A free writing prospectus, commonly called an FWP, is a written offering communication used in a registered securities offering that is not the statutory prospectus. In an IPO, and in many other registered transactions, the statutory prospectus is the prospectus that is part of the registration statement, including a Form S-1 registration statement. The SEC’s securities offering reform framework permits issuers and other offering participants to use FWPs to communicate efficiently with investors, but only if the communication remains tethered to the filed registration statement and the rule conditions are satisfied.

In modern deal execution, FWPs appear in investor decks, term sheets, emails to investors, website communications, and certain media-related content that functions as an offer. The benefit is speed and clarity. The trade-off is that FWPs offer communications and can carry meaningful securities law liability exposure, so they require disciplined controls aligned with the registration statement disclosure package.

Filing versus effectiveness in a Form S-1 IPO

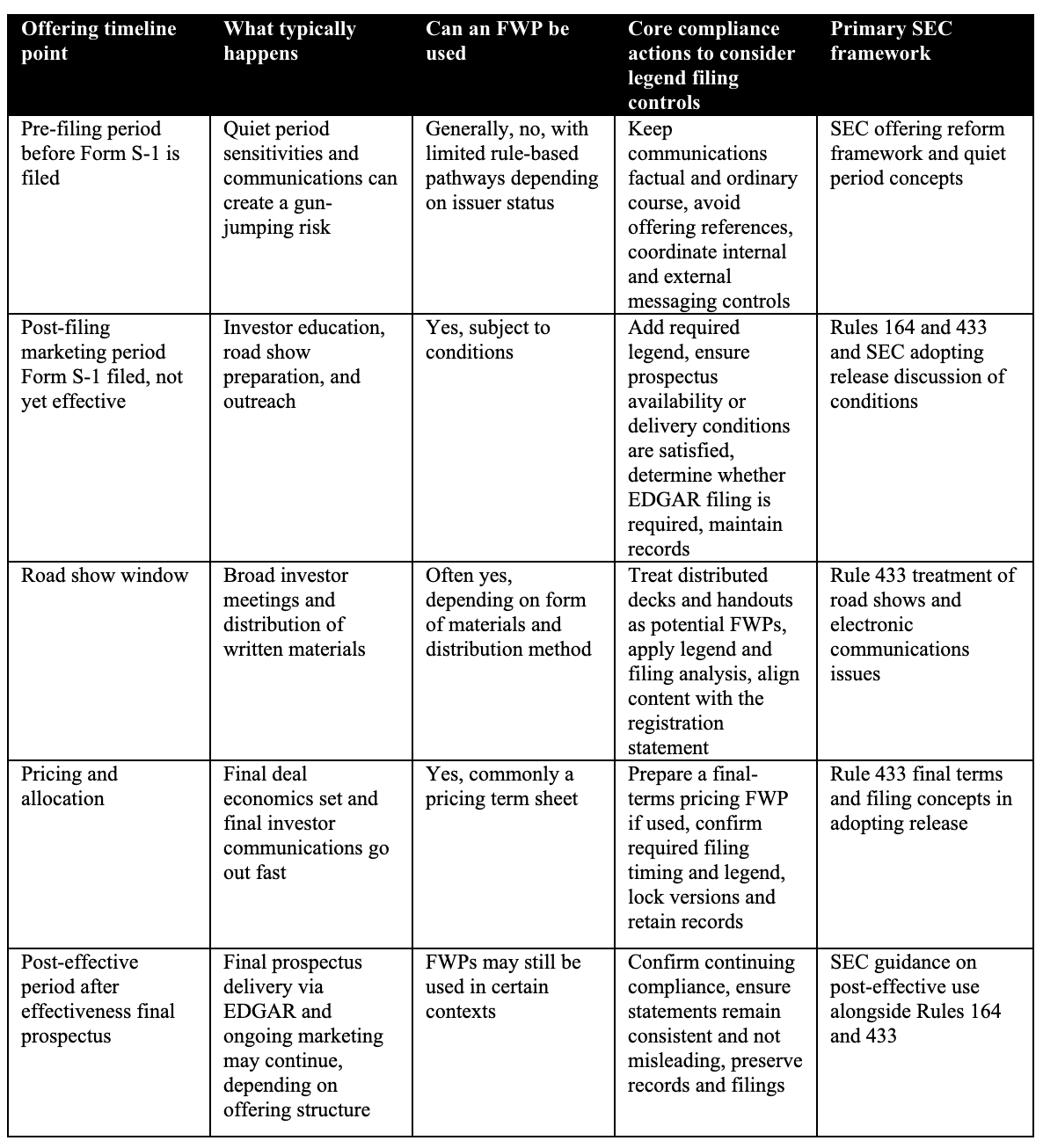

A Form S-1 filing and SEC effectiveness are distinct milestones that matter for FWP analysis. A Form S-1 is filed when the company first submits the registration statement on EDGAR. From that point until the SEC declares the registration statement effective, the offering is in the waiting period. During the waiting period, the company typically files one or more pre-effective amendments to the Form S-1 in response to SEC comments and to update the disclosure. Effectiveness occurs when the SEC declares the registration statement effective, which permits sales to be finalized and typically occurs shortly before pricing and closing in an IPO.

When this article refers to a registration statement that has been filed, it means the Form S-1 on EDGAR, including any pre-effective amendments, with a prospectus that investors can access. When this article refers to a registration statement that is effective, it is referring to the SEC effectiveness order for the Form S-1. These are separate points in time. and the SEC rules treat them differently for certain prospectus-delivery and offering-communication requirements.

What is a free writing prospectus?

A free writing prospectus is a written communication that constitutes an offer or solicitation of an offer in connection with a registered offering and is used under the SEC FWP framework rather than as the statutory prospectus. In practice, it is a supplement to the filed registration statement and prospectus, not a replacement. An FWP should not introduce a competing disclosure narrative that diverges from the Form S-1 prospectus.

What a free writing prospectus includes

FWPs are flexible in format. They can be brief or detailed, as long as they are accurate, not misleading, and used in compliance with the SEC framework for registered offerings.

Common FWP formats include investor presentations used during the road show, one pagers and investor handouts, term sheets including pricing term sheets used at pricing or shortly thereafter, written sales communications to investors such as emails or scripted electronic communications, website or other online materials that function as written offers, and certain media related written content in deal windows depending on how it is prepared and disseminated.

Substantively, FWPs often include a high-level business overview and investment highlights, selected financial information or metrics that must be balanced and consistent with the registration statement, offering terms or updates as terms evolve, and use of proceeds messaging, risk framing, and market context that remains consistent with the Form S-1 or other registration statement prospectus. FWPs typically include a legend directing investors to the registration statement and prospectus and explaining how to obtain them, often via EDGAR.

Can an FWP be used before the registration statement is effective?

Yes. An FWP may be used before the registration statement becomes effective, provided the registration statement has been filed, and the applicable conditions are satisfied. Effectiveness is not a prerequisite to using an FWP. Filing the registration statement is generally the prerequisite, as the FWP framework is designed to operate alongside a filed registration statement and related prospectus materials that investors can access during the waiting period.

Before a registration statement is filed, FWPs generally are not available. There are limited pathways for certain pre-filing written offers by well-known, seasoned issuers under Rule 163, and a separate concept of solicitations of interest under Rule 163B, testing the waters, which is not the same thing as an FWP. Because these pathways are issuer-status-dependent and fact-specific, deal teams should treat pre-filing communications as a high-risk area and use a controlled communications protocol.

After the registration statement becomes effective and the final prospectus is available, FWPs may still be used in certain offering structures, but the final Section 10(a) prospectus must precede or accompany the FWP once available, consistent with the Rule 433 framework.

What conditions must be satisfied to use an FWP in the waiting period

When this article refers to conditions for using an FWP, it means the core Rule 433 and Rule 164 compliance concepts that govern whether a written offering communication is permitted and how it must be handled. These conditions are applied to each specific written communication based on its content, timing, and distribution method.

A common condition is the required legend that tells investors that the communication relates to a registered offering and directs them to the registration statement and prospectus, including where the prospectus can be found on EDGAR. The legend is intended to keep the FWP tethered to the filed registration statement rather than functioning as a standalone marketing piece.

Another condition is the availability or delivery framework for the prospectus. In practical terms, the working group should be able to point to an accessible filed prospectus in the registration statement at the time the FWP is used, and the FWP should not be used in a way that deprives investors of access to the registration statement disclosure package.

A further condition is the EDGAR filing analysis for the FWP itself. Depending on who prepared the material and how it is disseminated, the FWP may need to be filed with the SEC on EDGAR, sometimes at or close to first use and sometimes within a short period after first use for certain final terms communications. The filing analysis is fact-specific and should be documented.

Additional conditions include record retention expectations and issuer eligibility concepts, including whether the issuer is eligible to use FWPs under the SEC framework. These gating and process conditions should be confirmed early in the transaction and then applied consistently during marketing.

SEC rules for free writing prospectuses

The SEC framework is built primarily around Securities Act Rules 164 and 433, together with related SEC staff guidance. These rules provide a pathway for written offering communications to be used in a registered offering without violating Section 5 restrictions, provided the required conditions are met.

Key compliance concepts include registration statement tethering and prospectus access, required legends, EDGAR filing analysis, record retention, and issuer eligibility concepts. These concepts should be applied to each written communication based on its content, timing, and distribution method. Short emails and one-page summaries can be FWPs if they function as written offers.

EDGAR filing requirements for FWPs and what filing refers to

When this article refers to filing requirements for FWPs, it is referring to filing the FWP itself on EDGAR under the SEC’s FWP filing regime, not filing the Form S-1 registration statement. These are separate. A company files a Form S-1 registration statement to start the registered offering process. Separately, an issuer or offering participant may have to file an FWP on EDGAR when the rules require it based on the FWP’s authorship and distribution.

At a high level, issuer-prepared FWPs are often filed, and offering participant FWPs may need to be filed when they are broadly disseminated or otherwise trigger the rule’s filing conditions. Final terms style FWPs used at pricing are commonly filed as part of the pricing and closing workflow. Because these requirements vary by deal structure and dissemination, the best practice is to treat each investor-facing written communication as a potential FWP, determine whether it is an FWP, determine who is responsible for filing, if required, and document the timing and the version used.

The filing analysis should also address whether any exception applies, including media-related scenarios where the communication is not prepared or paid for by the issuer or offering participants, and whether the substance has already been filed. These exceptions can be fact-sensitive and should be evaluated carefully.

Record retention and issuer eligibility concepts

Record retention means maintaining copies of FWPs and related distribution information in a way that supports diligence, internal controls, and any regulatory or litigation inquiry. Retention matters most when multiple versions of a deck or term sheet circulate, when marketing continues for a prolonged period, or when communications are distributed widely.

The concepts of issuer eligibility and ineligibility matter because FWP availability depends on issuer status. Eligibility should be confirmed early, and the working group should understand whether any restrictions apply to the issuer’s ability to use FWPs during the waiting period or in connection with the deal’s dissemination plan.

When free writing prospectuses are used in Form S-1 and other registered offerings

FWPs are most commonly used when the working group needs speed, clarity, or a tailored investor message while staying inside the registered offering disclosure framework. Typical use cases include IPO marketing alongside a Form S-1 registration statement to present the story in an investor friendly format while the prospectus remains the comprehensive disclosure document, road show and investor outreach where written materials supplement oral presentations, pricing communications such as a pricing term sheet, and controlled written responses to common investor questions so long as they remain consistent with the registration statement.

FWPs are also used to manage deal evolution. When offering size, price range, use of proceeds emphasis, or other marketing points change, a carefully controlled FWP can help communicate the change to investors while amendments to the Form S-1 catch up. The key is to avoid creating a parallel narrative that conflicts with the registration statement or selectively highlights favorable information.

Road show timing in a Form S-1 IPO and why it matters for FWPs

A road show is the concentrated investor marketing phase of an IPO or other registered offering, during which management and the underwriters present the investment thesis to prospective investors, answer questions, and build the order book. Road shows typically do not begin until after the registration statement is filed because road-show communications are generally treated as offers in a registered offering context.

In an IPO under Form S-1, the road show usually occurs late in the SEC review cycle, after the company has responded to a substantial portion of the SEC’s comments and the disclosure is stable enough to market. In many IPOs, the road show lasts roughly one to two weeks and typically culminates shortly before pricing and allocation. Actual timing varies with market conditions, the pace of SEC review, and the cadence of amendments to the registration statement.

Road show format affects FWP analysis. A live road show is often treated differently from a prerecorded electronic road show. A prerecorded electronic road show prepared after filing can be treated as a written communication and, therefore, may implicate the Rule 433 framework, including the legend and, in some cases, filing considerations. For this reason, working groups treat roadshow decks and written handouts as prospectus-level documents, even when delivery is primarily oral.

When a press release becomes a free writing prospectus

A press release can become an issuer FWP when it functions as a written offer in connection with a registered offering and is not otherwise excluded. This risk is highest after the registration statement is filed and during the waiting period, when communications that include offering-related selling language, deal terms, projections, or metrics framed as investment rationale, or explicit solicitation language may be viewed as conditioning the market.

Press releases are more likely to be treated as FWPs when they are prepared or distributed in a way that looks like offering conditioning rather than routine factual business disclosure during an active offering period, when they are coordinated with offering participants or involve paid placements, or when they are structured as marketing content rather than ordinary course disclosure.

A key nuance in SEC guidance is that unaffiliated, uncompensated media publications or broadcasts may raise different considerations in some contexts, but issuers should not rely on exceptions without a careful, fact-specific analysis and a clear record of the basis for the approach. The practical takeaway is that a press release during a Form S-1 process should be reviewed using the same controls applied to investor decks and term sheets, including content, timing, legend analysis, filing analysis, and consistency with the registration statement.

Compliance chart: timeline for using FWPs in a Form S-1 registration statement process

Liability that applies to free writing prospectuses

FWPs are not marketing only documents. They can trigger the same core liability regime that applies to registered offering communications. Section 12(a)(2) liability is a primary exposure point because materially false or misleading statements or omissions in a prospectus-type communication can create exposure for statutory sellers in the distribution chain, subject to defenses and fact-specific seller analysis.

Anti-fraud liability can also apply. Misstatements in FWPs can implicate anti-fraud standards, including SEC enforcement theories, especially when communications are broadly disseminated and investor-facing. The SEC has emphasized that FWPs must not be misleading and must not be used to evade Securities Act protections.

Section 11 risk via incorporation is another key concept. A filed FWP is not automatically part of the registration statement for Section 11 purposes. However, Section 11 exposure may become relevant if an FWP is incorporated or otherwise included in the registration statement disclosure package, depending on how it is used and filed.

Practical risk note: the biggest real-world liability driver is not the label. It is whether the communication is materially misleading, conflicts with the registration statement, and was distributed broadly without the required legend and filing controls.

FAQ about free writing prospectuses

Can a free-writing prospectus be used before the Form S-1 becomes effective? Yes. FWPs can be issued after the Form S-1 registration statement is filed and before the SEC declares it effective, provided the applicable conditions are satisfied.

What does filed mean in this context? Filed means the Form S-1 registration statement has been filed on EDGAR, and investors can access the registration statement prospectus. Filed does not mean effective.

What does filing an FWP mean? Filing an FWP means filing the FWP itself on EDGAR when required by SEC rules. It is separate from filing the Form S-1 registration statement.

When is the road show? The road show typically occurs after filing and late in the SEC review cycle, lasting roughly 1 to 2 weeks and culminating shortly before pricing and allocation.

Can a press release be an FWP? It can. A press release may be treated as an issuer FWP if it functions as a written offer in connection with the registered offering, particularly during the waiting period.

If you are considering taking your company public or would like to speak with a Securities Attorney, Hamilton & Associates Law Group, P.A. is ready to help. Our Founder, Brenda Hamilton, is a nationally known and recognized securities attorney with over two decades of experience assisting issuers worldwide with going public on the Nasdaq, NYSE, and OTC Markets.

Since 1998, Ms. Hamilton has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions. Whether you are taking your company public, raising capital, navigating regulatory challenges, or entering new markets, Brenda Hamilton and her team deliver the experience, strategic insight, and results-driven representation you need to succeed.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com