how securities become eligible for public quotation on over-the-counter (“OTC”) markets.

Previously, issuers relied on a sponsoring market maker to file a FINRA Form 211 before quotations could be published. The 2021 amendments authorized qualified inter-dealer quotation systems (“IDQS”)—including OTC Markets Group Inc.—to conduct their own Initial Information Reviews.

This allows issuers to work directly with OTC Markets through its OTCIQ Portal, bypassing the sponsoring market maker while maintaining full compliance under Rule 15c2-11. Read More

SEC to Formalize “Innovation Exemption” by Year-End: What It Means for Digital Asset Issuers and Market Participants

Posted on

The U.S. Securities and Exchange Commission (SEC) is preparing to formalize a long-discussed “innovation exemption” by the end of 2025, according to recent statements from Chair Mark Atkins. The initiative is designed to provide regulatory flexibility for emerging technologies, including blockchain and tokenized assets, while maintaining investor-protection standards under existing securities laws.

Background: The Push for Regulatory Clarity

For years, startups in the blockchain and digital-asset sectors have argued that the SEC’s rules are overly restrictive and ill-suited for decentralized technologies. Projects often face the difficult choice between delaying innovation and risking enforcement under the Howey Test. Chair Atkins’s remarks suggest that the agency intends to codify a structured exemption similar in spirit to the “Token Safe Harbor” framework proposed in 2021 by then-Commissioner Hester Peirce, but updated to reflect lessons from recent enforcement cases and global regulatory alignment efforts. Read More

The Role of Transfer Agents in OTC Markets Compliance

Posted on

![]()

In the OTC Markets, transfer agents play a critical — yet often overlooked — role in ensuring compliance, shareholder transparency, and investor confidence. For issuers quoted on the OTCQB, OTCQX, or OTCID market tiers, maintaining a reliable and SEC-registered transfer agent is essential to sustaining market integrity and avoiding compliance downgrades.

For a broader understanding of OTC issuer requirements, see: https://www.securitieslawyer101.com/2024/otc-markets-reporting-requirements/

What Is a Transfer Agent?

A transfer agent is a third-party professional or firm authorized to maintain an issuer’s shareholder records, process share issuances and cancellations, and manage stock transfers between investors. Transfer agents act as the official keepers of the share ledger, ensuring the accuracy of outstanding shares and ownership records. Under Section 17A of the Securities Exchange Act of 1934, transfer agents performing services for registered securities must register with the SEC. Read More

Uplisting from OTC Markets to Nasdaq or NYSE

Posted on

Uplisting from the OTC Markets to Nasdaq or NYSE American represents a pivotal transition for emerging companies seeking greater liquidity, institutional visibility, and enhanced credibility. This expanded guide outlines the financial, governance, and regulatory requirements — including SEC registration, FINRA Rule 6490 compliance, PCAOB audit standards, and market readiness — that issuers must meet to successfully uplist.

Why Uplist? Strategic Benefits vs. Real-World Hurdles

Moving from OTCQB, OTCQX, or OTCID to a national exchange expands institutional access, attracts analyst coverage, and can reduce the cost of capital. It also imposes rigorous corporate governance, minimum bid price requirements, and shareholder-distribution standards. National exchanges offer several advantages, including increased credibility, eligibility for inclusion in ETFs, greater liquidity, and access to institutional trading platforms. Read More

When Short Sellers Hit OTC Markets Stocks – Securities Lawyer 101

Posted on

The Reality of Short Selling in OTC Markets

Short selling — the sale of borrowed shares with the expectation of repurchasing them later at a lower price — plays a legitimate role in market efficiency. However, in the Over-the-Counter (OTC) Markets, where liquidity and transparency remain limited, short selling can be disruptive and manipulative when misused.

Issuers quoted on the OTCQX, OTCQB, or OTCID (OTC Information Designation) tiers often experience sudden price swings when targeted by aggressive short sellers. The shift from the former Pink Market to the new OTCID system underscores OTC Markets Group’s modernization efforts to enhance transparency and regulatory alignment.

Because OTC securities trade with lower volume and less institutional participation, aggressive short activity can trigger panic selling, liquidity loss, and significant price distortion — particularly in low-float microcap issuers. Read More

OTC Markets Direct: Sponsoring Market Makers Bypassed Under Rule 15c2-11

Posted on

The OTC Markets Group has transformed how companies access public quotations after the SEC’s 2021 amendments to Rule 15c2-11. Before the reform, a market maker had to submit FINRA Form 211 to initiate quotation for an issuer’s securities. Today, OTC Markets Group, Inc.—the operator of OTCQX, OTCQB, and OTC Pink—may conduct its own review of issuer information and determine compliance with Rule 15c2-11 without a sponsoring broker-dealer.

The OTC Markets Initial Information Review Process

Issuers seeking to quote securities on the OTC Markets can now approach OTC Markets Group directly through the OTCIQ Issuer Portal to begin an Initial Information Review. The process includes application submission, staff review, and coordination with FINRA, leading to a determination that the issuer’s information is current and publicly available. Read More

The SEC’s Inspector General Calls for Overhaul of CorpFin’s Disclosure Review Process

Posted on

The U.S. Securities and Exchange Commission’s Office of Inspector General (OIG) has released a critical audit evaluating how the Division of Corporation Finance (“CorpFin”) conducts its disclosure review program. The report highlights procedural gaps, incomplete guidance, and inadequate documentation practices that could compromise the SEC’s ability to effectively oversee public company filings. For public companies, securities lawyers, and compliance officers, the OIG’s findings are more than bureaucratic housekeeping—they may reshape how the SEC selects and scrutinizes issuers’ filings in 2025 and beyond.

Overview: Why the OIG Report Matters

The Division of Corporation Finance is responsible for reviewing the filings of thousands of issuers to ensure compliance with the Securities Act of 1933 and the Exchange Act of 1934. Its review process influences disclosure quality, investor protection, and overall market integrity. The Inspector General’s audit was designed to determine: (1) whether CorpFin employs a risk-based approach to identify which filings to review; and (2) whether it complies with Section 408 of the Sarbanes-Oxley Act, requiring review of each issuer’s financial statements at least once every three years. The audit’s results were striking—revealing outdated procedures, incomplete documentation, and a lack of transparency in how filings are selected and scoped for review. Read More

Texas Stock Exchange Nears Launch After SEC Approval — A New Challenger to NYSE and Nasdaq

Posted on

Published: October 6, 2025

In a landmark decision that could alter the balance of power in U.S. capital markets, the Texas Stock Exchange (TXSE) has received approval from the U.S. Securities and Exchange Commission (SEC) to operate as a national securities exchange. The Dallas-based exchange, backed by major institutional investors and corporate heavyweights, is now one step closer to launching its trading operations in 2026. This development marks the first SEC approval of a new national stock exchange in decades and signals the rise of Texas as a growing financial hub that rivals New York in both capital and confidence.

What Is the Texas Stock Exchange (TXSE)?

The Texas Stock Exchange Group Inc. was formed with a mission to create a more issuer-friendly, pro-business public market. Headquartered in Dallas, TXSE aims to attract companies frustrated by rising listing costs, governance mandates, and complex compliance requirements imposed by incumbents such as Nasdaq and the New York Stock Exchange (NYSE). Backed by over $100 million in private investment, the Texas Stock Exchange represents one of the most well-capitalized new entrants in the history of exchanges. It intends to list equities, ETFs, and potentially IPOs, providing a full alternative to existing U.S. exchanges. Read More

SEC Takes Action to Curb Skyrocketing Costs of Consolidated Audit Trail

Posted on

The U.S. Securities and Exchange Commission (SEC) has issued an order providing conditional exemptive relief aimed at trimming the operating expenses of the Consolidated Audit Trail (CAT), a massive database designed to track all equity and options trades in the U.S. markets. Announced on September 30, 2025, this move comes in the wake of ongoing criticisms over the system’s ballooning costs and a recent court ruling that upended its funding structure.

The CAT, mandated by Rule 613 of Regulation NMS following the 2010 Flash Crash, was intended to enhance market surveillance by creating a comprehensive audit trail of trading activity. However, since its inception, the project has been plagued by delays, technical issues, and escalating expenses that have far exceeded initial projections. The 2025 budget approved by the CAT’s Operating Committee initially topped $248 million, but prior adjustments had already reduced forecasts to around $196 million. With the new exemptive relief, the SEC estimates an additional savings of $20 million to $27 million for the year.

Restricted Stock Q&A — 2025 Edition

Posted on

Prepared by Hamilton & Associates Law Group, P.A.

www.securitieslawyer101.com

Introduction

Restricted and control securities are common in private placements, employee compensation, and merger transactions. Although these shares are “restricted” at issuance, they may later become eligible for resale under Rule 144 or other exemptions if specific conditions are met.

This Q&A explains the principal rules, SEC guidance, and common questions regarding the resale of restricted and control stock, including the impact of shell-company status, affiliate restrictions, and reporting obligations. Read More

Rule 144 Resales of Restricted Securities of Shell Companies and Former Shell Companies

Posted on

Under Rule 405 and Rule 12b-2 of the Securities Exchange Act, a ‘shell company’ is defined as a company with no or nominal operations and no or nominal assets other than cash or cash equivalents. This classification is subject to significant resale restrictions under Rule 144(i) of the Securities Act of 1933. This article explains when and how securities of SEC reporting and non-reporting shell companies may be resold, and provides direct links to authoritative SEC sources and related articles on SecuritiesLawyer101.com.

Rule 144(i): The Restriction on Shell Company Resales

Rule 144 is unavailable for securities initially issued by a shell company or a company that has ever been a shell. Resales under Rule 144 may occur only when the issuer: (1) is no longer a shell, (2) is subject to Exchange Act reporting requirements, (3) has filed all required reports (excluding Form 8-K) for 12 consecutive months, and (4) has filed Form 10-type information at least one year earlier. See SEC Release No. 33-8869. Read More

Selling Private Placement Shares on Forge Global, Nasdaq Private Market, or Illiquidx

Posted on

Company shareholders, whether employees, founders, or early investors, are increasingly looking to secondary marketplaces like Forge Global, Nasdaq Private Market (NPM), and Illiquidx to sell the shares they purchase in exempt offerings such as Regulation D. We often get asked whether restricted stock acquired in a private placement can be sold on these platforms.

The short answer is: yes, it may be possible—but only if several legal, contractual, and practical requirements are met. Read More

Deep-Sea Mining, Public Market: Capital, Risk, and Regulatory Turbulence

Posted on

Deep-Sea Mining and Capital Markets

As demand surges for strategic minerals like nickel, cobalt, manganese, and rare earths, deep-sea mining firms are increasingly turning to public markets as a path to raise the substantial capital needed for exploration, deepwater infrastructure, and subsea recovery systems. Listing on exchanges such as Nasdaq or the New York Stock Exchange (NYSE) provides access to institutional investors, liquidity, and reputational cachet—particularly useful in the capital-intensive and politically sensitive business of mining the ocean floor.

These listings may be executed via an initial public offering (IPO), a SPAC merger, a direct listing, or hybrid financing structures. However, the transition to public markets brings greater regulatory scrutiny, enhanced disclosure obligations, and higher governance expectations than in the private realm. Read More

SEC Trading Suspensions of QMMM, SDM – New SEC Cross-Border Task Force

Posted on

On September 29, 2025, the U.S. Securities and Exchange Commission (SEC) issued back-to-back trading suspensions for two foreign issuers listed on the Nasdaq Capital Market, underscoring regulatory concerns about fraudulent, social-media-driven stock manipulation. These are the first SEC trading suspensions since October 2024, making the actions both rare and significant.

Smart Digital Group Limited (SDM) and QMMM Holdings LTD (QMMM) in the SEC’s Crosshairs

- Smart Digital Group Limited (SDM) is a Cayman Islands holding company with principal executive offices in Singapore, listed on the Nasdaq Capital Market on May 1, 2024, at an IPO price of $4.00 per share. By the close of business on September 28, 2025, SDM’s stock had fallen to $1.85 per share—less than half its offering price.

- QMMM Holdings Limited (QMMM) is a Cayman Islands holding company based in Hong Kong, listed on the Nasdaq Capital Market on July 19, 2024, at an IPO price of $4.00 per share. By September 28, 2025, QMMM’s shares had soared to $119.40 per share, an extraordinary rise from its IPO level.

Both trading suspensions took effect at 4:00 a.m. ET on September 29, 2025, and are scheduled to terminate at 11:59 p.m. ET on October 10, 2025. Read More

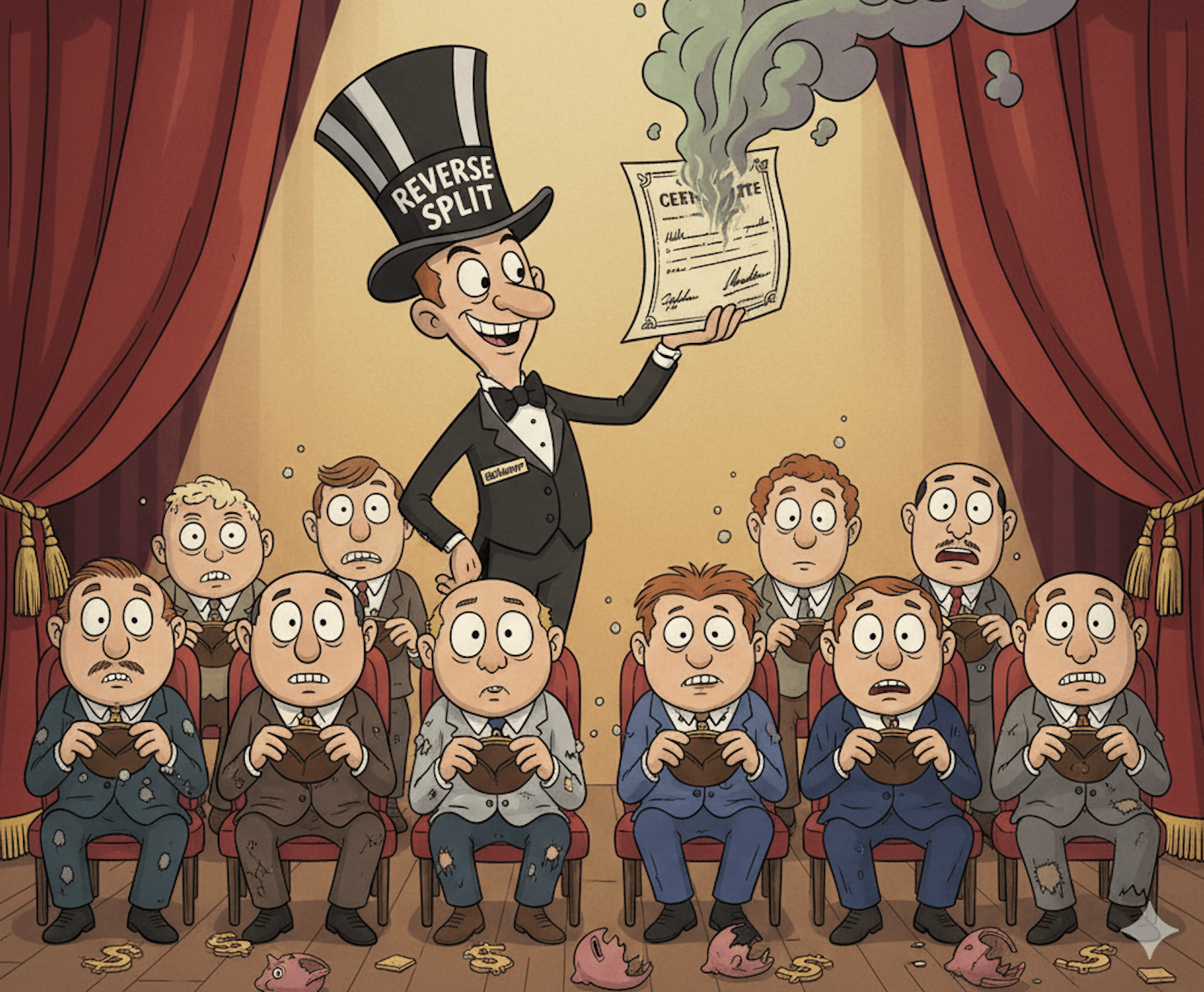

Bollinger Innovations: The Curious Case of the Disappearing Investor

Posted on

Yesterday, Bollinger Innovations Inc. (BINI) (formerly Mullen Automotive, Inc. (MULN)) announced a 1:250 reverse stock split, effective Monday, September 22, 2025, in an effort to regain compliance with the Nasdaq’s minimum bid price rule.

Under this plan, every 250 shares currently held by shareholders will be consolidated into a single share, reducing Bollinger’s approximately 126.2 million shares outstanding to about 505,000 shares (rounding fractional shares up). Read More

Rule 144 and 145: The SEC’s Favorite Party Poopers

Posted on

When it comes to the resale of securities, few areas of securities law generate as much scrutiny as those involving shell companies. Investors and issuers alike must navigate complex restrictions under the Securities Act, particularly the interplay of Rule 144 and Rule 145. We’ll walk through the resale restrictions under the Securities Act of 1933 (the “Securities Act”), focusing on Rule 144 and Rule 145. These rules set the stage for how securities of shell companies and former shell companies can be resold. Read More

Trump Says No More Nasty 10-Qs — Make SEC Reporting Great Again

Posted on

President Donald Trump has revived an idea he first floated during his earlier administration: doing away with quarterly reporting requirements for U.S. public companies. This move aligns with President Trump’s vision of reducing bureaucratic hurdles and fostering a business environment that prioritizes innovation and growth.

Direct Public Offerings in 2025

Posted on

A Direct Public Offering (DPO) is an effective method for going public. Private companies may also raise capital by selling securities directly to the public without intermediaries like underwriters or investment banks. This approach, also known as a direct listing, eliminates many of the costs and complexities associated with traditional Initial Public Offerings (IPOs) or reverse mergers, making it an attractive option for small to mid-sized companies seeking public company status. Below, we explore the key aspects of DPOs, their benefits, regulatory requirements, and practical considerations for issuers in 2025, based on the latest insights from securities law experts. Read More

Nasdaq Proposes Tougher Listing Standards

Posted on

On September 3, 2025, Nasdaq unveiled proposed updates to its listing standards, designed to strengthen investor protections and enhance market integrity. The changes come amid heightened concerns about market manipulation and liquidity in smaller company securities, and reflect the exchange’s ongoing efforts to adapt to evolving market dynamics.

Key Proposed Changes

Nasdaq’s revisions target both new listings and ongoing listing compliance:

- Higher Public Float Threshold: New listings under the net income standard will now require a minimum market value of publicly held shares (public float) of $15 million. This helps guarantee better liquidity right from the start.

- Faster Suspension and Delisting: Companies with a listing deficiency and a Market Value of Listed Securities below $5 million will face an accelerated suspension and delisting process.

- Stricter Standards for China-Based Companies: New listings from companies principally operating in China must raise at least $25 million in public offering proceeds, reviving a threshold first introduced for “restrictive markets” in 2020.

Navigating Periodic Reporting for U.S. Public Companies

Posted on

As a public company in the U.S., staying on top of your SEC reporting obligations under the Securities Exchange Act of 1934 (Exchange Act) is crucial. These requirements ensure transparency, keep investors informed about key developments, and help maintain market integrity. Whether you’re a newly public company or a seasoned issuer, understanding periodic reporting—Form 10-K, Form 10-Q, and current event (Form 8-K) reports—can prevent costly missteps.

What Makes a Company a “Reporting Company”?

A reporting company is one that has triggered ongoing disclosure obligations under the Securities Exchange Act of 1934. This can happen in three common ways:

- Listing on a national exchange (Section 12(b))

If you list securities on the NYSE, Nasdaq, or another national exchange, you must register with the SEC. - Hitting size thresholds (Section 12(g))

Even without a listing, companies with more than 2,000 shareholders (or 500 who are not accredited investors) and over $10 million in assets must register. - Filing a public registration statement (Section 15(d))

Companies that offer securities to the public via a registration statement (e.g., for debt or equity) automatically assume reporting responsibilities once the statement becomes effective.

Once subject to these rules, you’ll need to keep investors informed with ongoing filings. Read More

Hedge Funds Just Won a Key Review of the SEC’s Short-Sale Disclosure Rule. Here’s What It Means.

Posted on

A federal appeals court has ordered the Securities and Exchange Commission to take a fresh look at the economic impact of its short-sale transparency regime—a notable win for hedge fund groups that sued to block it. On August 25, 2025, a three-judge panel directed the SEC to reconsider the costs and cumulative economic effects of the rule, while leaving the agency’s underlying authority intact. The challenge was brought by industry associations representing hedge funds and other private funds. Read More

Navigating Audit Committee Requirements

Posted on

For public companies in the U.S., the audit committee plays a critical role in maintaining investor confidence and ensuring accountability. Audit committees sit at the intersection of corporate governance, financial integrity, and risk oversight. If you serve on a board—or advise one—understanding the rules that govern audit committees is essential. Read More

Navigating Florida’s Revamped Securities Laws

Posted on

In 2023 and 2024, Florida lawmakers overhauled Chapter 517, the Florida Securities and Investor Protection Act, ushering in a new era for businesses and investors. Effective October 1, 2024, these changes make it easier for Florida companies to raise capital locally while strengthening protections against fraud.

The reforms cover three key areas:

- Modernized registration and licensing rules

- New and expanded capital-raising exemptions

- Stronger investor protection and enforcement tools

This blog dives into the new exemptions and rescission rights, offering a clear guide for businesses and investors. Read More

What Happens at the SEC During a Government Shutdown?

Posted onIn its “Operations Plan Under a Lapse in Appropriations and Government Shutdown,” the SEC lays out with surprising candor the bare-bones framework it must follow when Congress fails to fund it. Here’s a breakdown of what the SEC will and will not do during a funding lapse.

Core Continuities: What Stays Alive

1. EDGAR remains open — for basic filing only

One of the few bright spots for market participants is that the SEC expects EDGAR to continue accepting filings, including registration statements, periodic reports, proxy materials, and amendments. That said:

Read More