Lawmakers seek ticker warnings and 10-business-day trading suspensions, but a temporary SEC suspension can become a practical death sentence for a stock.

U.S. Senator Rick Scott and Representative John Moolenaar have asked Securities and Exchange Commission Chairman Paul Atkins to restrict access to U.S. capital markets by Chinese companies identified on federal national-security lists. Their July 16, 2026 letter requests a standardized ticker-level warning and the use of the SEC’s existing authority to impose a ten-business-day trading suspension when a covered company is added to a U.S. government list.

The request raises a question with consequences far beyond the ten days stated in Exchange Act Section 12(k): Can a temporary SEC suspension function as a permanent market penalty? In many cases, particularly for an OTC security, the answer is yes. An SEC suspension is not a routine exchange halt. It can destroy liquidity, trigger broker restrictions, strand existing shareholders, derail financing and corporate transactions, and leave a security trading only in an opaque grey market. For a large foreign issuer with an active overseas listing, the operating company may survive, but the U.S.-traded ADR can still suffer severe and lasting damage.

Key Takeaways

What Scott and Moolenaar Asked the SEC to Do

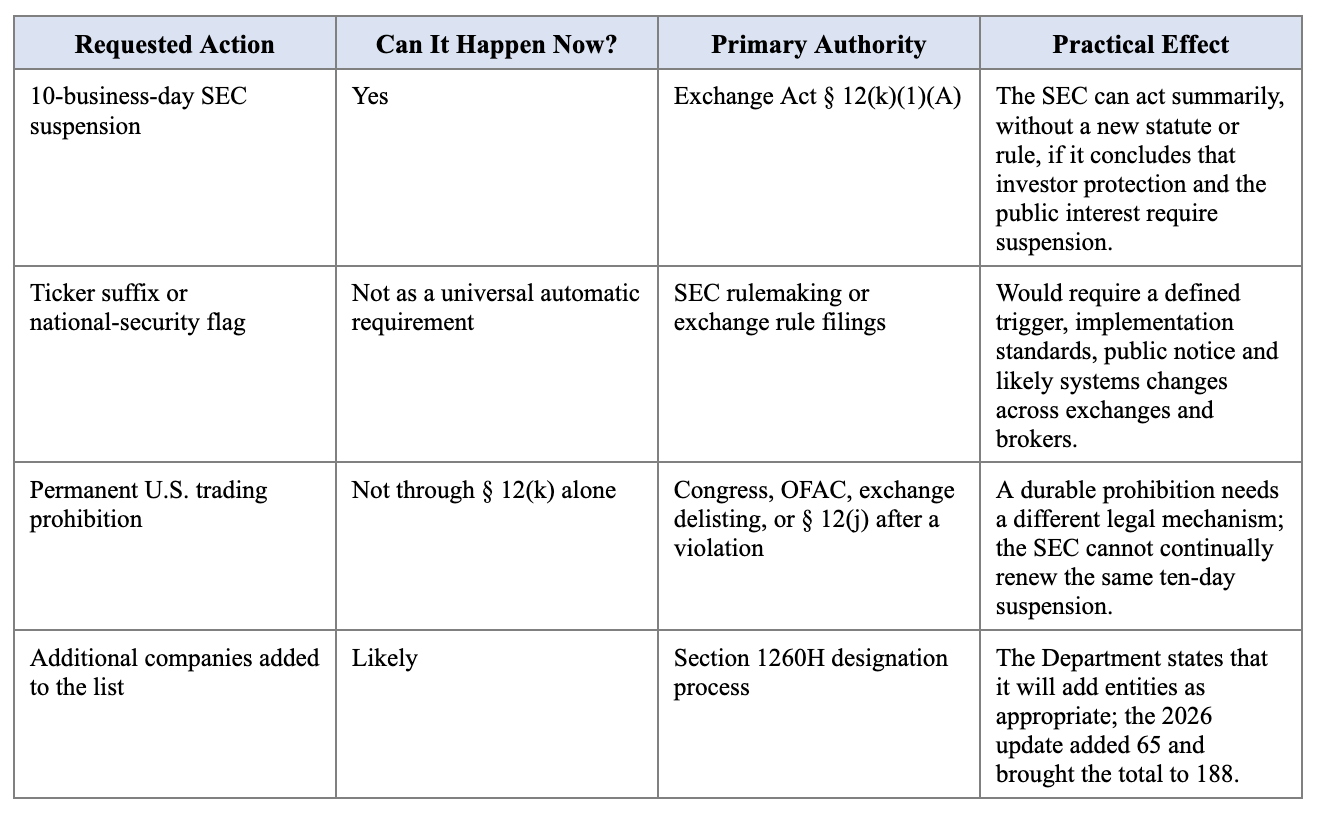

The lawmakers asked the SEC to take two different actions within 60 days. The first would require rulemaking. The second could theoretically be implemented immediately under existing law.

- Begin a notice of proposed rulemaking that would require national securities exchanges to append a standardized suffix or flag to the ticker symbol of a covered issuer within 30 days after its designation on a U.S. government list. The letter also proposes prominent disclosure in Forms 20-F and 6-K and asks the SEC to consider comparable treatment for OTC-traded ADRs.

- Use Exchange Act Section 12(k) to suspend trading for ten business days when a company headquartered in, or beneficially owned by an entity or government of, a foreign country of concern is added to a covered government list.

The letter names Alibaba Group Holding Limited, NIO Inc., Baidu Inc. and Hesai Group as exchange-listed examples. It also identifies BYD Company Limited and Tencent Holdings Limited, whose ADRs trade in the OTC market. The lawmakers describe the proposed suspension as a way to permit the SEC to evaluate permanent action while making clear to the market that a designation has consequences.

A Section 1260H Designation Is Not Automatically an OFAC Trading Sanction

The first legal distinction is critical. Inclusion on the Department of War’s Section 1260H list does not, standing alone, prohibit U.S. investors from buying or selling the company’s securities. The designation identifies an entity that the Department has determined meets the statutory definition of a Chinese military company. It may produce contracting, procurement, research-funding, supply-chain and reputational consequences, but it is not automatically equivalent to an OFAC blocking sanction or an investment prohibition.

Different federal lists create different legal consequences. An entity on OFAC’s Specially Designated Nationals and Blocked Persons List is generally subject to blocking sanctions. An entity specifically covered by the Non-SDN Chinese Military-Industrial Complex Companies program may be subject to restrictions on purchases and sales of publicly traded securities and related instruments. A Section 1260H designation, by contrast, does not itself create a blanket securities-trading ban.

That distinction matters because a ticker-level label using the single word “sanctioned” could overstate the law. A workable SEC rule would need to identify the designating agency, the precise list, the effective date, whether transactions are prohibited or merely discouraged, whether divestment is permitted, whether affiliates are covered, and whether the designation is subject to reconsideration or litigation.

Can the SEC Suspend These Companies Without a New Rule or Law?

Yes. Exchange Act Section 12(k)(1)(A), 15 U.S.C. § 78l(k)(1)(A), authorizes the SEC, if in its opinion the public interest and the protection of investors require it, to summarily suspend trading in any nonexempt security for a period not exceeding ten business days.

The SEC does not have to prove fraud or establish another securities-law violation before using Section 12(k). In its 2020 Apotheca Biosciences opinion, the Commission stated that Congress granted it broad discretion, that it may suspend trading without determining that an issuer violated the securities laws, and that the inquiry turns on the Commission’s opinion concerning investor protection and the public interest.

The SEC may act without advance notice, a pre-suspension hearing or findings developed in a formal evidentiary record. An issuer may file a petition under SEC Rule of Practice 550, but the ten-day period often expires before that challenge can be resolved. In practical terms, the market consequences can occur before the issuer receives meaningful review.

What Would the SEC Need to Say in a Suspension Order?

A designation alone might be asserted as sufficient under the broad statutory language, but it would present a more vulnerable and controversial use of Section 12(k). Section 12(k) is an investor-protection and market-protection provision, not an unrestricted national-security power. The SEC would have a stronger legal and administrative record if it connected the designation to specific market concerns, including:

- A lack of current, accurate or complete disclosure regarding the designation and its consequences;

- Material uncertainty about whether brokers, custodians, clearing agencies or ADR depositaries can lawfully process transactions;

- Conflicting statements about whether the company is actually subject to an investment prohibition;

- Abnormal trading, unusual volatility, suspicious promotional activity or potential manipulation following the designation;

- A need to permit investors to receive and evaluate material information before trading continues;

- A pending OFAC action, exchange proceeding, ADR termination or other development that may materially change the security’s legal status; or

- A threat to fair and orderly markets caused by inconsistent broker-dealer treatment or uncertainty about clearance and settlement.

A blanket policy that automatically suspends every company solely because another agency placed it on a list would create a different question. The Commission would still need to exercise the judgment Congress assigned to it. It could not simply treat another agency’s designation as a conclusive substitute for the SEC’s own investor-protection determination without risking challenge under the Exchange Act and the Administrative Procedure Act.

An SEC Ten-Day Suspension Is Often the “Kiss of Death” for a Stock

Calling the order “temporary” understates its economic impact. A Section 12(k) suspension is often the kiss of death for a security, particularly for an OTC stock. The SEC itself has acknowledged that suspension orders have significant consequences and that the practical effects can be difficult to undo once imposed.

In the Apotheca proceeding, the issuer described the suspension as a “kill-switch” that caused irreversible damage and the loss of shareholder equity. The SEC did not accept that harm as a basis for vacating the order, but it did not deny that a suspension can inflict serious collateral consequences. Instead, the Commission emphasized that it weighs those consequences against the interests of prospective investors and the public.

Why the Damage Is Usually Most Severe for OTC Securities

For an OTC security, the end of the ten-day statutory period does not mean that a normal market reappears on day eleven. After a suspension lasting more than four business days, a broker-dealer generally cannot reinitiate quotations without satisfying Exchange Act Rule 15c2-11. That commonly requires a Form 211 submission to FINRA or a qualified interdealer quotation system determination, current and reliable issuer information, and a reasonable basis for believing that the information is accurate in all material respects.

The SEC’s 2020 amendments to Rule 15c2-11 also prevent reliance on the piggyback exception during the first 60 calendar days following termination of an SEC trading suspension. Even where unsolicited transactions remain possible, the security may trade only in the grey market, without ordinary displayed quotations, reliable price discovery or meaningful liquidity.

The consequences can include:

- Market makers refusing to sponsor or resume quotations;

- Broker-dealers prohibiting purchases and allowing only liquidating sales;

- Large bid-ask spreads and erratic executions;

- Loss of DTC, clearing, custody or margin support;

- The collapse of planned financings, acquisitions or uplisting efforts;

- Inability of shareholders to obtain a reliable market price;

- Migration to the grey market or Expert Market; and

- A persistent market assumption that an undisclosed enforcement action is coming.

For a thinly traded OTC issuer, that combination can be fatal even if the company remains in business and even if the SEC never files an enforcement action. The stock may technically continue to exist while becoming commercially untradeable.

Exchange-Listed ADRs Are Stronger, but They Are Not Immune

Exchange-listed securities generally resume trading when the Section 12(k) period expires, unless the exchange, OFAC or another authority imposes a separate restriction. That makes a large NYSE- or Nasdaq-listed ADR materially different from a microcap OTC stock. Alibaba, Baidu or NIO would not necessarily disappear as operating companies merely because U.S. trading was suspended for ten business days.

Even so, the U.S.-traded security could suffer severe harm. A suspension involving a national-security designation would likely be interpreted as a precursor to OFAC restrictions, delisting, forced divestment or ADR termination. During the suspension, price discovery could continue in Hong Kong or another foreign market while U.S. holders remain unable to trade. When the ADR reopens, it could gap sharply to the foreign-market price, with U.S. investors absorbing the adjustment all at once.

Other potential consequences include index deletion, mandatory sales by funds, options and derivatives disruption, increased margin requirements, loss of analyst coverage, broker-dealer restrictions, reputational damage and a permanently higher cost of capital. For a large dual-listed issuer, the ten-day order may not be a death sentence for the enterprise, but it can become a death sentence for the company’s practical access to the U.S. public market.

The Investor-Protection Paradox

A suspension intended to protect investors can impose the largest immediate loss on investors who already own the stock. Existing holders are trapped during the suspension. They cannot reduce exposure as overseas markets react, and they may face a wave of forced or panic selling when U.S. trading resumes. The suspension can therefore transfer the cost of a government policy decision directly to public shareholders, including mutual funds, pension accounts and retail investors who had no role in the conduct underlying the designation.

This effect is particularly pronounced here because the lawmakers are not requesting a neutral information pause. Their letter expressly contemplates suspension as a signal that designation carries consequences and as a bridge to possible permanent action. The market would rationally treat the order not as a ten-day event but as notice that the security may lose U.S. market access altogether.

Why the SEC Might Hesitate to Use Section 12(k) Automatically

The SEC has broad authority, but broad authority is not unlimited authority. Several considerations may cause the Commission to resist an automatic suspension policy based solely on another agency’s designation.

- Traditional Section 12(k) orders generally identify issuer-specific information, manipulation, trading, clearance or settlement concerns.

- A Section 1260H designation is not itself a finding of securities fraud, deficient disclosure or unlawful trading.

- The order could be challenged as using an investor-protection statute primarily to implement foreign policy or national-security objectives assigned to other agencies.

- A categorical policy could appear inconsistent with the case-specific care the SEC says it exercises because suspension consequences are difficult to reverse.

- The SEC would need a principled explanation for treating some federal lists as suspension triggers while excluding others.

- An automatic suspension could create unequal treatment among direct listings, ADRs, OTC securities, affiliates, subsidiaries and companies with securities traded only abroad.

- Major market disruptions could arise if several highly capitalized issuers were suspended at the same time.

The Commission could still act against an individual security under existing law. The legal risk increases when the action is transformed from a discretionary emergency measure into a standing automatic penalty imposed whenever another agency updates a list.

The SEC Cannot Keep Renewing the Same Ten-Day Suspension

Section 12(k) is not a vehicle for an indefinite ban. In SEC v. Sloan, 436 U.S. 103 (1978), the Supreme Court held that the SEC could not maintain a continuous suspension by issuing consecutive ten-day orders based on the same underlying circumstances. The summary power is an emergency measure, not a substitute for a permanent statutory or adjudicatory remedy.

A later suspension could potentially rest on genuinely new facts, such as a subsequent OFAC designation, newly discovered manipulation, a material disclosure failure or a new clearance problem. The SEC could not simply reissue the same order every ten business days because the Section 1260H designation remained in effect.

What Must Happen to Adopt the Proposed Ticker Warning?

The ticker-level warning is not something the Chair can impose permanently by letter. It would ordinarily require SEC rulemaking, exchange rule changes, or both.

Route One: SEC Notice-and-Comment Rulemaking

- SEC staff would develop a proposed rule, identify statutory authority, define the covered lists and securities, and prepare an economic analysis addressing investor protection, market efficiency, competition and capital formation.

- A majority of the Commission would vote to publish the proposal.

- The proposal would be published in the Federal Register for public comment. Exchanges, issuers, broker-dealers, investment advisers, ADR depositaries, index providers, sanctions lawyers and investors would likely submit comments.

- The SEC would evaluate the comments, revise the rule where appropriate, complete required analyses and vote on a final rule.

- The final rule would establish an effective date and compliance period for market participants to modify symbol, market-data, order-routing, custody and disclosure systems.

- Affected parties could seek judicial review in a federal court of appeals, arguing that the rule exceeds the SEC’s authority, is arbitrary and capricious, inadequately analyzes costs, or is inconsistent with the Exchange Act.

The letter’s requested 60-day period is a request that the SEC begin the process, not a realistic deadline for a fully effective final rule. A significant market-structure rule normally requires a proposal, public comment, Commission consideration and implementation work.

Route Two: NYSE and Nasdaq Exchange Rule Filings

NYSE and Nasdaq could propose their own listing, financial-status indicator or market-data rules. Under Exchange Act Section 19(b) and Rule 19b-4, the exchange would file the proposal with the SEC. The SEC would publish it for comment and approve or disapprove it under the Exchange Act. This route might be more practical for a visible status flag, but it would not automatically solve treatment of OTC ADRs, securities traded on multiple venues or instruments linked to the designated company.

Route Three: Congressional Legislation

Congress could enact the clearest and most durable solution by expressly linking specified national-security lists to U.S. securities-market consequences. A bill would need to be introduced, referred to the relevant committees, approved by the House and Senate in identical form, and signed by the President or enacted over a veto.

Legislation could define the covered issuers and affiliates, determine whether only new purchases or all transactions are prohibited, establish divestment periods, address ADRs and derivatives, authorize waivers, provide a reconsideration process and assign enforcement authority among the SEC, Treasury and the exchanges.

Route Four: OFAC or Presidential Action

The President and Treasury can use sanctions authorities to create investment restrictions that are independent of Section 12(k). If an issuer is specifically made subject to a prohibition on U.S. persons purchasing or selling publicly traded securities, broker-dealers and investment managers must comply regardless of whether the SEC adopts a ticker flag. OFAC action is therefore a more direct mechanism for restricting transactions, but it carries its own statutory, executive-order, licensing and interpretive framework.

What Could Create a Permanent U.S. Market Ban?

A lasting exclusion would require a mechanism other than repeated Section 12(k) orders. Potential routes include:

- A federal statute that prohibits trading or requires delisting when an issuer is placed on a specified list;

- An OFAC investment prohibition or blocking sanction;

- NYSE or Nasdaq suspension and delisting under an applicable exchange rule, subject to the exchange’s procedures and SEC oversight;

- Exchange Act Section 12(j), which permits the SEC, after notice and an opportunity for hearing, to suspend for up to 12 months or revoke a security’s registration when the issuer has violated the Exchange Act or its rules;

- Holding Foreign Companies Accountable Act consequences if the issuer independently satisfies that statute’s audit-inspection triggers; or

- Termination of an ADR program, loss of depositary support, or broker and custodian restrictions that make the U.S. security commercially unavailable even without a formal federal prohibition.

The Holding Foreign Companies Accountable Act is not a general national-security delisting statute. It applies through its own PCAOB inspection and identification framework. A company’s presence on the Section 1260H list does not automatically establish the conditions for an HFCAA trading prohibition.

Will More Companies Be Added?

Yes, additional designations are likely. The June 8, 2026 Section 1260H update identified 188 entities and added 65 beyond the prior list. The Department expressly stated that it will update the list with additional entities as appropriate and reserved the government’s ability to take action under authorities other than Section 1260H.

The historical pattern also points toward continued updates. The Department issued updated lists in 2024, 2025 and 2026. As intelligence, ownership structures, military-civil fusion relationships and supply-chain information develop, companies may be added, renamed, reorganized or removed.

The lawmakers’ letter also states that pending fiscal-year 2027 defense legislation would remove the geographic limitation tied to operating directly or indirectly in the United States. If enacted in that form, the eligible universe could expand to companies without the same U.S. operational nexus. That does not mean every newly eligible company would be designated, but it would broaden the pool the Department could review.

The number of U.S.-traded securities potentially affected could also exceed the number of named parent companies. A designation may raise questions involving ADRs, sponsored and unsponsored programs, subsidiaries, controlled affiliates, variable-interest-entity structures, funds, indexes, derivatives and securities listed outside the United States. Any SEC rule would need to specify whether coverage follows the exact legal name on the government list or extends through ownership and control tests.

What Public Companies and Market Participants Should Do Now

No final SEC rule or automatic suspension policy has been adopted. Nevertheless, issuers and market participants with exposure to a covered company should prepare for the possibility of rapid action.

- Confirm exactly which government lists apply and avoid using “sanctioned” as a generic term.

- Evaluate whether the designation and its expected commercial consequences are material and require Form 6-K, Form 8-K, periodic-report or risk-factor disclosure.

- Review ADR agreements, exchange rules, financing covenants, index criteria, custody arrangements and broker policies for designation or sanctions triggers.

- Prepare a trading-suspension response plan, including disclosure, investor relations, exchange communications and foreign-market coordination.

- Assess whether current public statements fully and accurately describe the designation, reconsideration rights and potential consequences.

- Map subsidiaries, controlling shareholders, affiliates and investment vehicles that could be captured by an ownership or control standard.

- Monitor Department, Treasury, SEC and exchange actions rather than assuming that a Section 1260H listing has a single fixed consequence.

Frequently Asked Questions

Can Chairman Atkins personally suspend a stock?

A Section 12(k) suspension is an order of the Commission. The Chair can influence the agenda and direct staff priorities, but the authority belongs to the SEC as a Commission rather than to the Chair acting alone in a personal capacity.

Does the SEC have to give the company advance warning?

No. Section 12(k) permits summary action. The SEC has stated that an issuer is not entitled to advance notice or a pre-suspension hearing. The absence of advance notice is intended to preserve the effectiveness of investigations and prevent insiders from trading ahead of the suspension.

Does the SEC have to prove fraud?

No. The SEC may suspend trading without first finding a securities-law violation. It must form the opinion that the public interest and investor protection require the suspension. In practice, the Commission normally identifies concerns involving information, trading, manipulation, clearance, settlement or market orderliness.

Will trading automatically resume after ten business days?

Exchange-listed securities ordinarily resume when the SEC suspension expires unless a separate exchange or governmental action prevents trading. OTC quotations do not automatically return. Rule 15c2-11, FINRA processes, broker restrictions and the 60-day limitation on the piggyback exception can leave the security without a normal quoted market.

Can the SEC suspend the same company again?

The SEC cannot continuously stack ten-day orders based on the same facts. A later order would need genuinely new circumstances or a different legal basis. Permanent action requires another mechanism.

Is a Section 1260H company automatically prohibited from raising capital in the United States?

No. The designation alone is not an across-the-board securities offering or trading prohibition. Separate sanctions, exchange, disclosure, registration, underwriter, broker-dealer and investor restrictions may nevertheless make capital raising more difficult or impossible in practice.

Conclusion

The SEC can suspend trading in a Chinese military-linked company today under existing Exchange Act Section 12(k) authority. It does not need Congress to enact a new law, and it does not need to complete a rulemaking first. But the authority lasts only ten business days and should be tied to an investor-protection or market-integrity determination rather than treated as an unrestricted foreign-policy sanction.

The economic impact can extend far beyond ten days. For an OTC security, a suspension can eliminate the quoted market and become a practical death sentence. For a major exchange-listed ADR, the issuer may survive through its foreign listing, but the U.S. security can experience a price collapse, forced selling, broker restrictions and permanent loss of market access.

That is why the proposal should not be dismissed as a temporary pause. The lawmakers are asking the SEC to use an emergency investor-protection tool as the first stage of a national-security market-access policy. Whether that policy proceeds through SEC rulemaking, exchange action, OFAC sanctions or legislation, its most immediate costs may fall on the American investors who already own the affected securities.

This article is for informational purposes only and is not investment advice. To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com