{kind=link}

A Nasdaq direct listing allows an issuer to list its common equity on the exchange without the traditional underwritten initial public offering (IPO) process. While a traditional IPO involves underwriters building a book of demand and providing price stabilization, a direct listing prioritizes transparent price discovery through a high-stakes opening auction.

Choosing the Right Path to Market

Companies typically choose direct listings to broaden investor participation, reduce underwriting fees, and provide immediate liquidity to existing shareholders. However, this path requires accepting higher day-one volatility and increased execution responsibilities.

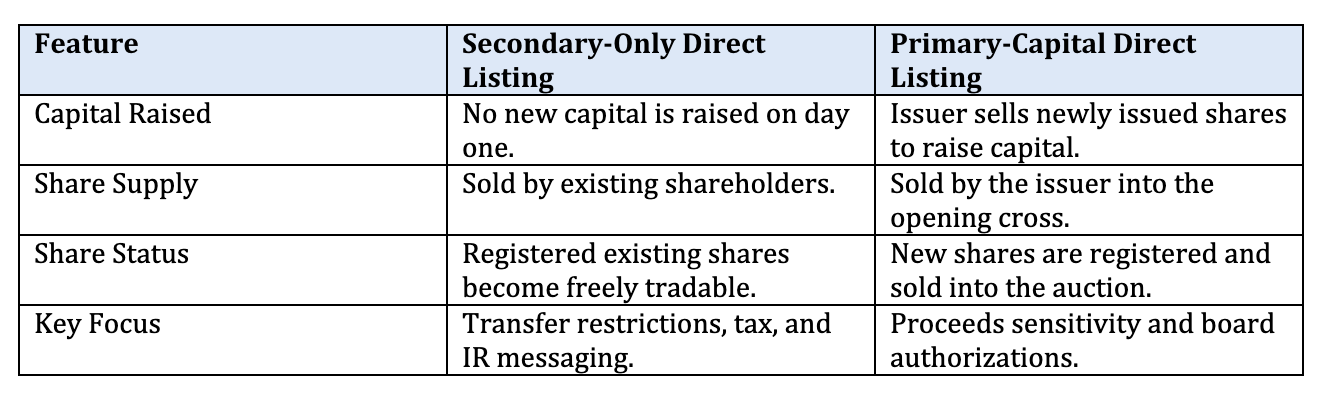

Comparison: Secondary-Only vs. Primary-Capital Listings

Nasdaq Listing Requirements

To qualify for a Nasdaq direct listing, issuers must meet both quantitative and qualitative standards.

- Quantitative Standards: Includes specific tests for public float, number of shareholders, price tests, market value, and total equity.

- Qualitative Requirements: Includes independent audit committee oversight, a formal code of conduct, and robust internal controls.

The Execution Process: Filings & Logistics

The central mechanism of a direct listing is the opening auction. Coordination between market participants, advisors, and the exchange is vital for successful price discovery.

Essential Documentation

Issuers must prepare a comprehensive suite of documents:

- Securities Act Registration Statement: Specifically tailored (S-1 or F-1) to direct listing and auction dynamics.

- Financials: PCAOB-audited financials, interim reviews, and pro forma information.

- Exchange & Regulatory: Exchange listing applications and coordination for DTC eligibility.

Integrated Timeline Sequencing

A successful launch depends on the precise sequencing of several milestones:

- SEC effectiveness of the registration statement.

- Final exchange approvals and auditor consents.

- Communications managed under Regulation FD and anti-manipulation rules.

Managing Post-Listing Liquidity and Volatility

Direct listings lack the stabilization support of traditional underwriters, often leading to wider early trading ranges.

- Communication: Strong disclosure regarding liquidity and ownership concentration is essential to align investor expectations.

- Lock-Ups: Companies must decide on company-imposed or holder lock-ups and map out affiliate sale mechanics.

- Rule 144: Careful planning is required for post-listing resale considerations.

Conclusion

By removing the traditional underwritten book-building process, issuers can achieve transparent price discovery and immediate liquidity for their stakeholders. However, the absence of a price stabilizer means companies must be prepared for heightened day-one volatility and a more rigorous internal execution load.

As the regulatory landscape evolves, the direct listing remains a powerful tool for mature companies seeking a cost-effective, democratic path to becoming a public entity.

If you are considering taking your company public or would like to speak with a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets. The firm represents clients in London, Dubai, Italy, Columbia, Malaysia, South Africa, Germany, India, France, Israel, Canada and throughout the U.S.

Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com