Federal Jury Convicts Defendants In NuTech Energy Resources Securities Fraud

On Wednesday, October 13, 2021, a federal jury in Cheyenne returned guilty verdicts against a Pennsylvania man and two Florida men related…

Read MoreBlog

Insights on securities law, exchange listings, going public, SEC reporting, and market regulation. Stay updated with our latest articles on capital markets compliance, regulatory developments, and strategic guidance for public and private companies.

On Wednesday, October 13, 2021, a federal jury in Cheyenne returned guilty verdicts against a Pennsylvania man and two Florida men related…

Read MoreAcross 2016–2020, enforcement actions centered on insider trading, offering frauds (including Ponzi‑like schemes), microcap promotion/manipulation, disclosure and internal‑controls failures, gatekeeper lapses, and…

Read MoreOn September 30, 2021, the Securities and Exchange Commission (the “SEC”) announced charges against Mark Melnick, a day trader and T3 Live…

Read MoreOn September 28, 2021, the Securities and Exchange Commission (the “SEC”) announced that it filed an emergency action and obtained an asset…

Read MoreOn September 24, 2021, the Securities and Exchange Commission (“SEC”) charged Carebourn Capital, L.P. and its managing partner Chip Rice of Maple…

Read MoreProceedings under Section 12(j) of the Securities Exchange Act of 1934, (the “Exchange Act”) are frequently initiated when an SEC reporting company…

Read MoreToday, the Securities and Exchange Commission charged a Florida resident and his friend for engaging in a fraudulent scheme designed to collect…

Read MoreWe’ve written several times about the Securities and Exchange Commission’s (“SEC”) amendments to Rule 15c2-11, first proposed in September 2019 and adopted…

Read MoreWe last wrote about the Securities and Exchange Commission’s new Rule 15c2-11 in early August. The amended rule was proposed in September…

Read MoreOn September 15, 2021, the Securities and Exchange Commission (the “SEC”) awarded approximately $110 million to a whistleblower whose information and assistance…

Read MoreOn September 8, 2021, the Securities and Exchange Commission (the “SEC”) charged Nevada resident Frederick Bauman with playing a critical role as…

Read MoreOn September 1, 2021, the Securities and Exchange Commission announced that it filed an action against Alexander Kon, a penny stock promoter…

Read MoreIn 2020, the Securities and Exchange Commission (the “SEC”) stepped up its efforts to reel in “toxic lenders”: individuals who profit enormously…

Read MoreOn August 2, 2021, Gary Gensler, the new chair of the Securities and Exchange Commission (SEC), announced that because he wasn’t entirely…

Read MoreOn Friday, August 13th, the Securities and Exchange Commission (the “SEC”) filed charges against GPL Ventures LLC, GPL Management LLC, Alexander J.…

Read MoreGoing public offers many benefits to companies seeking to grow their business, including: Enhanced ability to raise capital, Liquidity for founders and…

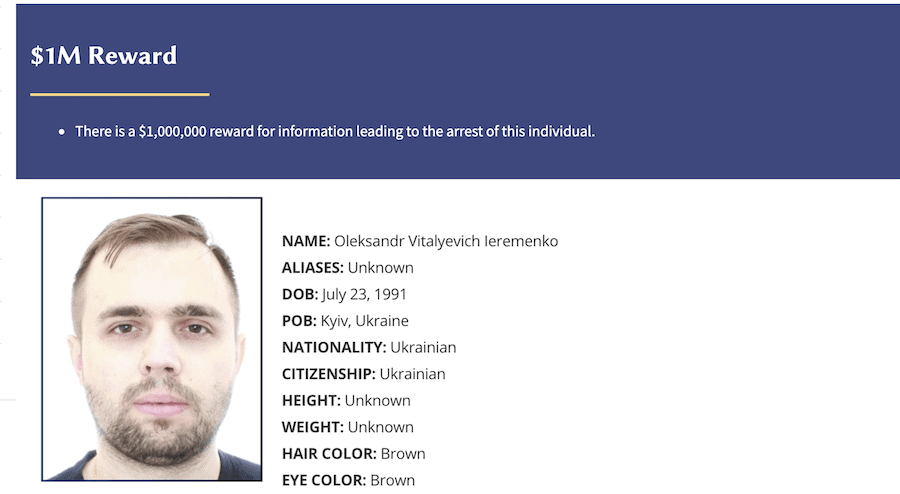

Read MoreOn July 29, 2021, the United States District Court for the District of New Jersey entered a default judgment against Oleksandr Ieremenko…

Read MoreAs the summer of 2021 enters its final months, investors in the U.S. over-the-counter market and OTC issuers themselves await the rollout…

Read More2020 has been a historic year for Securities and Exchange Commission ("SEC") enforcement action against toxic lenders as unregistered dealers.

Read MoreOn July 29th, the Securities and Exchange Commission (the “SEC”) announced charges against Trevor R. Milton, the founder, former CEO and former…

Read MoreOn July 22, 2021, the Securities and Exchange Commission (the “SEC”) filed an emergency action charging California resident Charlie Abujudeh with running…

Read MoreOn July 15th, the Securities and Exchange Commission (the “SEC”) announced charges against Marlon Muller for engaging in a pattern of…

Read MoreOn September 28, 2021, new amendments to Rule 15c-211 under the Securities Exchange Act of 1934 go into effect to enhance investor…

Read MoreToday, July 15, 2021, the Securities and Exchange Commission (the “SEC”) charged the former CEO and CFO of FTE Networks, Inc. (“FTE”),…

Read MoreToday, the Securities and Exchange Commission (the “SEC”) suspended trading in 55 publicly traded penny stock companies because of public interest concerns.…

Read MoreOn July 9th, the Securities and Exchange Commission (the “SEC”) charged three individuals with insider trading in advance of an announcement by…

Read MoreOn July 1st, the Securities and Exchange Commission (the “SEC”) filed charges against banned attorney Shawn F Hackman for violating a September…

Read MoreOn June 30, the Securities and Exchange Commission (the “SEC”) announced settled charges against Reuben Robert Goldman and his online stock promotion…

Read MoreOTC Markets Pink companies will need to update their disclosure to ensure they comply with the new requirements. Alternative Reporting…

Read MoreIn September of last year, the Securities and Exchange Commission (the “SEC”) adopted amendments to Securities Exchange Act Rule 15c2-11. In early 2020, we…

Read MoreExplore our curated collection of external resources and industry links that complement our blog content. These hand-picked links provide additional perspectives on securities law, market regulations, and business compliance.