Foreign companies frequently want access to U.S. investors without the time, cost and regulatory burden of becoming full SEC reporting companies. For many foreign private issuers, the most practical path is not a Nasdaq or NYSE listing and not a registered U.S. public offering. Instead, the company may seek quotation of its securities on the U.S. over-the-counter market, including OTCQX, while continuing to rely primarily on its home-country exchange filings and public disclosures.

Exchange Act Rule 12g3-2(b) is the exemption that often makes that structure possible. The rule allows a qualifying foreign private issuer to avoid registration of a class of equity securities under Section 12(g) of the Securities Exchange Act of 1934, even though its securities may be traded in the United States over the counter. For established foreign issuers listed on a non-U.S. exchange, the exemption can provide U.S. market visibility, U.S.-dollar trading and broader investor access without converting the issuer into a full SEC reporting company.

For companies seeking OTCQX, Rule 12g3-2(b) frequently serves as the bridge between home-market disclosure and U.S. market access. It does not eliminate all U.S. securities law considerations. It does not permit misleading disclosure. It does not replace OTC Markets eligibility standards. It does not make a foreign issuer immune from U.S. antifraud rules. But for the right issuer, it can provide an efficient and widely used framework for U.S. secondary market trading.

What Is Exchange Act Rule 12g3-2(b)?

Rule 12g3-2(b) is an exemption from registration under Section 12(g) of the Exchange Act for qualifying foreign private issuers. Section 12(g) can require issuers to register a class of equity securities with the SEC when they meet specified asset and shareholder thresholds. Once a class of securities is registered under Section 12(g), the issuer becomes subject to ongoing SEC reporting obligations.

For a foreign private issuer, SEC reporting can mean annual reports on Form 20-F, current reports on Form 6-K, SEC-compliant financial statements, Sarbanes-Oxley obligations and broader public company compliance. Some foreign issuers want that status because they plan to raise capital in the United States or list on Nasdaq or the NYSE. Others want U.S. OTC visibility but do not want the cost and complexity of full Exchange Act reporting.

Rule 12g3-2(b) is designed for the second category. In practical terms, it allows a qualifying foreign issuer to say: the company is already publicly traded and regulated in its primary foreign market, and it will make its material home-market disclosure available in English electronically. Because of that, the company should not have to duplicate its disclosure system by becoming an SEC reporting company solely because its securities trade in the U.S. OTC market.

The Exemption Is Automatic, But Compliance Is Not Informal

One of the most important features of Rule 12g3-2(b) is that the exemption is generally automatic for a foreign private issuer that satisfies its conditions. Historically, foreign issuers submitted materials to the SEC to obtain the exemption. The modern rule is self-executing. No SEC order is issued and no paper submission to the SEC is required merely to claim the exemption.

That does not mean compliance is casual. An issuer relying on Rule 12g3-2(b) should maintain a written compliance file showing why it qualifies. That file should include the company’s foreign private issuer analysis, foreign listing and trading-volume analysis, evidence of English electronic disclosure, copies or links to the materials published, and confirmation that the issuer is not otherwise subject to Exchange Act reporting under Sections 13(a) or 15(d).

The rule is automatic only if the issuer actually meets the rule. If it does not, the issuer may be unable to rely on the exemption and may need to determine whether Exchange Act registration is required or whether another exemption is available.

Who Can Use Rule 12g3-2(b)?

Rule 12g3-2(b) is available only to a foreign private issuer. A company is not a foreign private issuer merely because it is incorporated outside the United States. The analysis depends on U.S. shareholder ownership and the issuer’s U.S. business contacts.

Generally, a foreign company qualifies as a foreign private issuer if 50 percent or less of its outstanding voting securities are held by U.S. residents. If more than 50 percent of its outstanding voting securities are held by U.S. residents, the company can still qualify only if it does not have the level of U.S. management, assets or business administration that would make it substantially similar to a domestic U.S. issuer.

This analysis matters. A company incorporated in Canada, the British Virgin Islands, the Cayman Islands, the United Kingdom, Australia or another non-U.S. jurisdiction may still fail to qualify as a foreign private issuer if its shareholder base, management, assets and business operations are too U.S.-centered. Conversely, a foreign company with meaningful U.S. investors may still qualify if it satisfies the foreign private issuer tests.

Core Eligibility Requirements Under Rule 12g3-2(b)

1. The issuer must not already be an SEC reporting company.

Rule 12g3-2(b) is not available to an issuer that is already required to file reports under Exchange Act Section 13(a) or Section 15(d). If the issuer has registered a class of securities under Section 12(b) for a Nasdaq or NYSE listing, registered a class under Section 12(g), or has an active Section 15(d) reporting obligation from a registered offering, it generally cannot use Rule 12g3-2(b) as a substitute for SEC reporting.

This is a common misunderstanding. Rule 12g3-2(b) is not a way for an existing SEC reporting company to stop filing reports. Deregistration and suspension of reporting obligations involve separate rules and procedures. The exemption may become relevant after a foreign private issuer properly terminates or suspends reporting and satisfies the rule’s conditions, but it is not a shortcut around active Exchange Act reporting obligations.

2. The issuer must maintain a primary foreign trading market.

The issuer must maintain a listing of the subject class of securities on one or more exchanges in a non-U.S. jurisdiction that constitute its primary trading market. The purpose is to ensure that the issuer is genuinely a foreign public company with an active non-U.S. market, not a U.S.-focused issuer trying to avoid U.S. reporting.

A foreign listing that exists only in form, while actual trading is concentrated in the United States, may not satisfy the rule. The SEC’s foreign issuer guidance describes the primary trading market concept by reference to non-U.S. markets representing more than 55 percent of worldwide trading volume. For that reason, trading-volume analysis is an important part of the Rule 12g3-2(b) file.

3. The issuer must publish material non-U.S. disclosure documents electronically in English.

The issuer must publish in English, on its website or through an electronic information delivery system generally available to the public in its primary trading market, material information that it makes public under home-country law, files with its principal foreign exchange, or distributes to security holders.

The disclosure obligation is not limited to annual reports. It includes material home-market disclosure documents such as annual financial statements, interim financial reports, press releases, notices of shareholder meetings, material event disclosures, changes in management, changes in control, acquisitions or dispositions, securities issuances and other information made public in the issuer’s home market.

The English-language requirement is critical. A foreign issuer cannot rely on the exemption while leaving U.S. investors to search for untranslated disclosure in another language. The issuer must make relevant disclosure electronically available in English.

What Rule 12g3-2(b) Does Not Do

- It does not register securities for resale. The exemption is an Exchange Act registration exemption, not a Securities Act registration statement.

- It does not permit a U.S. public offering. A registered U.S. offering generally requires an appropriate Securities Act registration statement, such as Form F-1, Form F-3 or Form F-4.

- It does not allow listing on Nasdaq or the NYSE without SEC registration. A U.S. national securities exchange listing requires Exchange Act registration.

- It does not eliminate antifraud liability. Public statements, websites, investor materials and OTC Markets disclosures must be accurate and not misleading.

- It does not automatically satisfy OTCQX eligibility. OTCQX imposes its own financial, market, shareholder, float, quotation, disclosure and qualitative standards.

Rule 12g3-2(b) and OTC Markets

The U.S. OTC market provides a trading venue for securities that are not listed on a U.S. national securities exchange. For foreign issuers, OTC Markets can create U.S. visibility and secondary trading without requiring a full U.S. exchange listing.

OTC Markets operates multiple market tiers. For established foreign issuers, the most important tier is often OTCQX, the highest OTC Markets tier. OTCQX is designed for companies that meet higher financial and disclosure standards and that are current in their reporting obligations.

For foreign issuers, OTCQX can be attractive because it allows the company to combine its home-market listing with a U.S. trading platform. U.S. investors can obtain U.S.-dollar quotations and trade through U.S. broker-dealers, while the issuer continues to rely on its primary foreign disclosure system.

How Rule 12g3-2(b) Supports OTCQX International Eligibility

A foreign issuer listed on a Qualified Foreign Exchange may be able to qualify for OTCQX without becoming an SEC reporting company if it is exempt from SEC registration under Rule 12g3-2(b) and meets OTCQX’s other standards.

This is the central practical benefit of the rule for many international companies. OTCQX recognizes that a foreign company may already be subject to public disclosure and exchange regulation in its home market. Rather than requiring every foreign issuer to become SEC reporting, OTCQX permits certain foreign issuers to rely on home-market disclosure, provided that the issuer makes required materials available in English and satisfies OTCQX eligibility criteria.

- Confirm that the issuer is a foreign private issuer.

- Confirm that the issuer is listed on a Qualified Foreign Exchange.

- Confirm that the foreign exchange is the issuer’s primary trading market.

- Confirm that the issuer is not already subject to Exchange Act reporting under Sections 13(a) or 15(d).

- Publish required home-market disclosure in English.

- Submit the OTCQX application and required certifications.

- Satisfy OTCQX financial, shareholder, bid price, market capitalization, float, quotation and disclosure standards.

- Continue to publish ongoing disclosure through OTCIQ and required public disclosure channels.

Current OTCQX International Requirements to Consider

Reporting status

An international company generally must be listed on a Qualified Foreign Exchange and current in its reporting obligations. It must also fit within an acceptable reporting-status category, such as being exempt from SEC registration under Rule 12g3-2(b), otherwise exempt from SEC registration, an SEC reporting company, or a Regulation A reporting company. For the classic non-SEC-reporting foreign issuer, the Rule 12g3-2(b) path is often the cleanest and most direct.

Financial standards

OTCQX is not designed for distressed, shell or low-quality issuers. International companies must meet financial standards intended to exclude issuers that do not meet minimum operating or financial thresholds. An issuer may need to show net tangible assets, revenue, market value or other financial criteria based on audited financial statements. Annual financial statements must be audited and the audit opinion cannot be adverse, disclaimed or qualified.

No bankruptcy and no shell company status

OTCQX excludes companies in bankruptcy or reorganization proceedings and generally excludes shell companies and blank-check companies, subject to limited SPAC-related provisions. This matters for foreign issuers with a legacy trading history, minimal operations or restructuring background.

Public float and shareholder requirements

OTCQX requires meaningful public distribution. Current international standards include public float and shareholder requirements for each class of securities to be traded on OTCQX. These requirements are designed to support a real public market rather than a thinly held or insider-dominated security.

Bid price and market capitalization

OTCQX imposes minimum bid price and market capitalization standards. A home-market listing does not automatically qualify a company for OTCQX. The issuer must meet OTCQX’s market-based thresholds and maintain ongoing standards after admission.

Market maker quotations

OTCQX trading requires proprietary priced quotations by market makers on OTC Link ATS. Companies may phase in the market maker requirement under current rules, but they must have appropriate broker-dealer quotation support. Rule 12g3-2(b) does not itself create a quoted market.

Ongoing disclosure

An OTCQX international company relying on Rule 12g3-2(b) must remain current with the rule and must publish required information in English through OTCIQ on an ongoing basis. OTCQX also requires ongoing certification and company profile verification.

OTCQX Does Not Make the Issuer SEC Reporting

A common question is whether a foreign issuer becomes SEC reporting merely by being quoted on OTCQX. The answer is no, not if the issuer is properly relying on Rule 12g3-2(b) or another available exemption and is not otherwise subject to Exchange Act reporting.

OTCQX quotation is not the same as a Nasdaq or NYSE listing. Nasdaq and NYSE are U.S. national securities exchanges. OTCQX is an OTC Markets tier. A foreign issuer quoted on OTCQX under Rule 12g3-2(b) can remain outside the SEC periodic reporting system, provided it continues to satisfy the exemption and OTCQX requirements.

That said, the issuer is still operating in the U.S. securities market. It should maintain accurate public disclosure, monitor its U.S. investor base and trading activity, comply with applicable U.S. securities laws, and coordinate with counsel before capital raising, investor relations campaigns, Regulation S offerings, Rule 144 matters, ADR programs or material corporate transactions.

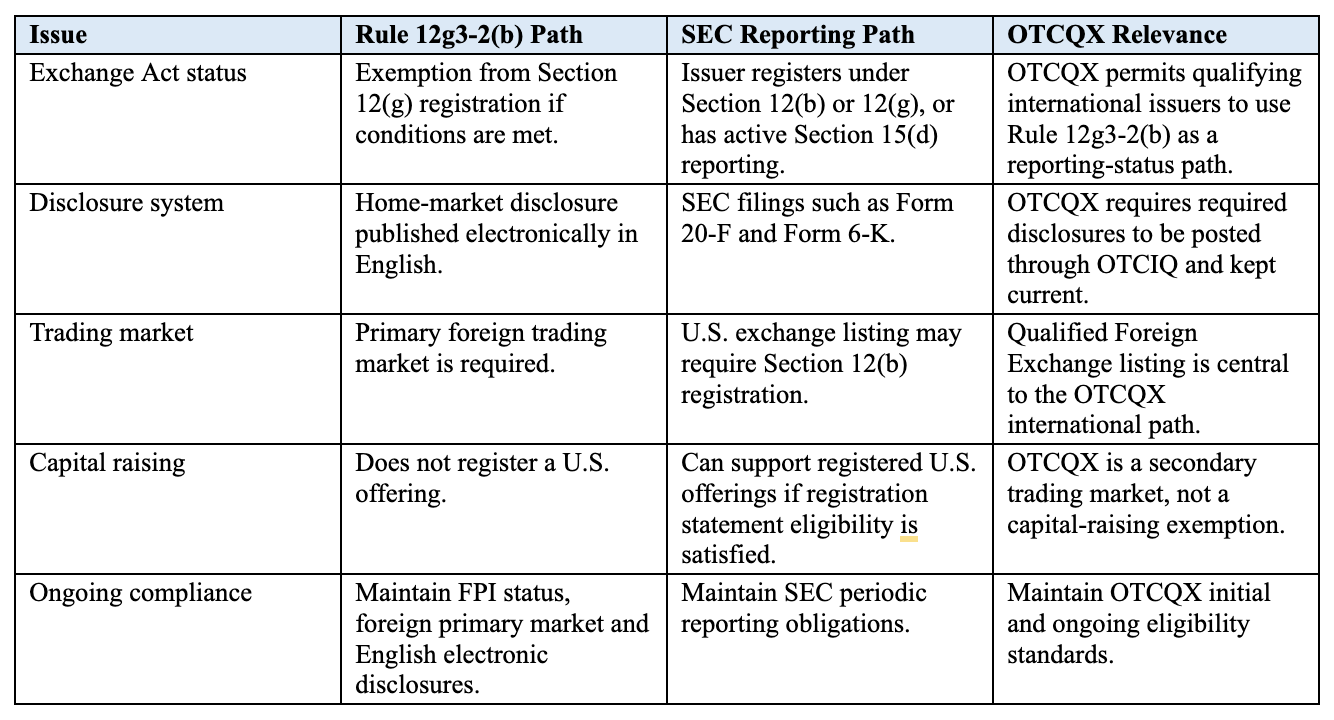

Comparison Chart

Rule 12g3-2(b), ADRs and U.S. Investor Access

Rule 12g3-2(b) is also important for American Depositary Receipt programs, particularly Level I ADR programs traded over the counter. ADRs allow U.S. investors to hold depositary receipts representing foreign ordinary shares. These programs are often used by foreign companies that want U.S. investor access without a U.S. exchange listing.

A sponsored Level I ADR program typically involves cooperation between the foreign issuer and a depositary bank. An unsponsored ADR program may be established without the issuer’s direct participation. In both contexts, the availability of English-language public disclosure is important because investors and market participants need access to material issuer information.

Foreign issuers should understand the relationship among OTC quotation, ADR facilities, depositary arrangements and Rule 12g3-2(b). Even where the issuer is not sponsoring an ADR facility, the existence of U.S. trading can affect investor relations, disclosure practices and monitoring obligations.

Practical Compliance Checklist for Foreign Issuers

Foreign private issuer status: Confirm the issuer qualifies as a foreign private issuer. Review U.S. ownership of voting securities, U.S. record holders, nominee accounts, directors, officers, assets, headquarters and principal business administration.

Exchange listing: Confirm the issuer maintains a listing of the relevant class of securities on a foreign exchange and that the foreign exchange is acceptable for the intended OTC Markets tier.

Primary trading market: Confirm that the foreign market or markets represent the required majority of worldwide trading volume. Prepare a trading-volume analysis using reliable data.

SEC reporting status: Confirm that the issuer is not required to file reports under Exchange Act Sections 13(a) or 15(d). Review prior U.S. registered offerings, Exchange Act registrations, Form F-1 or Form F-3 filings, Form 20-F history, Form 15 or Form 15F filings and any deregistration history.

English disclosure: Confirm that material home-market disclosures are available in English electronically. Maintain a process for prompt translation or English preparation of annual reports, interim reports, press releases, meeting materials and material event disclosures.

OTCQX eligibility: Confirm that the issuer satisfies OTCQX financial standards, bid price, market capitalization, shareholder, public float, audit, good standing, no bankruptcy, no shell company and quotation requirements.

OTCIQ process: Prepare the OTCQX application materials, certifications, background check authorizations, shareholder information, company profile and required disclosure uploads through OTCIQ.

Ongoing compliance calendar: Create a compliance calendar for home-market reports, English translations, OTCIQ uploads, annual certifications, company profile verification, press releases, shareholder meetings and corporate action notices.

Common Mistakes Foreign Issuers Make

Assuming any foreign listing is enough: A foreign listing alone does not automatically satisfy Rule 12g3-2(b) or OTCQX. The issuer must analyze whether the foreign market is its primary trading market and whether the exchange qualifies under OTCQX standards.

Ignoring English disclosure: The rule requires English-language electronic disclosure. A company cannot rely on untranslated home-market materials and assume U.S. investors can locate or interpret them.

Treating OTCQX as a capital-raising transaction: OTCQX provides a secondary trading market. It does not itself raise capital. If the issuer wants to sell securities into the United States, it must separately analyze Securities Act registration or exemption requirements.

Overlooking prior SEC reporting obligations: Some foreign issuers previously filed with the SEC, completed a registered offering, or had a class registered under the Exchange Act. Those facts must be reviewed carefully. Rule 12g3-2(b) is not available while active Exchange Act reporting obligations remain.

Failing to monitor U.S. trading volume: A foreign issuer relying on Rule 12g3-2(b) should monitor where its securities trade. If U.S. trading becomes too significant relative to foreign trading, the issuer may need to revisit its primary trading market analysis.

Forgetting ongoing OTCQX obligations: OTCQX admission is not the end of the process. The issuer must maintain ongoing eligibility, disclosure, quotation and certification obligations. Failure to do so can result in compliance issues, suspension or removal from OTCQX.

Why Rule 12g3-2(b) Matters for Foreign Issuers

Rule 12g3-2(b) matters because it recognizes the reality of global capital markets. Many foreign companies are already public, already regulated and already filing extensive disclosure in their home markets. Requiring every such company to duplicate that disclosure under the U.S. reporting system solely to permit U.S. OTC trading would discourage cross-border market access and reduce investment opportunities for U.S. investors.

The rule provides a balanced approach. It gives U.S. investors access to material English-language disclosure while allowing qualifying foreign issuers to avoid unnecessary duplication. It also supports OTCQX as a market for established international companies seeking U.S. visibility without the expense and complexity of a U.S. national securities exchange listing.

- broader access to U.S. investors;

- increased visibility in the U.S. capital markets;

- U.S.-dollar trading;

- potential liquidity support;

- enhanced investor relations;

- a lower-cost alternative to Nasdaq or NYSE listing;

- continued reliance on home-market disclosure; and

- avoidance of full SEC reporting where the exemption is available.

When a Foreign Issuer Should Consider SEC Reporting Instead

Rule 12g3-2(b) is not right for every foreign issuer. Some companies should consider SEC registration or a U.S. exchange listing if their business plan requires it.

SEC reporting may be appropriate where the issuer wants to conduct a registered U.S. public offering, list on Nasdaq or the NYSE, use registered securities for acquisitions, access a broader institutional investor base, or establish a more robust U.S. capital markets profile.

The decision should be strategic. OTCQX with Rule 12g3-2(b) may be ideal for an established foreign issuer that wants U.S. secondary trading and visibility. SEC reporting may be better for an issuer seeking primary capital formation in the United States or a national exchange listing.

Conclusion

Exchange Act Rule 12g3-2(b) is one of the most important exemptions available to foreign private issuers seeking U.S. OTC market access. It allows qualifying foreign issuers to avoid Section 12(g) registration while making their home-market disclosure available to U.S. investors in English.

For OTCQX International companies, the rule can be especially valuable. A foreign issuer listed on a Qualified Foreign Exchange may be able to trade on OTCQX without becoming an SEC reporting company, provided it qualifies under Rule 12g3-2(b), publishes required disclosures, and satisfies all OTCQX eligibility and ongoing compliance standards.

The key is careful planning. Foreign issuers should not treat Rule 12g3-2(b) as a box-checking exercise. They should confirm foreign private issuer status, primary trading market, English disclosure procedures, SEC reporting history, OTCQX eligibility and ongoing compliance obligations before entering the U.S. OTC market. Used correctly, Rule 12g3-2(b) offers foreign issuers a practical, efficient and legally recognized path to U.S. market visibility without the burdens of full SEC reporting.

This article is for general informational purposes only and does not constitute legal advice. Companies should consult qualified securities counsel before relying on Rule 12g3-2(b), seeking OTCQX quotation, conducting U.S. securities offerings, or making public disclosures to U.S. investors.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com