The deadline depends on the action

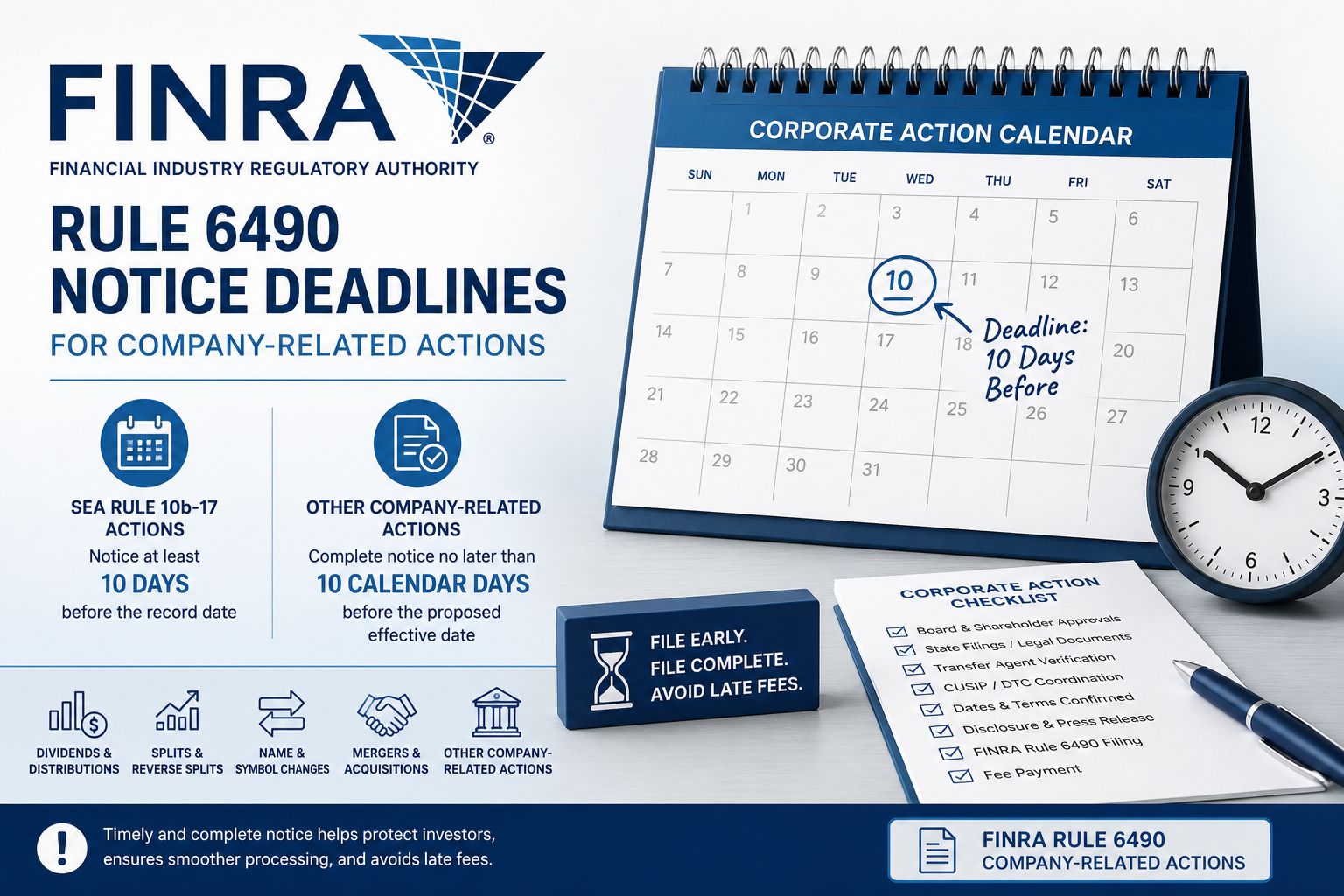

FINRA Rule 6490 separates actions into two broad categories. The first category is an SEA Rule 10b-17 Action, which generally includes dividends and other distributions, stock splits, reverse stock splits, and rights or subscription offerings. The second category is an Other Company-Related Action, which includes actions such as name changes, symbol changes, mergers, acquisitions, dissolutions, bankruptcy-related actions, and similar events that affect market information for OTC securities.

For an SEA Rule 10b-17 Action, the issuer must provide notice consistent with SEC Rule 10b-17. In general, notice must be provided at least 10 days before the record date. If the issuer misses the deadline, the submission may be treated as late and may trigger a higher FINRA fee.

For Other Company-Related Actions, Rule 6490 requires a complete request to be submitted in the manner and form required by FINRA no later than 10 calendar days before the proposed effective date. The word complete matters. A partial submission without key documents, transfer agent verification, payment support, or accurate dates can create processing problems.

Work backward from the market date

Companies should not wait until the last 10 days to begin the process. A company may need board approval, shareholder approval, state filings, CUSIP coordination, transfer agent review, DTC coordination, updated disclosures, draft press releases, and legal review before the FINRA submission is ready. If any document contains inconsistent dates, share amounts, names, ratios, or capitalization information, FINRA may ask questions or refuse to process the action.

For reverse splits and name changes, the timeline should account for new CUSIP requests, charter amendments, transfer agent confirmations, issuer disclosure updates, and trading symbol issues. For dividends and distributions, the issuer must coordinate record dates, payment dates, distribution mechanics, and disclosure language.

Late filings can become expensive

Rule 6490 imposes late fees for SEA Rule 10b-17 notifications. The fee increases as the corporate action date approaches. A timely notification costs far less than a late notification submitted shortly before, on, or after the corporate action date. Late notice can also create market confusion and may increase the risk that FINRA will delay processing.

A corporate action calendar should therefore be part of every OTC issuer’s compliance program. Management should identify proposed corporate actions early, circulate the timeline to counsel and the transfer agent, and confirm that the proposed dates comply with FINRA and SEC requirements before public announcements are made.

Practical filing tip

The best practice is to file early, complete, and consistently. FINRA should receive a package that tells one coherent story: the corporate authority exists, the dates are correct, the capitalization is accurate, the transfer agent can verify the facts, and the action can be processed without harming investors or market integrity.

Before setting a record date or effective date for a corporate action, an OTC issuer should consult securities counsel to calculate the Rule 6490 deadline and prepare a complete filing package.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com