A Practical Guide for Issuers, Boards, Counsel, Transfer Agents and Practitioners Under Amended Nasdaq Rule 5250(e)(7)

Current through June 18, 2026.

Nasdaq-listed companies that plan to use a reverse stock split to regain or maintain compliance with Nasdaq minimum bid price requirements must now build a longer and more disciplined timeline. Nasdaq Listing Rule 5250(e)(7) and IM-5250-3 require a complete Company Event Notification Form by 12:00 p.m. Eastern Time at least ten calendar days before the proposed market effective date of the reverse stock split. The Company Event Notification Form must be complete when submitted, including the definitive split ratio, board and stockholder approval dates, the new post-split CUSIP, evidence that the new CUSIP has been made DTC eligible, and a draft of the public disclosure required by Nasdaq Rule 5250(b)(4).

The change matters because the CUSIP and DTC eligibility process can be the longest lead-time item in the transaction. Broadridge states in its corporate actions guidebook that a new CUSIP may take two business days to issue and that DTC may take approximately ten business days to make the new CUSIP DTC eligible. Nasdaq requires evidence of DTC eligibility with the Company Event Notification Form, so issuers cannot treat Nasdaq notice as a placeholder filing. The form must be complete at the time of submission.

Reverse split planning also requires attention to proxy and information statement timing. Broadridge’s current registered issuer guidebook states that beneficial shareholder records are returned from banks and brokers three business days after the record date, that materials should be received at least five business days before the preferred mailing date, and that mail method can affect delivery timing. VStock Transfer describes transfer-agent support for proxy mailings, broker search services, NOBO list or DTC Security Position List assistance, voting reports and mailing affidavits. These mailing and intermediary mechanics can affect when stockholder approval can be obtained and, for written-consent transactions, when the Rule 14C waiting period can begin.

The key practical point is simple: a Nasdaq reverse stock split should be planned backward from the proposed market effective date, and then adjusted for stockholder approval, proxy or information-statement mailing, Broadridge processing, VStock or other transfer-agent requirements, CUSIP issuance, DTC eligibility, Nasdaq notice, public disclosure, state filing, transfer-agent instructions and post-effective share reporting.

Quick Takeaways for Issuers and Practitioners

- The Nasdaq reverse split notice deadline is now 12:00 p.m. ET at least ten calendar days before the proposed market effective date, not five business days.

- The Nasdaq Company Event Notification Form must be complete and must include the new CUSIP, DTC eligibility evidence, approval dates, the reverse split ratio and draft public disclosure.

- Nasdaq Rule 5250(b)(4) separately requires public disclosure by 12:00 p.m. ET at least two business days before the proposed market effective date, with required MarketWatch notice before release.

- Nasdaq will not process a reverse split unless the Rule 5250(e)(7) and Rule 5250(b)(4) requirements are timely satisfied, and Nasdaq can halt trading if a company effects a reverse split without meeting them.

- Nasdaq Capital Market companies must check the post-split number of publicly held shares. A reverse split that fixes the bid price but causes the company to fall below the 500,000 publicly held shares continued listing threshold may not solve the Nasdaq compliance problem.

- A company with a prior reverse split may lose access to a Nasdaq compliance period if it later falls below the minimum bid price again within one year or if it has a cumulative reverse split ratio of 250-to-1 or more over two years.

- Proxy and information-statement timing can be as important as Nasdaq timing. Rule 14C requires the information statement to be sent or given at least 20 calendar days before the earliest date the corporate action may be taken.

- Issuers should prepare a reverse split calendar before scheduling the stockholder meeting or written-consent mailing, not after approval has already been obtained.

Why Reverse Stock Splits Matter for Nasdaq Companies

Nasdaq-listed companies often consider a reverse stock split when their common stock trades near or below the $1.00 minimum bid price required by Nasdaq continued listing standards. A reverse stock split combines a number of outstanding shares into a smaller number of shares. For example, in a one-for-ten reverse split, each ten pre-split shares become one post-split share. If market capitalization were unchanged, the post-split trading price would be expected to increase by the split multiple. In practice, however, post-split trading prices depend on market reaction, trading volume, liquidity, float, short interest, company fundamentals and investor perception.

A reverse split does not create value by itself. It changes the capital structure and may increase the nominal per-share price. That can be critical for a company seeking to regain compliance with the Nasdaq minimum bid price requirement, preserve an exchange listing, satisfy broker-dealer processing requirements, maintain institutional eligibility or avoid the reputational and liquidity consequences of delisting.

The process is not merely a corporate law filing. It is a coordinated securities, exchange, transfer agent, DTC, CUSIP, proxy, disclosure and market operations project. The amended Nasdaq rules make that coordination more important because the company must complete key preparatory steps before Nasdaq will accept the required reverse split notice.

Nasdaq Minimum Bid Price Rules and the Deficiency Timeline

Under Nasdaq Rule 5810(c)(3)(A), a minimum bid price deficiency exists if a company fails to meet the applicable minimum bid price requirement for 30 consecutive business days. After Nasdaq issues the deficiency notice, the company generally has 180 calendar days to regain compliance. A company typically regains compliance by maintaining a closing bid price of at least $1.00 for a minimum of ten consecutive business days during the compliance period, unless Nasdaq staff exercises discretion to require a longer period.

A Nasdaq Capital Market company may be eligible for an additional 180-calendar-day compliance period if it satisfies the conditions in Nasdaq Rule 5810(c)(3)(A)(ii). Among other things, on the 180th day of the first compliance period, it must meet the applicable market value of publicly held shares requirement and all other applicable initial listing standards for the Nasdaq Capital Market, other than the bid price requirement, and it must notify Nasdaq of its intent to cure the deficiency.

The deficiency notice also triggers disclosure obligations. Under Nasdaq Rule 5810(b), a company that receives a deficiency notification, Staff Delisting Determination or Public Reprimand Letter must publicly disclose the notice and the Nasdaq rule or rules on which it is based. The announcement generally must be made promptly and no later than four business days after receipt of the notice. The company should coordinate this disclosure with any Form 8-K obligation and with Nasdaq MarketWatch notice requirements.

New Nasdaq Limits on Using Reverse Splits to Cure Bid Price Deficiencies

The 2025 rule changes are broader than the new Company Event Notification Form deadline. Hogan Lovells has emphasized that the SEC-approved Nasdaq and NYSE revisions affect the compliance strategy of companies seeking to use reverse stock splits to regain or maintain compliance with the $1.00 minimum bid price requirements. For Nasdaq issuers, the rule changes address compliance periods, appeals and repeated reverse splits.

First, Nasdaq Rule 5810(c)(3)(A)(iii) provides that if a company security has a closing bid price of $0.10 or less for ten consecutive business days, Nasdaq will issue a Staff Delisting Determination and the company will be ineligible for the otherwise available compliance period.

Second, Nasdaq Rule 5810(c)(3)(A)(iv) provides that if a company fails to meet the minimum bid price requirement and has effected a reverse stock split over the prior one-year period, or has effected one or more reverse stock splits over the prior two-year period with a cumulative ratio of 250-to-1 or more, the company is not eligible for a bid-price compliance period and Nasdaq will issue a Staff Delisting Determination.

Third, a reverse split that creates another numeric listing deficiency may not cure the bid-price problem. Nasdaq Rule 5810(c)(3)(A) provides that a company will not be considered to have regained compliance with the bid-price requirement if the corporate action used to regain compliance causes the security to fall below the numeric threshold for another listing requirement. In that event, the company remains non-compliant until the other deficiency is cured and, after that, the company again meets the bid-price standard for the required trading period.

Nasdaq Capital Market Hook: The 500,000 Publicly Held Shares Issue

The Nasdaq Capital Market issue deserves special attention. Nasdaq Rule 5550(a) requires a Capital Market company to maintain, among other things, a minimum bid price of at least $1.00 per share, at least 300 public holders, at least 500,000 publicly held shares and a market value of publicly held shares of at least $1 million. A reverse split reduces the number of outstanding shares and can reduce the number of publicly held shares. A ratio that appears sufficient to increase the bid price may create a separate continued listing deficiency if it reduces publicly held shares below the applicable threshold.

For that reason, a Nasdaq Capital Market issuer should not select the split ratio by looking only at the pre-split trading price. The board, counsel and transfer agent should model the post-split public float, publicly held shares, registered holder count, public holder count, market value of publicly held shares, warrant and convertible security adjustments and shares reserved under equity plans. The ratio should create a meaningful bid-price cushion without jeopardizing another Nasdaq continued listing requirement.

Board Considerations Before Approving a Reverse Stock Split

The board should begin evaluating reverse split alternatives well before the end of the Nasdaq compliance period. A reverse stock split decision involves legal approvals, Nasdaq compliance, market strategy, capital structure, investor communications and operational mechanics. The board should create a written record of the factors considered and should work with counsel to ensure that the approvals cover all necessary actions.

- Nasdaq compliance deadline. Identify the exact end of the current compliance period, whether an additional compliance period is available and whether a hearing or appeal process is relevant.

- Reverse split history. Review all reverse splits over the prior one-year and two-year periods and calculate the cumulative ratio for Nasdaq Rule 5810(c)(3)(A)(iv).

- Ratio analysis. Model several ratios and assess the expected post-split bid price, float, liquidity, market value of publicly held shares, public holders and publicly held shares.

- Capital Market thresholds. For Nasdaq Capital Market issuers, confirm that the post-split share count will not fall below the 500,000 publicly held shares continued listing requirement or any other applicable threshold.

- Timing and disclosure. Consider whether the company can complete proxy or information-statement timing, DTC eligibility and Nasdaq notice before the desired effective date.

- Investor relations. Prepare messaging that explains the purpose of the reverse split without implying that Nasdaq compliance, price stability or increased market value is guaranteed.

- Derivative securities and contracts. Review warrants, preferred stock, convertible notes, equity awards, equity plans, financing documents, registration rights agreements, credit agreements and stockholder agreements for adjustment, consent or notice requirements.

- Fractional shares. Decide whether fractional shares will be rounded up, paid in cash or otherwise treated under the governing documents and applicable law.

- Authorized shares. Determine whether the reverse split will leave authorized shares unchanged, thereby increasing the number of authorized but unissued shares available for future issuance, and disclose that effect if material.

Stockholder Approval, Proxy Statements and Information Statements

Many public company reverse splits require stockholder approval under state law, the issuer certificate of incorporation or bylaws, or the structure of the proposed amendment. Companies incorporated in Delaware should analyze the current Delaware General Corporation Law, the specific charter provisions applicable to the company and whether a lower approval threshold is available for the reverse split amendment. The availability of any streamlined approval standard should not be assumed without reviewing the company charter and applicable law.

A company seeking stockholder approval will typically ask stockholders to approve either a specific split ratio or a ratio range, such as one-for-five to one-for-one hundred, with the board authorized to select the final ratio and abandon or delay the reverse split if circumstances change. A ratio range can be useful because the board may need to respond to market prices closer to implementation. The proxy statement should describe the factors the board may consider in selecting the final ratio.

Proxy disclosure should address the reasons for the reverse split, Nasdaq compliance, effects on outstanding shares, effects on authorized shares, effects on stockholders, fractional share treatment, risks, possible impact on liquidity, treatment of equity awards and derivative securities, and the fact that the reverse split may not result in a sustained increase in the trading price. The disclosure should avoid promising that the reverse split will cure Nasdaq compliance or improve the company market value.

If the company uses written consent and a Schedule 14C information statement, the Rule 14C timing rule must be built into the reverse split calendar. Rule 14c-2 provides that the information statement must be sent or given at least 20 calendar days before the meeting date or, in the case of corporate action by written authorization or consent, at least 20 calendar days before the earliest date on which the corporate action may be taken. This means that a company using written consent cannot simply move from stockholder consent to effectiveness. The mailing date and the 20-calendar-day waiting period must be integrated with the Nasdaq T-10 calendar-day notice deadline, DTC eligibility, state filing and market effective date.

In the ordinary issuer-controlled written-consent context, Rule 14c-2 should be treated as a gating item. The SEC added C&DI 182.01 on January 23, 2026 for a narrow dissident-consent situation where written consents are solicited without the registrant’s knowledge. In that limited circumstance, the staff states that Rule 14c-2 does not invalidate the corporate action merely because the 20-calendar-day period could not be satisfied, and state law or the registrant’s governing documents determine effectiveness. That interpretation should not be treated as a general shortcut for issuer-planned reverse splits.

Broker Search, Broadridge Mailing and Beneficial-Owner Processing

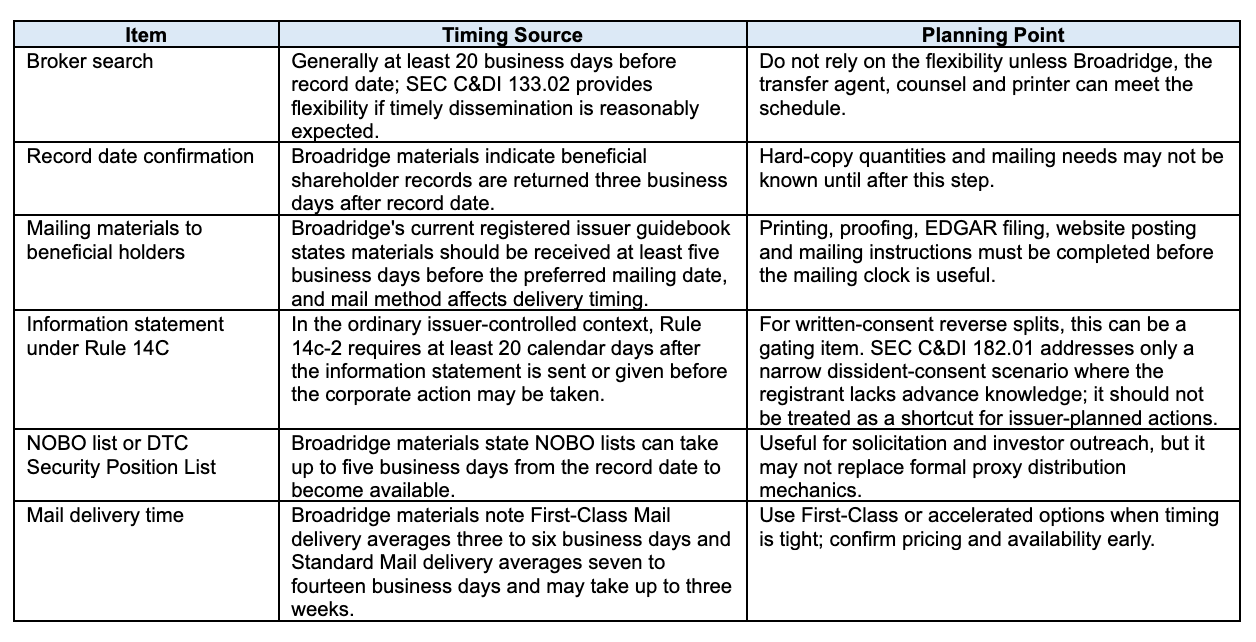

Proxy distribution can create a separate timing track. Broadridge materials explain that beneficial shareholder records are returned from banks and brokers three business days after the record date. Broadridge also states that hard-copy proxy materials are mailed within five business days after receipt of materials and instructions, and that accelerated mailing may be available for an additional fee. Broadridge materials further note that domestic USPS First-Class Mail delivery averages three to six business days after the mailing vendor receives the material, while USPS Standard Mail delivery averages seven to fourteen business days and may take up to three weeks.

The SEC staff updated its proxy rules interpretations in January 2026. SEC C&DI 133.02 states that Rule 14a-13(a)(3) generally requires broker search at least 20 business days before the record date, but the staff will not object if a registrant conducts broker search less than 20 business days before the record date when the registrant reasonably believes the proxy materials will be timely disseminated to beneficial owners and otherwise complies with Rule 14a-13. The same position applies to similar information-statement broker searches under Rule 14c-7(a)(3). This interpretation provides flexibility, but it should not be treated as permission to ignore practical mailing and intermediary delays.

NOBO lists and DTC Security Position Lists should also be requested early if needed for vote solicitation, investor communications or holder analysis. Broadridge materials state that a NOBO list can take up to five business days from the record date to become available online. VStock describes assistance with ordering NOBO lists or DTC Security Position Lists, as well as broker search services, proxy mailing coordination, certified registered shareholder lists and notarized mailing affidavits. These transfer-agent and intermediary steps can affect the date on which materials are actually mailed and, for Schedule 14C transactions, the date on which the 20-calendar-day waiting period begins.

CUSIP, DTC Eligibility and the Transfer Agent Role

A reverse stock split generally requires a new CUSIP number for the post-split common stock. Obtaining the CUSIP number and making the new CUSIP DTC eligible are not the same thing. Nasdaq requires evidence that the new CUSIP has been made eligible at DTC as part of the Company Event Notification Form. The company therefore needs both the new CUSIP and DTC eligibility evidence before the Nasdaq T-10 calendar-day submission deadline.

Broadridge corporate action materials state that the issuer should acquire a new CUSIP as early as possible, that the CUSIP Bureau may take two business days to issue the new CUSIP, and that DTC may take approximately ten business days to make the new CUSIP DTC eligible. Broadridge also states that the new CUSIP must be DTC eligible before the effective date. Those operational lead times are important because Nasdaq will not process the reverse split unless the required Nasdaq notice and public disclosure steps are timely satisfied.

Broadridge’s 15-day corporate action timeline should be treated as an operational planning benchmark, not as the controlling Nasdaq notice rule. For Nasdaq-listed issuers, the binding reverse split notification deadline is Nasdaq Rule 5250(e)(7): a complete Company Event Notification Form by 12:00 p.m. ET at least ten calendar days before the proposed market effective date.

VStock explains that DTC eligibility allows securities to be deposited, cleared, settled and transferred electronically through The Depository Trust Company and integrated into the national clearing and settlement system. VStock also describes DTC eligibility as essential for listings on Nasdaq, NYSE and NYSE American, as well as for public offerings, secondary market trading and electronic brokerage deposits. Transfer agents that participate in DTC systems, including DWAC/FAST and DRS, are central to making the post-split security operational for electronic clearing and settlement.

The most important sequencing issue is that DTC eligibility may not be granted until after stockholder approval has been obtained when stockholder approval is required. As a result, the company should prepare all transfer-agent materials, CUSIP applications, board approvals, draft charter amendment, proxy or information-statement disclosure, Nasdaq forms and public announcement drafts in advance so that the DTC eligibility process can move immediately after approval.

Amended Nasdaq Rule 5250(e)(7): Company Event Notification Form

The central Nasdaq timing rule is Rule 5250(e)(7). For a reverse stock split, the company must file a complete Company Event Notification Form by 12:00 p.m. ET ten calendar days before the proposed market effective date. Nasdaq states that the submission must include all information required by the form and a draft of the public disclosure required by Rule 5250(b)(4). Nasdaq will not process the reverse split unless these requirements and the public disclosure requirements are timely satisfied. If the company takes legal action to effect a reverse stock split despite failing to satisfy the requirements, or provides incomplete or inaccurate public disclosure about timing or ratio, Nasdaq can halt trading.

The Nasdaq Company Event Notification Form preview identifies the information Nasdaq expects for a reverse split submission, including the new CUSIP, board approval date, stockholder approval date if applicable, DTC eligibility date, current and post-split share information, par value information, insider holdings, publicly held shares, transfer agent contact information, legal filing timing, expected market effective date, definitive split ratio and draft public disclosure. The company should treat the form as a completion checklist, not as a notice that can be supplemented later.

Nasdaq Issuer Alert 2025-1 confirms the operative change from the prior five-business-day reverse split notice standard to the ten-calendar-day notice standard. The alert also confirms that the two-business-day public disclosure requirement remains unchanged and that the notification rules apply across the Nasdaq Global Select Market, Nasdaq Global Market and Nasdaq Capital Market tiers.

Public Disclosure Under Nasdaq Rule 5250(b)(4)

The Nasdaq T-10 Company Event Notification Form requirement does not replace the separate public disclosure requirement. Nasdaq Rule 5250(b)(4) requires the company to publicly disclose the reverse stock split by 12:00 p.m. ET at least two business days before the proposed market effective date. Before releasing the disclosure, the company must notify Nasdaq MarketWatch at least ten minutes before public announcement if the release is made between 7:00 a.m. and 8:00 p.m. ET. If the disclosure is released outside those hours, the company must notify MarketWatch before 6:50 a.m. ET.

The press release should be specific and consistent with the Nasdaq form, charter amendment, board resolutions, Form 8-K and transfer-agent instructions. It should include the reverse split ratio, legal effective time, expected market effective date, new CUSIP, treatment of fractional shares, effect on outstanding shares, exchange mechanics for registered holders, and the purpose of the reverse split. If the split is intended to help regain Nasdaq minimum bid price compliance, the disclosure should state that goal accurately and should avoid suggesting that compliance is guaranteed.

State Filing, Legal Effectiveness and Market Effectiveness

Most reverse stock splits are effected through a certificate of amendment or articles of amendment filed with the company state or jurisdiction of incorporation. The company should coordinate the filing time with Nasdaq, the transfer agent and DTC. A common structure is for the amendment to become legally effective after market close on the business day before the proposed Nasdaq market effective date, with the common stock beginning to trade on a split-adjusted basis at the open of trading on the next business day.

Practitioners should distinguish between legal effectiveness and market effectiveness. The legal effective time is when the amendment becomes effective under corporate law. The market effective date is the first trading day on which Nasdaq reflects the reverse split in the trading market. Nasdaq Rule 5250(e)(7) measures the ten-calendar-day notice deadline by the proposed market effective date.

Nasdaq’s Company Event Notification Form materials also note the market operations mechanics. Under Nasdaq Rules 4120(a)(14) and 4753(b), Nasdaq generally halts trading at approximately 7:50 p.m. ET on the day immediately before the market effective date of a reverse stock split and generally reopens the security for trading at approximately 9:00 a.m. ET on the market effective date, subject to Nasdaq processing.

Fractional Shares and Exchange Mechanics

Reverse splits often create fractional shares. The board should approve the treatment of fractional shares and counsel should confirm that the approach is permitted under applicable state law and the company governing documents. Common approaches include rounding fractional shares up to the next whole share, paying cash in lieu of fractional shares, or aggregating fractional shares and distributing proceeds. The selected approach must be disclosed in the proxy statement or information statement, press release and Form 8-K, and must be operationally supported by the transfer agent.

Broadridge corporate action materials state that, after the event date, Broadridge generally mails letters of transmittal and cover letters within four days to holders of certificates or mixed certificate/book-entry positions and automatically exchanges book-entry shares, including DTC positions, within four days after the event. If cash in lieu is payable, the company and transfer agent should confirm funding needs before effectiveness.

Equity Awards, Warrants, Convertible Securities and Other Instruments

A reverse split requires review of the company entire capital structure. Equity plan reserves, stock options, restricted stock units, performance awards, warrants, pre-funded warrants, convertible notes, preferred stock and other securities may require proportionate adjustment. Most instruments adjust both the number of shares issuable and the exercise or conversion price. Some instruments contain special rounding provisions, beneficial ownership blockers, exchange caps, anti-dilution provisions or notice requirements.

Counsel should prepare a security-by-security adjustment schedule before effectiveness. The company should confirm whether notices must be delivered before or after effectiveness, whether board or committee approvals are required, whether any third-party consents are needed and whether the transfer agent or warrant agent must receive special instructions. If the company has outstanding warrants or convertible securities with unusual anti-dilution provisions, the reverse split should not be treated as a purely mechanical adjustment.

Form 8-K, SEC Filings and Offering Documents

A company that receives a Nasdaq deficiency notice should evaluate Form 8-K disclosure obligations, including Item 3.01. A company that files a charter amendment to effect a reverse stock split should evaluate Form 8-K disclosure under Item 5.03 and, where applicable, Item 3.03 or other items depending on the facts. Companies often file the reverse split press release as an exhibit and describe the ratio, effective time, market effective date, new CUSIP and fractional share treatment.

The company should also review pending registration statements, resale prospectuses, ATM programs, equity lines, shelf takedowns, Rule 424 prospectus supplements and investor presentations to determine whether share numbers, prices, conversion prices, exercise prices or risk factors need updating. Companies with prior reverse splits, volatile trading prices or a realistic risk of future bid-price non-compliance should update risk factors to reflect the current Nasdaq rules.

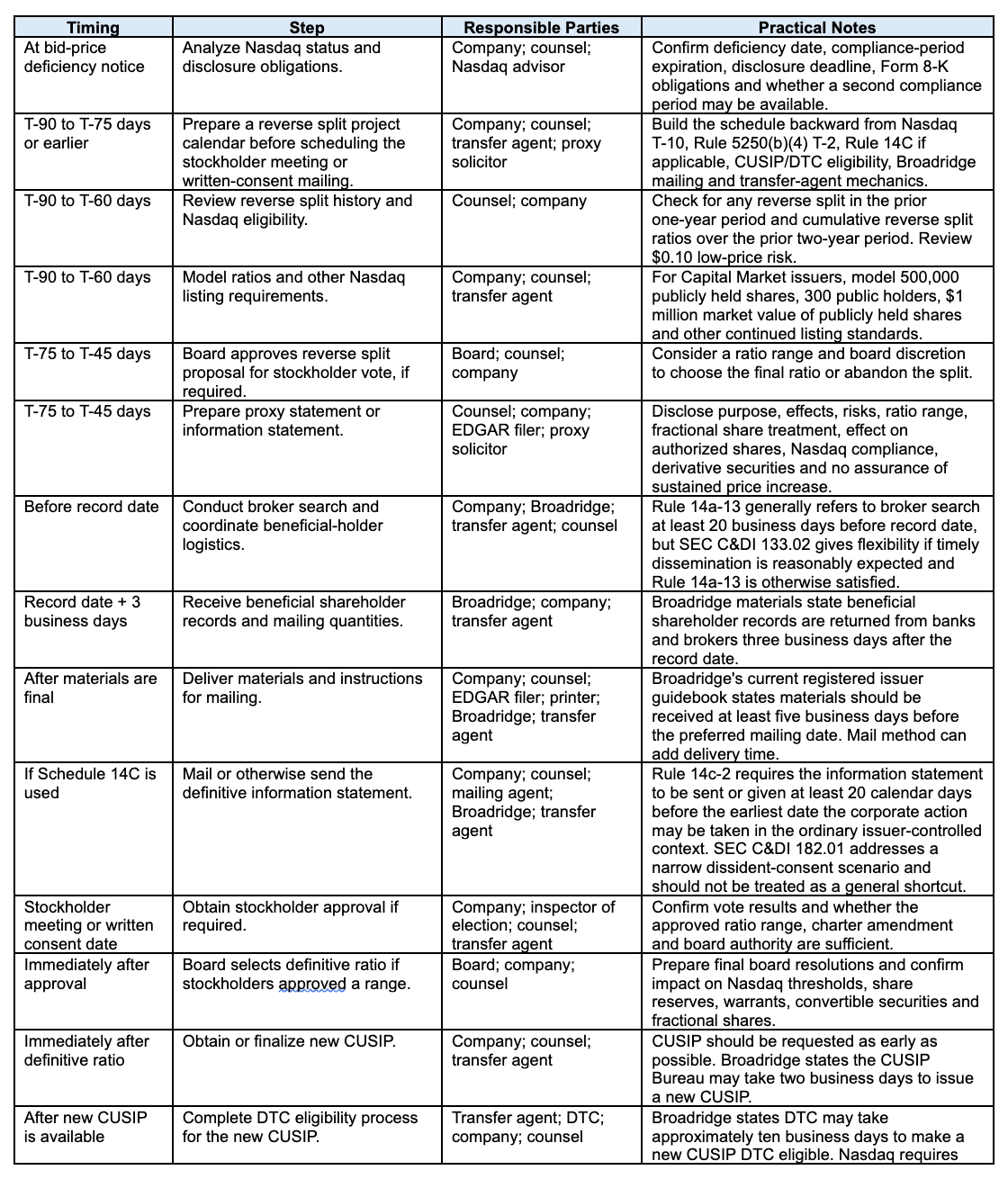

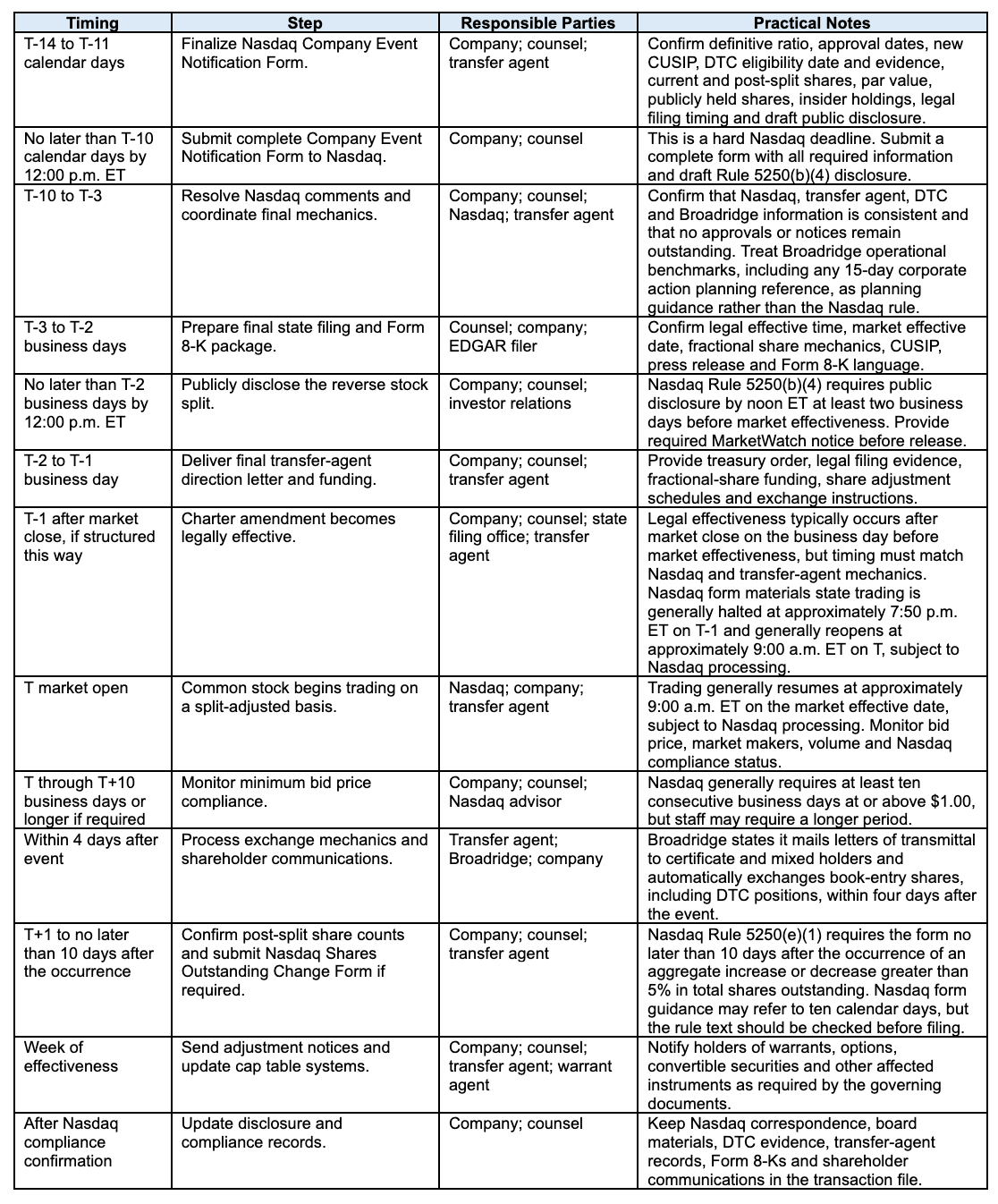

Detailed Nasdaq Reverse Stock Split Timeline

The following timeline assumes T equals the proposed Nasdaq market effective date, meaning the first trading day on which the common stock trades on a split-adjusted basis. The legal effective time is often after market close on T-1, but the structure should be confirmed with counsel, Nasdaq and the transfer agent. Because DTC eligibility and proxy distribution can drive timing, issuers should customize the calendar based on the stockholder approval path, transfer agent requirements, Broadridge processing and the Nasdaq compliance deadline.

Practical Proxy and Mailing Overlay

Common Mistakes That Delay Nasdaq Reverse Stock Splits

- Treating the Nasdaq T-10 deadline as a notice filing rather than a complete-form deadline.

- Obtaining the CUSIP but not DTC eligibility evidence before the Nasdaq filing deadline.

- Selecting a ratio that cures bid price but creates a new deficiency in publicly held shares, public holders or market value of publicly held shares.

- Failing to build Rule 14C mailing and 20-calendar-day waiting periods into the calendar.

- Waiting to involve the transfer agent, Broadridge, DTC or the financial printer until after stockholder approval.

- Using inconsistent dates or ratios in board resolutions, proxy materials, Nasdaq forms, press releases, Form 8-Ks and transfer-agent instructions.

- Ignoring warrant, convertible security, equity award or contractual notice requirements.

- Assuming Nasdaq will waive or expedite the reverse split processing deadline.

- Forgetting that Nasdaq may require more than ten consecutive business days above $1.00 if the margin of compliance or trading activity is weak.

- Announcing a market effective date before DTC eligibility and Nasdaq processing are realistically achievable.

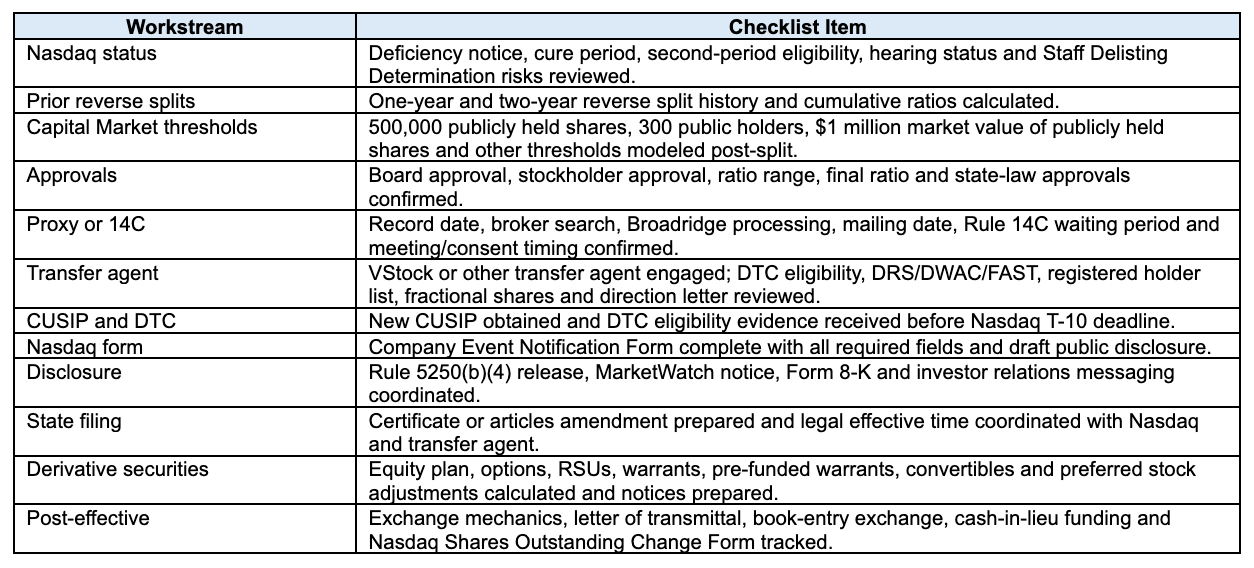

Practitioner Checklist

Planning Recommendations

A company should not set a proposed market effective date until it has a credible path to completing stockholder approval, CUSIP issuance, DTC eligibility and Nasdaq submission. The safest practice is to create two calendars: an approval calendar and an implementation calendar. The approval calendar covers board approval, proxy or information statement preparation, broker search, Broadridge mailing, VStock or other transfer-agent support, meeting or written consent and Rule 14C waiting periods. The implementation calendar covers the final ratio, new CUSIP, DTC eligibility, Nasdaq Company Event Notification Form, public disclosure, state filing, transfer-agent instructions, market effectiveness and post-effective reporting.

Counsel should circulate the timeline to the company, transfer agent, Nasdaq advisor, Broadridge or other intermediary, EDGAR filer, financial printer, investor relations team and proxy solicitor. Each party should confirm its own lead times in writing. When a company is close to the end of a Nasdaq cure period, assumptions about mailing, DTC eligibility or Nasdaq processing can become the difference between timely compliance and a delisting determination.

The reverse split calendar should include contingency time. DTC eligibility may take longer than expected, broker search and beneficial-holder records may delay mailing quantities, stockholder approval may require adjournment, and Nasdaq may require clarification or correction before processing. A reverse split is often viewed as an emergency step, but the amended Nasdaq rules reward companies that start early and penalize those that wait until the final week.

Conclusion

Reverse stock splits remain an important tool for Nasdaq-listed companies seeking to regain compliance with the minimum bid price requirement. Under the amended Nasdaq rules, however, the process must begin earlier and must be managed more carefully. The company must have a complete Nasdaq submission by noon ET at least ten calendar days before the proposed market effective date, and that submission must include DTC eligibility evidence for the new CUSIP. Public disclosure must be made by noon ET at least two business days before the market effective date, with Nasdaq MarketWatch notice before release.

For issuers and practitioners, the practical lesson is to plan backward from the market effective date and forward from the stockholder approval process. A reliable reverse split timeline must include Nasdaq compliance rules, Rule 14C or proxy mailing requirements, Broadridge and beneficial-owner processing, VStock or other transfer-agent mechanics, CUSIP and DTC eligibility, state filing, public disclosure, Nasdaq halt and reopen mechanics, derivative security adjustments and post-effective Nasdaq reporting.

This article is for general informational purposes only and does not constitute legal advice. Companies should consult securities counsel, their transfer agent, Nasdaq representatives and other advisors before implementing a reverse stock split or making related public disclosures.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com