Why Nasdaq compliance matters

A Nasdaq listing can be a major milestone for a public company. It can increase market visibility, broaden potential institutional interest, improve trading liquidity, and make a company easier for analysts, investment banks, market makers, and investors to follow. For many smaller public companies, the Nasdaq Capital Market is the practical entry point because it is designed for companies that are not yet large enough for the Nasdaq Global Market or Nasdaq Global Select Market but can meet meaningful financial, liquidity, and corporate governance standards.

Nasdaq compliance should not be treated as a final step that begins after a financing is complete. It is a transaction workstream that should begin early. The company’s capitalization table, transfer agent records, public float, shareholder base, SEC reporting history, board composition, committee charters, code of conduct, press releases, website, investor presentation, and public filings may all become part of the review. A company that waits until the listing application is ready to discover weaknesses in these areas can lose valuable time.

Nasdaq’s three market tiers

Nasdaq maintains three principal listing tiers: the Nasdaq Global Select Market, the Nasdaq Global Market, and the Nasdaq Capital Market. The Global Select Market has the highest initial listing standards. The Global Market is generally used by companies with stronger financial and liquidity profiles than Capital Market issuers. The Nasdaq Capital Market is often the most relevant tier for small-cap issuers and many companies seeking to uplist from the OTC market.

Each tier has separate quantitative requirements, but the tiers share many qualitative and governance expectations. A company that meets a numerical standard is not automatically entitled to list. Nasdaq retains discretion to deny a listing if it believes the listing would be inconsistent with the protection of investors or the public interest.

Nasdaq review is both quantitative and qualitative

A listing application is not just a numbers exercise. Nasdaq reviews whether the issuer satisfies one of the applicable listing standards, but it also evaluates the integrity of the issuer’s public record and corporate governance. Nasdaq may review SEC filings, financial statements, auditor reports, state corporate records, charter documents, transfer agent information, litigation disclosures, regulatory history, related-party transactions, public statements, press releases, website content, financing history, convertible securities, and the backgrounds of officers, directors, promoters, control persons, and significant shareholders.

For that reason, a company preparing for Nasdaq should conduct a pre-filing readiness review. The goal is to identify issues before Nasdaq staff raises them. Common issues include going concern language, inconsistent share counts, unresolved transfer agent questions, incomplete committee independence analysis, outstanding regulatory correspondence, recent private placements, unregistered resales, related-party debt, and corporate actions that were not clearly documented.

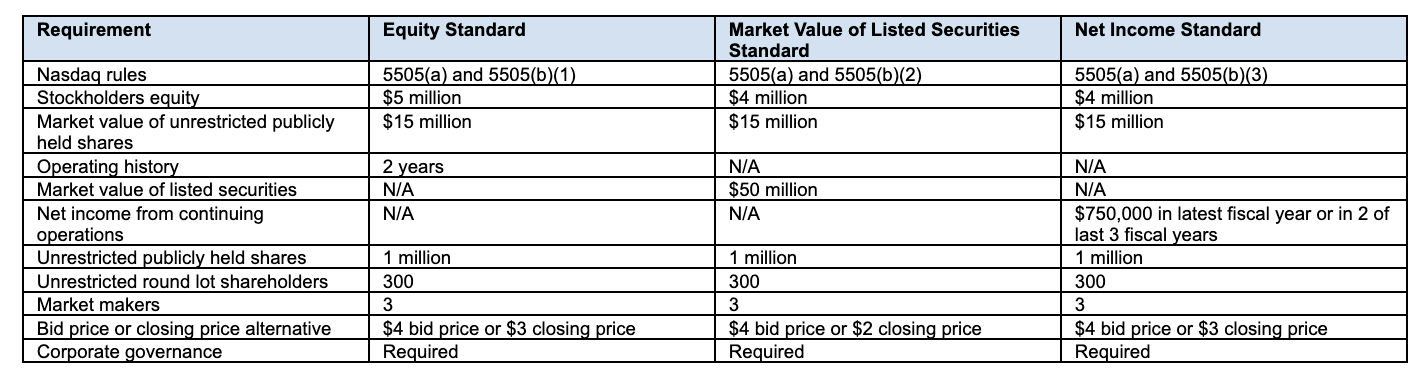

Nasdaq Capital Market initial listing standards

A company seeking to list common equity on the Nasdaq Capital Market generally must satisfy all applicable criteria under at least one of three financial standards: the Equity Standard, the Market Value of Listed Securities Standard, or the Net Income Standard. The following table summarizes the core Capital Market financial and liquidity thresholds reflected in Nasdaq’s 2026 initial listing guide.

A currently traded company that seeks to qualify solely under the Market Value of Listed Securities Standard must also satisfy the market value and bid price requirements for a specified trading period before applying. Nasdaq also has additional requirements for companies that were trading over the counter before applying, including average daily volume requirements, unless the company is completing a qualifying firm commitment underwritten offering. Issuers using an offering to satisfy the market value of publicly held shares test should coordinate the offering mechanics carefully because Nasdaq may require that the requirement be satisfied through the offering proceeds.

Direct listings and valuation-supported listings

Some companies seek a Nasdaq listing without a traditional firm commitment underwritten public offering. Direct listings can be available, but they involve separate valuation and pricing requirements. Nasdaq’s direct listing framework requires an independent third-party valuation or other compelling evidence of value, depending on the standard relied upon. The direct listing standards also generally impose higher market value, publicly held share value, and bid price thresholds than traditional listing routes.

Direct listings require careful sequencing. A company must analyze whether it can demonstrate an adequate market for its securities, satisfy public float and shareholder requirements, and provide the valuation support Nasdaq expects. A direct listing may reduce underwriting involvement, but it does not reduce the importance of securities counsel, transfer agent coordination, investor relations planning, and reliable market data.

Corporate governance requirements

Nasdaq-listed companies must maintain corporate governance practices that support independent oversight, transparent decision-making, and shareholder protection. These standards apply across Nasdaq’s market tiers and include requirements for annual and interim reports, a majority independent board, an independent audit committee, an independent compensation committee, independent director oversight of nominations, a code of conduct, annual shareholder meetings, proxy solicitation, quorum requirements, conflict of interest review, shareholder approval for specified transactions, and voting rights protections.

A Nasdaq listing plan should include a governance checklist long before filing. The company should confirm the independence of each director, verify that audit committee members meet Rule 10A-3 and Nasdaq requirements, adopt or update committee charters, document executive sessions of independent directors, review related-party transaction policies, and confirm that shareholder approval requirements are understood before any financing or acquisition is signed.

For smaller reporting companies and foreign private issuers, certain accommodations or home-country practice exceptions may be available, but exemptions should be documented rather than assumed. Nasdaq’s corporate governance certification process requires the issuer to identify applicable exemptions and certify compliance with the governing rules.

Preparing the Nasdaq application

Nasdaq’s listing application is submitted electronically through the Nasdaq Listing Center. The application package typically includes the listing application, listing agreement, corporate governance certification, logo submission, applicable fees, and supporting documents. Depending on the transaction, the issuer may also need market maker letters, shareholder lists, transfer agent confirmations, regulatory correspondence, legal documentation, and offering-related materials.

The company should expect Nasdaq to assign an analyst after the application is submitted. The review process often includes comments and follow-up questions. A well-prepared application can reduce avoidable delays because the staff can focus on substantive eligibility issues rather than missing signatures, inconsistent share numbers, or incomplete documentation.

Symbol reservation and CUSIP coordination

A trading symbol is more than a branding decision. Nasdaq symbols generally contain one to five characters and are coordinated through market symbol reservation systems designed to avoid conflicts and operational confusion. A company should submit symbol choices in order of preference and should not assume that its first choice will be available. Nasdaq retains authority over symbol assignment.

Symbol planning should be coordinated with CUSIP matters, state corporate filings, transfer agent records, and any related name change, merger, or reverse split. Inconsistent names, dates, ratios, or share amounts can create processing issues for Nasdaq, DTC, market makers, brokers, and data vendors.

Nasdaq listing fees

Nasdaq charges initial entry fees and annual fees. For the Nasdaq Capital Market, entry fees are based on the aggregate number of shares outstanding at the time of initial listing, subject to fee schedules and a non-refundable application fee component. Nasdaq’s 2026 guide reflects Capital Market initial entry fees of $50,000 for up to 15 million shares and $75,000 for more than 15 million shares, with $5,000 of that amount treated as the non-refundable application fee. Special purpose acquisition companies and other issuers may be subject to separate fee schedules.

Fees should be budgeted as part of the transaction. A company should also budget legal fees, auditor costs, transfer agent costs, exchange advisory costs, DTC or CUSIP expenses, investor relations costs, and board or committee compensation.

Benefits of uplisting from the OTC market

A Nasdaq listing can help a company move beyond many of the limitations that affect OTC securities. Exchange-listed securities may have greater visibility, more reliable market data, broader broker-dealer participation, more potential research coverage, and better access to institutional investors. An exchange listing can also help reduce the stigma associated with penny stocks because securities listed on a national securities exchange are generally excluded from penny stock treatment if the exchange maintains the required listing standards.

That benefit should not be overstated. Nasdaq listing does not eliminate securities law compliance, resale restrictions, anti-fraud obligations, corporate governance duties, disclosure controls, internal control issues, or financing diligence. It does, however, create a more regulated market structure and may make the company’s securities more accessible to investors and market participants.

Penny stock considerations

The penny stock rules restrict broker-dealer activity in low-priced, non-exchange-listed securities. These rules can require account approvals, written customer agreements, risk disclosures, quotation disclosures, compensation disclosures, and ongoing account statements. The practical effect is that many brokers are reluctant to recommend or facilitate transactions in penny stocks.

For OTC issuers, this can limit liquidity, investor access, and market support. For a company planning a public financing, acquisition strategy, or investor relations campaign, a Nasdaq listing may be part of a broader plan to improve trading conditions. Still, a reverse split or price increase alone is not enough. Nasdaq will review the issuer’s full eligibility, public record, shareholder base, governance, and market quality.

Practical Nasdaq readiness checklist

Before filing, a company should confirm that it can meet the applicable Nasdaq Capital Market standard without relying on unsupported assumptions. Management should test the company’s public float, shareholder count, unrestricted share count, bid or closing price, market makers, stockholders’ equity, net income, market value, and operating history. The company should also confirm that any recent private placements or recapitalizations will not create listing, shareholder approval, or resale concerns.

The issuer should also complete a governance readiness review. This includes board independence, audit committee composition, compensation committee independence, nominating procedures, committee charters, code of conduct, annual meeting planning, proxy procedures, related-party transaction controls, and shareholder approval requirements. Public companies should also review disclosure controls, SEC reporting timeliness, auditor independence, internal controls, and consistency across public materials.

Conclusion

Nasdaq compliance requires strategy, documentation, timing, and discipline. The strongest applicants treat the listing process as a coordinated legal, accounting, market structure, corporate governance, and investor relations project. For small-cap issuers, the Nasdaq Capital Market can be a realistic path to a national exchange listing, but only when the company prepares early and resolves compliance issues before filing.

A securities lawyer can help evaluate Nasdaq eligibility, structure financing transactions around listing requirements, prepare the listing application, coordinate with auditors and transfer agents, and respond to Nasdaq comments. Companies considering a Nasdaq uplisting or initial listing should begin with a comprehensive readiness review.

FAQ

How long does the Nasdaq listing process take?

Nasdaq’s initial listing guide states that the listing process generally takes four to six weeks, but timing can vary depending on the quality of the application, the complexity of the issuer’s history, comments from Nasdaq staff, financing timing, and whether the company must resolve governance, shareholder, or market structure issues.

Is the Nasdaq Capital Market only for small companies?

No. It is often used by smaller public companies because its initial listing standards are less demanding than the Global Market and Global Select Market standards, but every applicant must satisfy Nasdaq’s applicable financial, liquidity, and governance rules.

Can Nasdaq reject an application even if the company meets the numbers?

Yes. Nasdaq has discretion to deny listing when it believes approval would be inconsistent with investor protection or the public interest. Regulatory history, incomplete records, disclosure issues, shareholder concerns, and market integrity concerns can matter.

This securities law blog post is provided as a general informational service. If you have any questions about this article or need assistance with Nasdaq listing requirements, Nasdaq uplistings, public offerings, reverse split planning, corporate governance compliance, and securities law disclosure, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com