Overview: Nasdaq Raises the Bar for SPAC IPO Listings

Nasdaq has adopted enhanced initial listing standards for special purpose acquisition companies, commonly known as SPACs, that seek to list in connection with an initial public offering. In Nasdaq’s rules, SPACs are referred to as “Acquisition Companies.” The changes were filed with the U.S. Securities and Exchange Commission in SR-NASDAQ-2026-033 and were published by the SEC in Release No. 34-105291. Market participants can review the SEC notice for SR-NASDAQ-2026-033 and the Nasdaq rule text filed with the SEC for the official language.

The rule change is important for SPAC sponsors, underwriters, investors and private operating companies considering a de-SPAC transaction. It increases the size and liquidity thresholds for SPAC IPOs on Nasdaq, particularly for SPACs seeking to list on the Nasdaq Capital Market. For issuers planning a going-public transaction, the changes should be reviewed together with Nasdaq’s general quantitative and corporate governance standards. For additional background, see SecuritiesLawyer101’s guide to NASDAQ and NYSE initial listing requirements and its overview of going public transactions.

Although the SPAC structure remains available, the revised listing standards narrow the path for smaller or thinly distributed SPAC offerings. In practical terms, Nasdaq is signaling that SPACs should enter the public market with more capital, more public investors and greater market-maker support. That emphasis is consistent with broader SEC and exchange scrutiny of SPAC IPOs, de-SPAC transactions, shell companies, projections, conflicts of interest and public-company readiness.

What Changed Under the 2026 Nasdaq SPAC Listing Standards?

The amendments affect both the Nasdaq Global Market and the Nasdaq Capital Market. The Global Market change is relatively targeted: Nasdaq increased the Market Value of Listed Securities threshold for Acquisition Companies listing under the Market Value Standard. The Capital Market change is broader: Nasdaq created a SPAC-specific listing standard and increased the minimum public-shareholder, public-float and market-maker requirements that apply to Acquisition Companies.

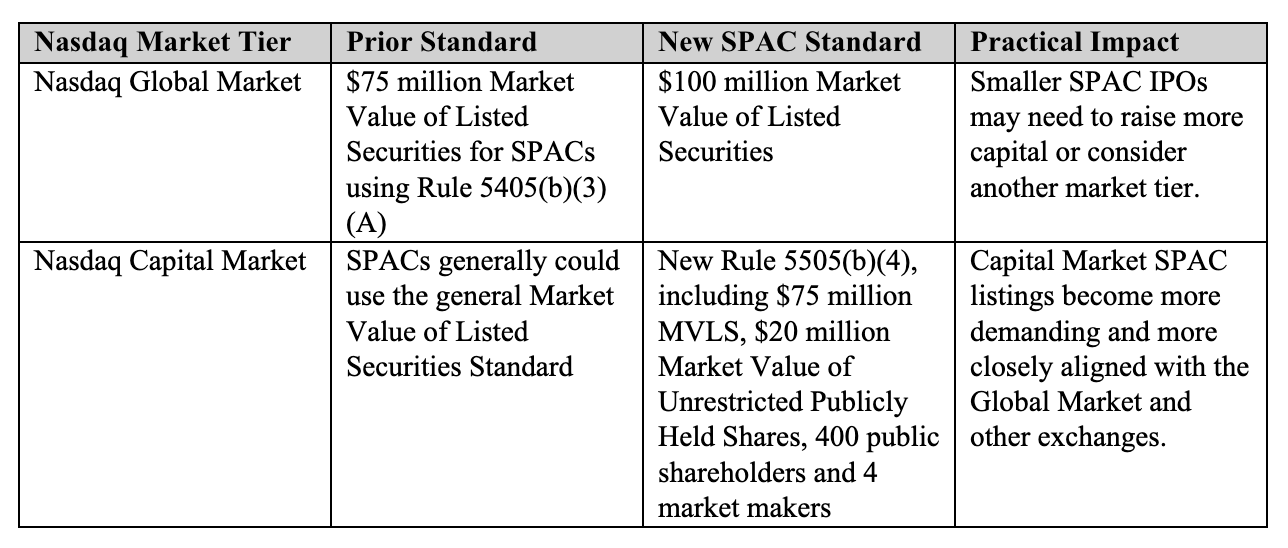

Nasdaq Global Market: $100 Million Market Value Requirement for SPACs

For SPACs seeking to list on the Nasdaq Global Market under the Market Value Standard, Nasdaq increased the minimum Market Value of Listed Securities from $75 million to $100 million. The 400-public-shareholder requirement remains unchanged. This is a narrow amendment, but it can be significant for sponsors designing a smaller SPAC IPO or trying to maintain flexibility in offering size.

Market Value of Listed Securities is especially important in the SPAC context because the company generally has no operating business at the time of its IPO. The value test is therefore closely tied to the size of the SPAC IPO and, in some structures, any listed-class securities purchased by the sponsor, underwriter or other investors in a concurrent private placement. A sponsor that previously could structure a Nasdaq Global Market SPAC around the $75 million threshold must now model compliance at the higher $100 million level.

For larger sponsors, the change may not alter transaction planning dramatically because many recent SPAC IPOs have been at or above $100 million. However, for smaller sponsors, specialized acquisition teams or sector-focused SPACs seeking a lower-cost entry point, the amendment reduces flexibility. It also reinforces the importance of planning Nasdaq eligibility before filing the IPO registration statement and before finalizing underwriting economics, warrant coverage and sponsor promote terms.

Nasdaq Capital Market: A New SPAC-Specific Listing Standard

The Nasdaq Capital Market amendments are likely to have a greater day-to-day impact. Historically, many SPACs viewed the Capital Market as a practical listing venue because it offered lower thresholds than the Nasdaq Global Market. Nasdaq’s new Rule 5505(b)(4) changes that approach by creating a SPAC-specific listing standard for Acquisition Companies and preventing SPACs from qualifying under the general Market Value of Listed Securities Standard in Rule 5505(b)(2).

Under the new Capital Market standard, a SPAC must have a Market Value of Listed Securities of at least $75 million. It also must have a Market Value of Unrestricted Publicly Held Shares of at least $20 million. For a SPAC listing in connection with an IPO, the rule text states that this unrestricted public float requirement must be satisfied from the offering proceeds. The SPAC also must have at least four registered and active market makers, rather than three, and at least 400 public shareholders, rather than the 300 round lot holder requirement that continues to apply to many non-SPAC companies.

These requirements matter because a SPAC may be able to satisfy a dollar-value test but still fail a distribution or liquidity test. Sponsors and underwriters should therefore coordinate investor outreach, syndicate structure, market-maker participation and closing mechanics early in the IPO process. SecuritiesLawyer101’s discussion of the NASDAQ listing process and documentation provides additional context for issuers preparing for a national exchange listing.

Why Nasdaq Tightened SPAC Listing Rules

Nasdaq’s stated rationale focuses on investor protection, liquidity and the distinctive risks associated with blank check companies. A SPAC does not have an operating business when it lists. Public investors are placing capital in a vehicle that is expected to identify, negotiate and complete a future business combination. That differs from a traditional operating company IPO, where investors can evaluate historical revenue, operations, assets, liabilities and management performance.

The rule change also reflects post-2020 SPAC market developments. After the SPAC boom of 2020 and 2021, market conditions changed, redemptions increased in many de-SPAC transactions, and regulators focused more heavily on conflicts of interest, projections, dilution and disclosure quality. The SEC’s final rules on Special Purpose Acquisition Companies, Shell Companies, and Projections are part of that broader regulatory environment.

Nasdaq also pointed to SPAC accounting and balance-sheet presentation issues. Many SPAC IPOs include redeemable shares. Depending on the accounting treatment, redeemable equity may affect a SPAC’s ability to satisfy stockholders’ equity-based listing standards. Nasdaq’s solution was not to eliminate SPAC listings but to impose standards that are tailored to Acquisition Companies and designed to support adequate scale and liquidity at the time of listing.

Key Takeaways for SPAC Sponsors and Underwriters

Model Nasdaq compliance before filing. Sponsors should test offering size, public float, public shareholder count and market-maker requirements before filing a registration statement or launching the IPO roadshow.

Do not rely on historical Capital Market thresholds. The new Rule 5505(b)(4) creates a dedicated SPAC pathway and removes the general market-value pathway for Acquisition Companies.

Plan distribution mechanics early. The increase to 400 public shareholders on the Capital Market may require more deliberate investor outreach, especially for smaller offerings.

Coordinate with market makers. A Capital Market SPAC now needs at least four registered and active market makers. This requirement should not be left until the end of the listing process.

Assess disclosure and post-IPO readiness. SPAC sponsors should evaluate Nasdaq compliance alongside SEC disclosure obligations, conflicts disclosure and public-company reporting systems. SecuritiesLawyer101’s article on preparing for SEC disclosure requirements may be useful for planning.

Implications for Target Companies in De-SPAC Transactions

Private companies considering a business combination with a Nasdaq-listed SPAC should not view the revised IPO listing standards in isolation. A larger SPAC may provide a broader trust account at the IPO stage, but the economics of a de-SPAC transaction depend on redemptions, sponsor promote, warrants, PIPE financing, transaction expenses and post-closing capital structure. A SPAC that meets Nasdaq’s enhanced IPO standards may still face significant challenges when completing a business combination and satisfying initial listing requirements for the combined company.

Target companies should also evaluate whether the SPAC has a credible plan for continued compliance, investor relations, financial reporting, internal controls and governance after the transaction. The combined company will need to operate as a public company immediately after closing. SEC filings for the SPAC and the combined company can be reviewed through SEC EDGAR, and target companies should use those filings to evaluate the SPAC’s disclosure history, capitalization and shareholder base.

The revised Nasdaq standards may also affect negotiation leverage. If smaller SPACs find it harder to list, target companies may see fewer lower-capitalization SPAC alternatives. On the other hand, the remaining Nasdaq-listed SPACs may be larger and better distributed. The best result will depend on the specific sponsor, investor base, financing plan and target company profile.

FAQ: Nasdaq SPAC Listing Rules

What is SR-NASDAQ-2026-033?

SR-NASDAQ-2026-033 is Nasdaq’s rule filing with the SEC to modify certain initial listing requirements for Acquisition Companies, commonly known as SPACs. The SEC published notice of filing and immediate effectiveness in Release No. 34-105291.

When do the new Nasdaq SPAC listing standards become operative?

The rule change became effective upon filing on April 15, 2026, and is scheduled to become operative 30 days after filing, on May 15, 2026, unless suspended by the SEC within the applicable review period.

How do the Nasdaq SPAC rules affect the Nasdaq Global Market?

For SPACs listing on the Nasdaq Global Market under the Market Value Standard, the minimum Market Value of Listed Securities increases from $75 million to $100 million. The 400-public-shareholder requirement remains unchanged.

How do the Nasdaq SPAC rules affect the Nasdaq Capital Market?

For SPACs listing on the Nasdaq Capital Market, new Rule 5505(b)(4) requires at least $75 million in Market Value of Listed Securities, at least $20 million in Market Value of Unrestricted Publicly Held Shares, at least 400 public shareholders and at least four registered and active market makers.

Do the new rules eliminate SPAC IPOs on Nasdaq?

No. The rules do not eliminate SPAC IPOs. They raise the entry threshold and make it more difficult for smaller or thinly distributed SPACs to list on Nasdaq without sufficient scale, public ownership and market-maker support.

Conclusion

Nasdaq’s enhanced SPAC IPO listing standards represent a meaningful tightening of exchange eligibility for Acquisition Companies. The most visible changes are the new $100 million Market Value of Listed Securities threshold for SPACs listing on the Nasdaq Global Market and the new SPAC-specific Capital Market standard requiring $75 million in Market Value of Listed Securities, $20 million in unrestricted publicly held shares, 400 public shareholders and four market makers.

For SPAC sponsors and underwriters, the message is straightforward: listing eligibility must be built into the transaction model from the beginning. For target companies, Nasdaq compliance should be reviewed as part of broader de-SPAC due diligence. For investors, the rule change reflects a continuing regulatory shift toward larger, more liquid and more broadly held SPACs. For more information about exchange listings, SEC reporting and going public transactions, visit SecuritiesLawyer101.com.