Quick answer: what can an issuer say during the IPO quiet period?

An issuer can usually continue factual, ordinary-course business communications during the IPO quiet period if they are consistent with past practice, directed to ordinary business audiences and do not mention the IPO, securities offering, valuation, investor demand or growth projections. Examples include routine product announcements, customer notices and factual supplier updates. The safer practice is to route all public communications through securities counsel and, once engaged, the underwriters before release.

“Talk Is Cheap — Until It Tanks Your IPO” is more than a catchy warning. In a registered IPO, IPO communications rules can be unforgiving because the legal analysis often turns on when a statement is made, who receives it, whether it is oral or written, whether a qualifying prospectus is available and whether the statement can be viewed as conditioning the market for the offering.IPO communications rules.

This article provides a practical framework for issuers, executives, investor relations teams, marketing departments and deal professionals. It covers the three major IPO communications periods, the role of Form S-1, permitted ordinary-course business communications, free writing prospectuses, Rule 163B testing-the-waters communications, investor qualification and FINRA considerations for underwritten public offerings.

Related IPO communications and Form S-1 resources

For more background, see Securities Lawyer 101 articles on Communications During an IPO, the Form S-1 registration statement quiet period, the Guide to Preparing SEC Form S-1, Testing the Waters (TTW) Under SEC Rule 163B and Free Writing Prospectus (FWP) vs. Testing-the-Waters Communications.

Why Section 5 controls the communications timeline

Section 5 of the Securities Act creates the basic registration framework. In general, a sale of securities in a registered offering cannot occur until the registration statement is effective. For SEC background, see the SEC pages on what a registration statement is, filing a registration statement and the SEC’s IPO overview. Offers and written communications before effectiveness require separate analysis because an issuer can violate Section 5 without actually completing a sale.

Official SEC resources for registration statements include SEC: What is a Registration Statement?, SEC Form S-1 and SEC EDGAR Search Filings.

For IPO planning, the key issue is not only whether the company uses the word “IPO.” The SEC may examine whether a communication, taken in context, is designed to stimulate investor interest. Statements about growth, market opportunity, revenue expectations, expansion plans, industry prospects, brand campaigns, analyst outreach or unusually timed publicity can raise gun-jumping concerns even when no price or share count is mentioned.

The practical compliance question should be: Would a reasonable reader, viewer or listener understand the communication as part of an effort to generate interest in the securities offering? If the answer may be yes, counsel should review the communication before it is released.

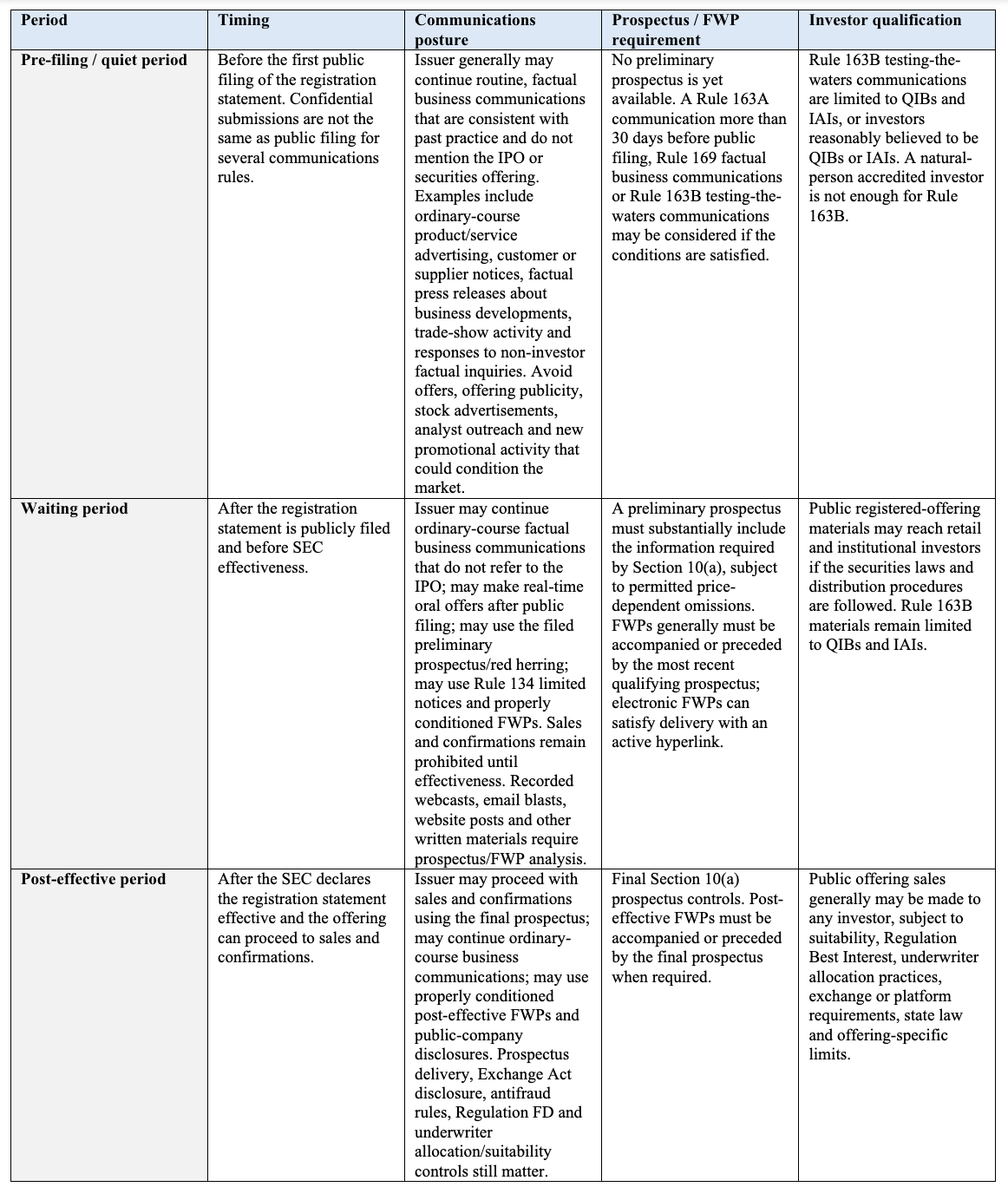

The three IPO communications periods

The most useful way to manage IPO communications is to divide the process into three periods: the pre-filing period, the waiting period and the post-effective period. The rules become progressively more permissive, but each period still has its own limits.

Chart 1 – IPO communications by period

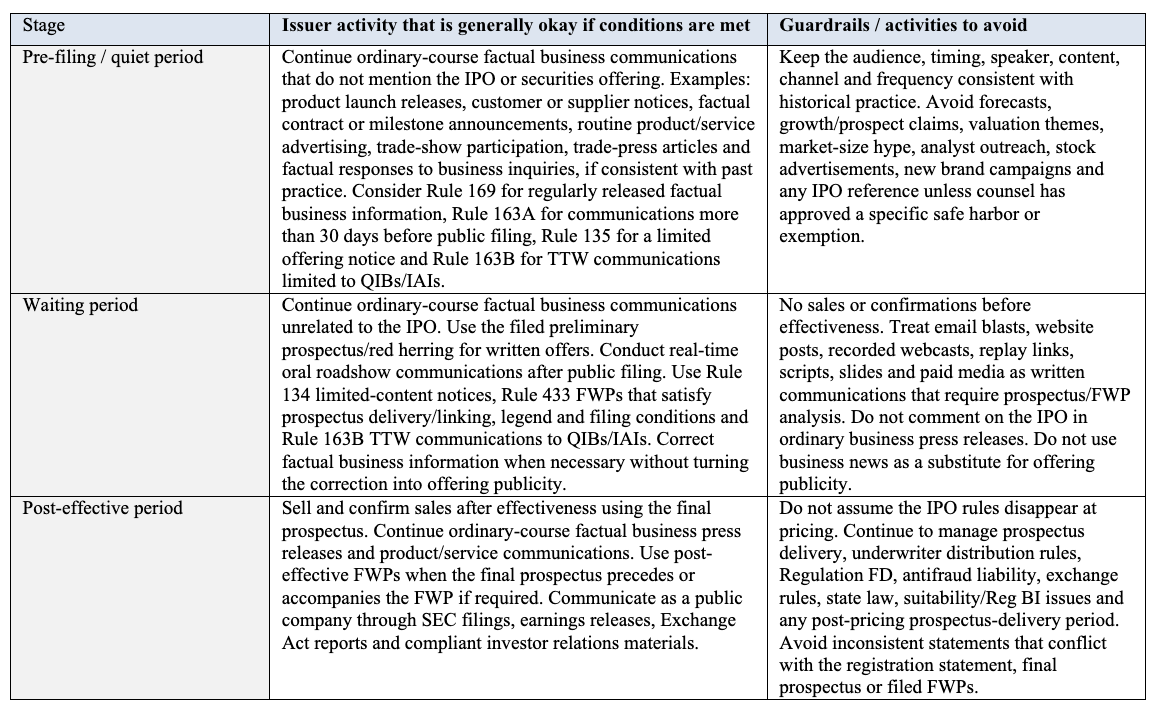

What the issuer can generally do during each stage

The issuer does not have to stop operating its business during an IPO. The safer approach is to separate ordinary-course business communications from offering communications. Ordinary business press releases, customer updates and product advertising are generally less risky when they are factual, consistent with past practice, not directed to investors as investors and do not mention the IPO, the registration statement, valuation, share price, anticipated trading market or investment merits.

The following stage-by-stage framework should be used as a practical editorial checklist. It is not a substitute for counsel review, but it helps marketing, investor relations, executives and deal teams understand what can usually continue, what must be controlled and what should be avoided.

Chart 1A – What issuers can generally do by stage

Pre-filing and quiet period: Ordinary-course business can continue

During the pre-filing period, the issuer should avoid offering-related publicity but may generally continue normal business communications. A business press release that announces a product release, customer contract, partnership, operational milestone or similar factual matter may be appropriate if it is consistent with the issuer’s past practice and does not mention the IPO, a securities offering, investor demand, valuation, growth projections or the expected trading market.

- Generally okay: ordinary product and service advertising, factual customer/supplier communications, trade-show participation, trade press, routine website updates and factual business press releases that do not mention the IPO and are consistent with past practice.

- Use extra care: new or significantly expanded branding campaigns, executive profiles, market-size articles, interviews, podcasts, award campaigns or social media pushes that begin after IPO planning starts.

- Usually avoid: references to the IPO, offering timing, valuation, share price, expected listing, investor demand, future revenues, income, growth prospects or industry growth prospects.

Waiting period: Offers may be made, but sales cannot occur

After the registration statement is publicly filed and before effectiveness, the issuer has more flexibility, but the form of the communication matters. Real-time oral offers may be permitted, while written materials generally need to be a statutory prospectus, a Rule 134 notice, a properly conditioned FWP or another communication fitting a specific rule. The issuer may still issue ordinary-course factual business press releases that do not mention the IPO, but the review should be stricter because the company is actively in the market with a pending registration statement.

- Generally okay: a filed preliminary prospectus/red herring, live roadshow presentations, real-time oral communications, properly limited Rule 134 notices, properly conditioned FWPs, Rule 163B TTW limited to QIBs/IAIs and ordinary-course factual business communications unrelated to the IPO.

- Use extra care: website updates, emails, media interviews, webcast replays, recorded presentations, social media posts, paid articles and sponsor content, because they may be written offering materials or media FWPs.

- Not okay: sales, confirmations or acceptance of binding purchase commitments before SEC effectiveness.

Post-effective period: sales can proceed, but disclosure controls remain important

Once the SEC declares the registration statement effective, sales and confirmations may proceed using the final prospectus. The issuer can continue ordinary business communications and public-company disclosures, but it should avoid inconsistent statements and should continue to coordinate with underwriters and counsel during any required prospectus-delivery period.

Where a FINRA member participates in the IPO, deal teams should also consider FINRA Public Offerings, FINRA Rule 5110 on corporate financing and underwriting terms, and investor-allocation rules such as FINRA Rule 5130 and FINRA Rule 5131, where applicable.

- Generally okay: final prospectus delivery, sales confirmations, Exchange Act reporting, ordinary-course press releases, product advertising, factual business updates and properly conditioned post-effective FWPs.

- Use extra care: any communication that updates, supplements or appears inconsistent with the registration statement, final prospectus, pricing disclosure, roadshow materials or FWPs.

- Continue controls: centralized spokespeople, counsel review, disclosure committee coordination, Regulation FD controls, underwriter coordination and a complete file of communications and approvals.

Practical drafting rule for business press releases: if the release were to have been issued in the same form, at the same time, through the same channel and to the same audience, even if there were no IPO, and if it contains only factual business information without offering references or promotional investment themes, it is more likely to be acceptable. If the timing, tone, claims or distribution appear designed to increase investor interest, it should be revised, delayed or treated as an offering communication.

What counts as an offer, sale or promotional activity?

In an IPO, the communications review should cover more than formal investor presentations. The same legal issues can arise from business communications that are unusually promotional, timed around the IPO, directed to investors or picked up by the media. Written communications include traditional written materials as well as many digital communications, such as emails, website posts, broadly distributed voicemail messages and on-demand webcasts. Real-time presentations to a live audience may be treated differently from recorded or on-demand materials.

Commonly reviewed communications include press releases, blog posts, executive interviews, podcasts, conference presentations, analyst meetings, trade-show materials, advertising, corporate branding campaigns, website updates, social media posts, investor decks, customer emails, lender or partner communications and internal messages that could be leaked or forwarded.

For related discussions of IPO marketing roles, underwriter coordination and offering publicity, see Who Handles IPO Marketing? and Understanding the Role of IPO Underwriters.

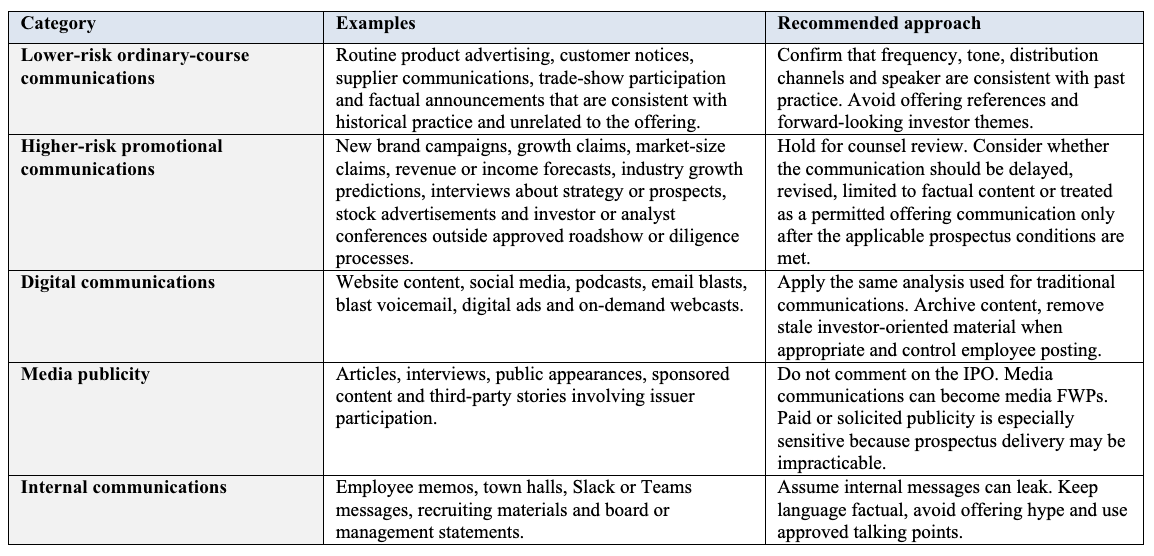

Practical rule: ordinary-course facts are safer than new promotional claims

Companies generally can continue communicating about products, services and factual business developments when those communications are consistent with past practice, are not directed at investors as investors and do not refer to the securities offering. The risk increases when the company changes the timing, tone, audience or substance of its communications after IPO planning begins.

Chart 2 – Communications risk matrix

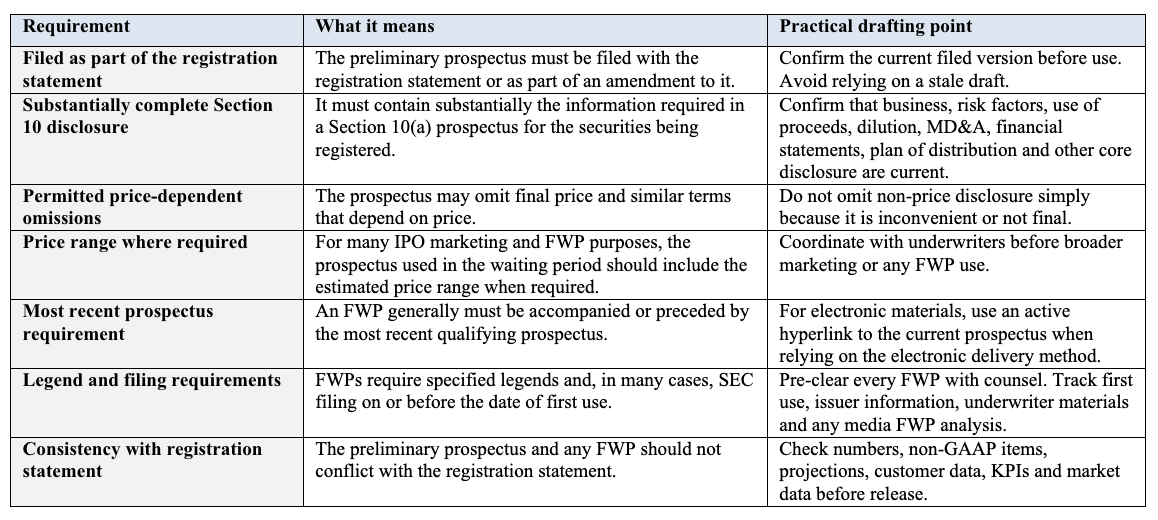

Qualifying preliminary prospectus requirements

A preliminary prospectus, often called a red herring, is central to the waiting-period communications framework. Before effectiveness, a prospectus filed as part of the registration statement can satisfy Section 10 for purposes of Section 5(b)(1) if it contains substantially the required information for the securities being registered. Certain price-dependent information may be omitted before pricing, such as the final offering price, underwriting discounts and commissions, dealer discounts and commissions, proceeds, conversion rates, call prices and other items dependent on price.

In IPO practice, the version used for marketing often includes an estimated price range once the SEC review has progressed far enough. This is important for FWPs because Rule 433 requires certain free writing prospectuses to be accompanied or preceded by the most recent prospectus that satisfies Section 10, including a price range where required by rule.

Chart 3 – Qualifying preliminary prospectus checklist

Free writing prospectuses and written offering materials

A free writing prospectus, or FWP, is a written communication that constitutes an offer but is not itself a statutory prospectus. Examples may include emails, slide decks, website posts, on-demand webcasts, blast voicemails, term sheets, updated roadshow materials and certain media communications. Because FWPs are prospectuses under the federal securities laws, they carry liability concerns and must be controlled carefully.

For related FWP guidance, see Securities Lawyer 101 resources on Free Writing Prospectus Rules for Form S-1 Registration Statements and FWP vs. Testing-the-Waters Communications. For official investor-facing examples and filing context, see SEC EDGAR Search Filings and the SEC’s registration statement resources.

An issuer should treat FWP preparation as a securities disclosure exercise, not as ordinary marketing copy. The material should be checked for consistency with the registration statement, factual support, omissions, legends, filing obligations and underwriter distribution rules. Counsel should also confirm whether the recipient already received the most recent statutory prospectus or whether an electronic hyperlink satisfies the accompanying or preceding prospectus condition.

Testing the waters under Rule 163B

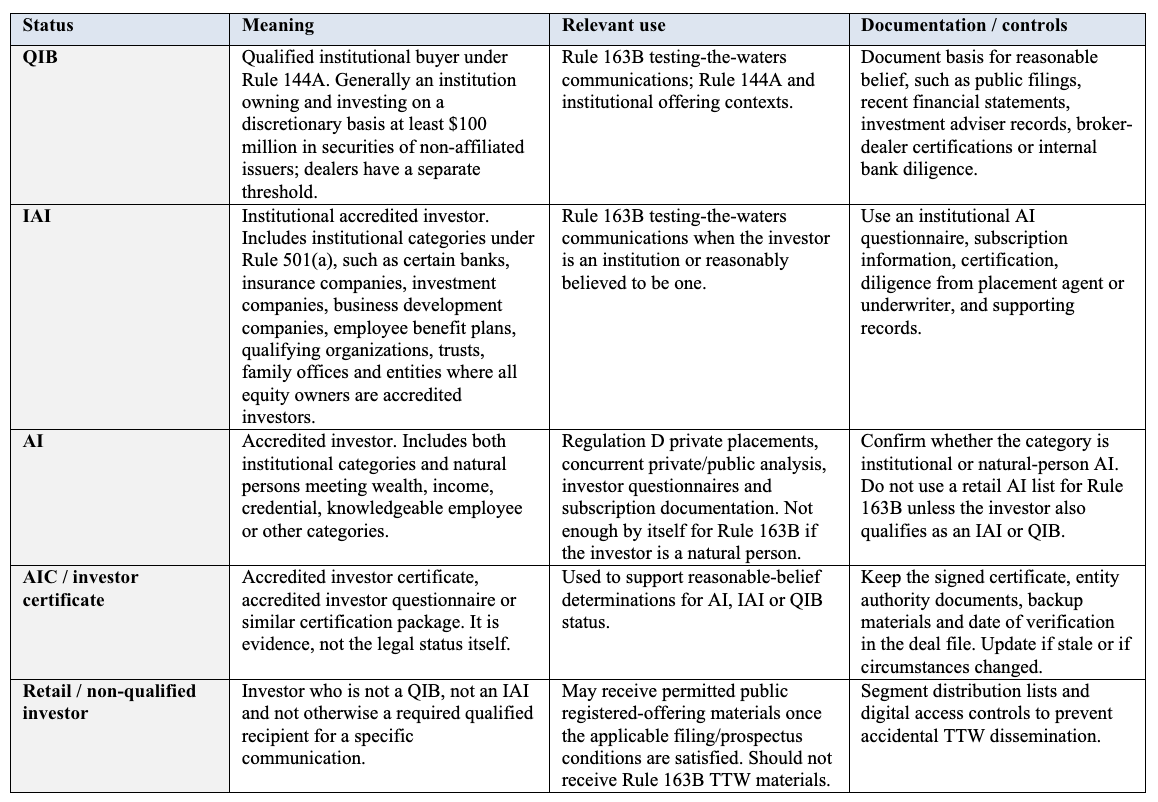

Rule 163B allows an issuer, or a person authorized to act on its behalf, to test investor interest before or after filing a registration statement. The rule is powerful because it is available to all issuers, not only emerging growth companies, but it is not a general public solicitation rule. The communications must be limited to QIBs and IAIs, or persons the issuer reasonably believes fall into those categories.

For Rule 163B background, see Securities Lawyer 101 on Testing the Waters (TTW) Under SEC Rule 163B and the SEC Small Business Compliance Guide on solicitations of interest prior to a registered public offering. The SEC explains that Rule 163B is available to all issuers and limits test-the-waters communications to QIBs and institutional accredited investors or investors reasonably believed to be in those categories.

A key compliance point is that “accredited investor” is broader than “institutional accredited investor.” A natural person who meets the income or net worth test may be an accredited investor, but that does not by itself make the person a permissible Rule 163B recipient. Rule 163B is designed for institutional recipients, and the issuer should preserve evidence supporting its reasonable belief about QIB or IAI status.

Chart 4 – Investor qualification matrix for IPO communications

AICs and investor qualification controls

An AIC or investor qualification certificate should not be treated as a substitute for legal analysis. It is a diligence tool that helps establish the issuer’s or underwriter’s reasonable belief that the recipient falls into the applicable category. The most useful certificates identify the exact status being claimed, require the investor to select the applicable category, include representations about authority and investment purpose, and require notice if the investor’s status changes before closing or before additional communications are made.

For Rule 163B testing-the-waters activity, the certificate should distinguish QIB status from institutional accredited investor status and should not rely on natural-person AI categories. For concurrent private placements, the certificate may need to address Regulation D requirements, state blue sky issues, bad actor questionnaires, investment intent, transfer restrictions and beneficial ownership information.

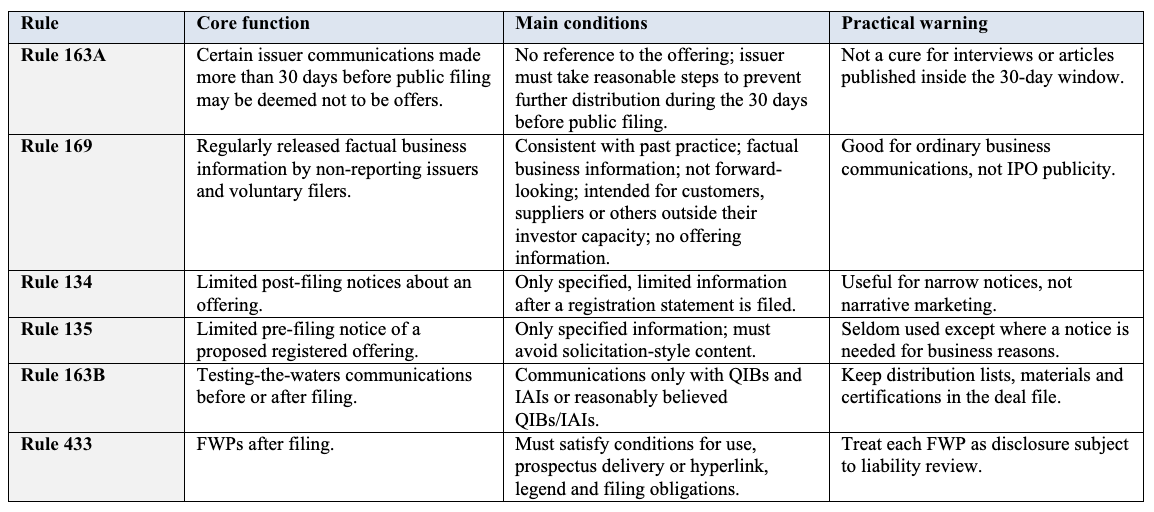

Safe harbors and limited communication tools

Several Securities Act rules allow specific communications in narrow circumstances. They are useful only when the conditions are satisfied. Issuers should avoid assuming that a safe harbor applies merely because a communication is factual or because it does not expressly mention price.

Chart 5 – Key IPO communications rules and how they fit together

Publicity, paid media and media FWPs

Publicity is one of the most common areas where securities law and marketing instincts collide. From a marketing perspective, an interview, profile or sponsored article may appear helpful. From a Securities Act perspective, a story that results from issuer participation may be analyzed as a written offering communication. If the issuer participates in a media communication that becomes an FWP, filing and liability issues may follow even if the media outlet writes the final story.

Paid publicity can be even more problematic. If a company pays for or solicits promotional coverage, the FWP and prospectus-delivery conditions may be difficult or impossible to satisfy in a compliant way. During IPO planning, media activity should be controlled by a small group of approved spokespeople and reviewed by counsel before any interview, podcast, conference panel, advertorial, sponsored content or market-facing campaign proceeds.

Roadshows, webcasts and oral versus written offers

After public filing, oral offers may generally be made during the waiting period, but the category of “oral” is narrower than many business teams expect. Live, real-time roadshow presentations to a live audience can be oral offers. Recorded, on-demand or broadly distributed materials are usually written communications and may require FWP treatment. A live webcast can raise different issues than a replay of the same webcast, because the replay is no longer a real-time oral communication.

Deal teams should decide in advance whether a roadshow, webcast or presentation will be recorded, archived, distributed by email or posted online. A communication that starts as an oral presentation can become a written communication when slides, recordings, transcripts or replays are distributed.

Recommended IPO communications policy

Every issuer preparing for an IPO should adopt a communications policy before the quiet period begins. The policy should apply to executives, directors, employees, consultants and advisors. It should also cover marketing, public relations, investor relations, recruiting, social media and internal messaging.

- Designate one or two approved spokespeople. All investor, media and analyst inquiries should be routed to them.

- Freeze unusual promotional activity. Do not launch new brand campaigns, market-size campaigns or growth-focused thought leadership without counsel review.

- Use approved talking points. Keep communications factual, ordinary-course and unrelated to the offering unless they are specifically approved offering communications.

- Review digital assets. Audit the website, social media, podcasts, executive bios, investor pages, downloadable materials and archived presentations.

- Pre-clear interviews and conferences. Media interviews, public speaking, podcasts and industry conference appearances should be reviewed in advance.

- Control testing-the-waters materials. Limit access to QIBs and IAIs, preserve investor status support and retain copies of all materials.

- Track FWPs. Record first use, legends, filing status, recipients, hyperlinks and coordination with underwriters.

- Train employees. Employees should understand that internal messages can leak and that social media commentary can create offering risk.

- Keep a communications file. Retain press releases, presentations, website screenshots, emails, scripts, ads, interview notes, approvals and distribution lists.

Common mistakes to avoid

- Assuming a confidential submission starts the waiting period. Several communication rules key off public filing, not confidential SEC submission.

- Treating all accredited investors as eligible Rule 163B recipients. Rule 163B requires QIBs or IAIs, or a reasonable belief that the recipient is one of them.

- Using an old red herring link with an updated FWP. Electronic delivery works only if the hyperlink takes investors to the most recent qualifying prospectus.

- Letting marketing continue as if nothing changed. Ordinary-course communications are safer when they are genuinely ordinary, not newly created for IPO visibility.

- Posting roadshow replays without FWP analysis. A live presentation may be oral; an on-demand replay is a written communication.

- Ignoring third-party media. An issuer-assisted article can create FWP, filing and liability issues.

- Failing to preserve records. If a question arises later, the company needs to show what was said, when it was said, who received it and why the team believed it was permitted.

Practical takeaways

IPO communications rules are manageable when a company uses a period-based framework and treats publicity as a controlled disclosure process. Before filing, the safest course is to avoid offering references and maintain ordinary-course factual communications. After public filing, oral offers and preliminary prospectus delivery become available, but written offering materials must be analyzed under the statutory prospectus and FWP rules. After effectiveness, sales can proceed, but prospectus and liability considerations still matter.

The most important operational controls are early training, centralized spokespersons, counsel pre-clearance, careful treatment of digital communications, documented investor qualification for Rule 163B activity, and a complete file of materials used during the offering process. Companies that build those controls before the IPO accelerates are better positioned to avoid gun-jumping delays, SEC comments, rescission risk and offering liability.

Suggested conclusion

An IPO changes the legal significance of ordinary business communications. A statement that would be routine in normal corporate life can become an offer, a free writing prospectus or impermissible market conditioning when made during the offering process. Issuers should map each communication to the correct offering period, confirm whether a qualifying preliminary prospectus is required, determine whether the audience must be limited to QIBs or IAIs, and document the analysis before the communication is released.

FAQ: IPO communications rules

Can an issuer issue ordinary business press releases during the IPO quiet period?

Generally, yes, if the press release is factual, consistent with past practice, intended for business audiences such as customers or suppliers, and does not mention the IPO, securities offering, valuation, investor demand or growth projections.

Can an issuer sell securities during the waiting period?

No. After public filing and before SEC effectiveness, offers may be permitted if made properly, but sales and confirmations must wait until the registration statement is effective.

Who can receive Rule 163B testing-the-waters communications?

Rule 163B communications may be directed only to QIBs and institutional accredited investors, or investors the issuer reasonably believes satisfy those standards.

Is a free writing prospectus the same as a preliminary prospectus?

No. A preliminary prospectus is part of the registration statement. An FWP is a separate written offering communication that must satisfy Rule 433 conditions, including legend, filing and prospectus-delivery or hyperlink requirements when applicable.

This blog post is for general educational purposes only. It is not legal advice and does not create an attorney-client relationship. IPO communications rules are fact-specific and should be reviewed with securities counsel before any offering-related communication is made or distributed.

Hamilton & Associates Law Group, P.A. assists issuers with Form S-1 registration statements, SEC comments, going-public transactions, Nasdaq and NYSE listings, OTC Markets matters, direct public offerings, resale registrations and ongoing public-company compliance. Companies considering a registered offering should begin planning well before the desired filing date so audit, disclosure, governance and market-entry issues can be addressed before they delay the transaction.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com