A comprehensive guide to OTCQX International eligibility, quotation, Rule 15c2-11, Form 211 and ongoing compliance under the April 6, 2026 V11 rules

Current through OTCQX Rules for International Companies and OTCQX Rules for U.S. Companies, Version 11, effective April 6, 2026.

Executive Summary

OTCQX is the highest market tier operated by OTC Markets Group for over-the-counter securities. For a foreign issuer, OTCQX can provide a practical U.S. trading platform without the full cost, timing and corporate governance burden of a Nasdaq or New York Stock Exchange listing. It can also create a disciplined public-company framework that helps a foreign company build U.S. investor awareness, develop trading history, improve disclosure practices and prepare for a future national securities exchange listing.

The April 6, 2026 Version 11 OTCQX Rules materially changed the qualification analysis. The rules now require a $25 million global market capitalization for admission, a minimum $5 million market value of public float, 100 beneficial shareholders each owning at least 100 shares, and more detailed continued-qualification standards. They also add transition provisions for companies already on OTCQX as of April 6, 2026, and clarify the conditional qualification route for companies that do not yet meet the net tangible asset or revenue components of the penny-stock exemption tests but can satisfy a $5.00 bid price and demonstrate expected compliance in their next annual report.

For international companies, the 2026 rules should be read carefully. The international company rule set requires the issuer to be listed on a Qualified Foreign Exchange and current in its home-market reporting obligations, and to be exempt from SEC registration under Rule 12g3-2(b), otherwise exempt from SEC registration, or an SEC Reporting Company or Regulation A Reporting Company. SEC reporting can satisfy the reporting-status prong, but under the OTCQX International Rules it is not a substitute for the separate Qualified Foreign Exchange listing requirement. A foreign-incorporated company that is not listed on a Qualified Foreign Exchange must analyze whether it is treated as a U.S. Company under the OTCQX U.S. Companies rules or whether another market tier is more appropriate.

This guide covers OTCQX admission, quotation and continued qualification for foreign issuers in 2026. It also includes U.S. comparative requirements because OTC Markets uses separate U.S. and International rulebooks, and because foreign companies sometimes fall between the two categories depending on where they are organized, where their securities trade, where their operations are managed and whether they have an SEC reporting obligation. The guide is written as a practical reference for issuers, boards, transfer agents, market makers and securities counsel.

Introduction: Why Foreign Issuers Use OTCQX

Small- and mid-cap companies seeking access to U.S. capital markets and improved liquidity for their capital stock should consider the benefits that OTC Markets can provide as an alternative to a primary national securities exchange. For many foreign issuers, OTCQX is not intended to replace a home-market listing. Rather, it supplements the home-market listing by creating a U.S. quotation and disclosure channel that U.S. investors, broker-dealers and information vendors can recognize and access.

Unlike Nasdaq and the New York Stock Exchange, OTCQX is not a registered stock exchange. It is a premium market operated by OTC Markets Group through a broker-dealer quotation and alternative trading system structure. Trading is conducted through a decentralized network of broker-dealers rather than a centralized exchange matching engine. This distinction matters because the process is built around quotation eligibility, market-maker participation, issuer disclosure and continuing OTC Markets standards rather than an exchange listing application alone.

OTCQX is attractive in the short term because it generally involves lower monetary and timing costs than a national exchange listing. It does not require the same level of exchange governance infrastructure, listing fees, underwriter involvement, or securities exchange review that usually accompanies a Nasdaq or NYSE listing. In the long term, OTCQX can serve as a springboard. A foreign issuer that builds a compliant OTCQX trading market may later use that trading history, shareholder base, disclosure record and U.S. investor familiarity as part of a strategy to uplist to Nasdaq, NYSE American or the NYSE.

OTCQX is not suitable for every company. It is designed for established, investor-focused companies that meet financial standards, are current in disclosure obligations, are not penny stocks for broker-dealer purposes, are not shell companies or blank-check companies other than qualifying SPACs and are not in bankruptcy. OTCQX is also not a shortcut around securities-law compliance. Foreign issuers must analyze Exchange Act status, Rule 12g3-2(b), home-market obligations, Securities Act resale issues, blue sky issues, transfer-agent readiness, market-maker interest and the practical requirements of Rule 15c2-11.

The April 2026 amendments make this threshold analysis more important. A company that might have qualified under the pre-2026 rules may not qualify under the new standards without additional planning. The most common problems are insufficient market capitalization, insufficient public float value, too few beneficial shareholders, stale financial statements, absence of a Qualified Foreign Exchange listing, inadequate English-language disclosure, and lack of market-maker support.

OTC Markets Tiers and the Role of OTCQX

OTC Markets Group organizes issuers into four principal market tiers: OTCQX Best Market, OTCQB Venture Market, OTCID Basic Market and Pink Limited Market. Each tier reflects a different level of disclosure, eligibility standards and market visibility. These designations are not the same as a national securities exchange listing, and they do not eliminate the need to analyze federal securities laws, state securities laws, FINRA rules, transfer-agent issues or broker-dealer quotation requirements.

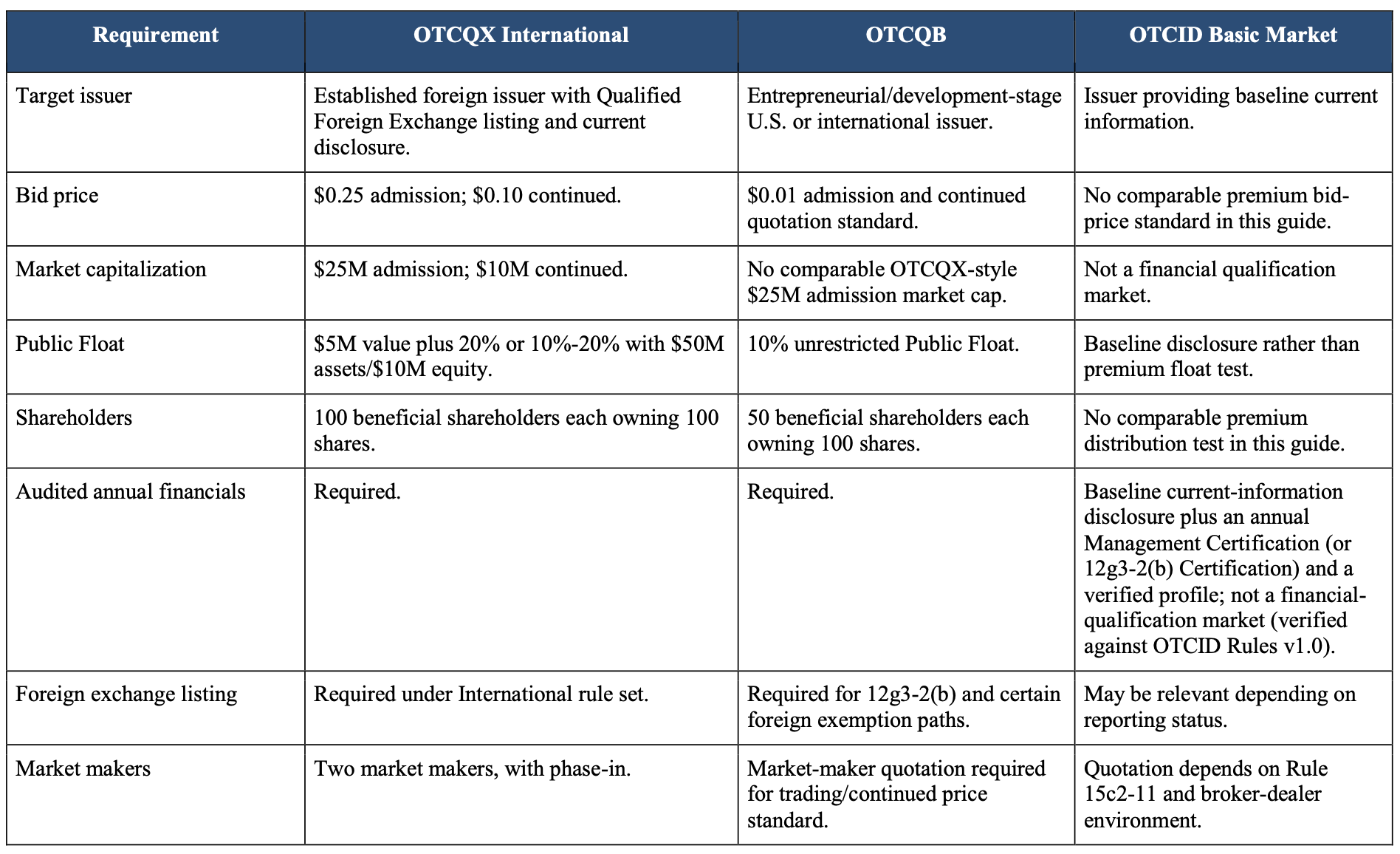

OTCQX Best Market is the highest OTC Markets tier. It is intended for established U.S. and international companies that satisfy financial standards, follow best-practice governance, demonstrate compliance with U.S. securities laws and remain current in their disclosure obligations. OTCQB Venture Market is designed for entrepreneurial and development-stage companies that meet a lower bid-price threshold and less demanding financial thresholds. OTCID Basic Market is a baseline disclosure market for companies that publish ongoing financial disclosure, provide a management certification and verify their company profile. Pink Limited Market reflects limited issuer-provided disclosure and generally offers less transparency.

A foreign issuer choosing between OTCQX, OTCQB and OTCID should begin with the strategic objective. If the company wants a premium U.S. market designation and has the market value, float, shareholder distribution, financial statements and home-market status to support it, OTCQX may be the right target. If the company is earlier stage or does not satisfy the higher market capitalization and float standards, OTCQB may be more realistic. If the company is only trying to maintain baseline disclosure and visibility, OTCID may be a transitional or minimum market solution.

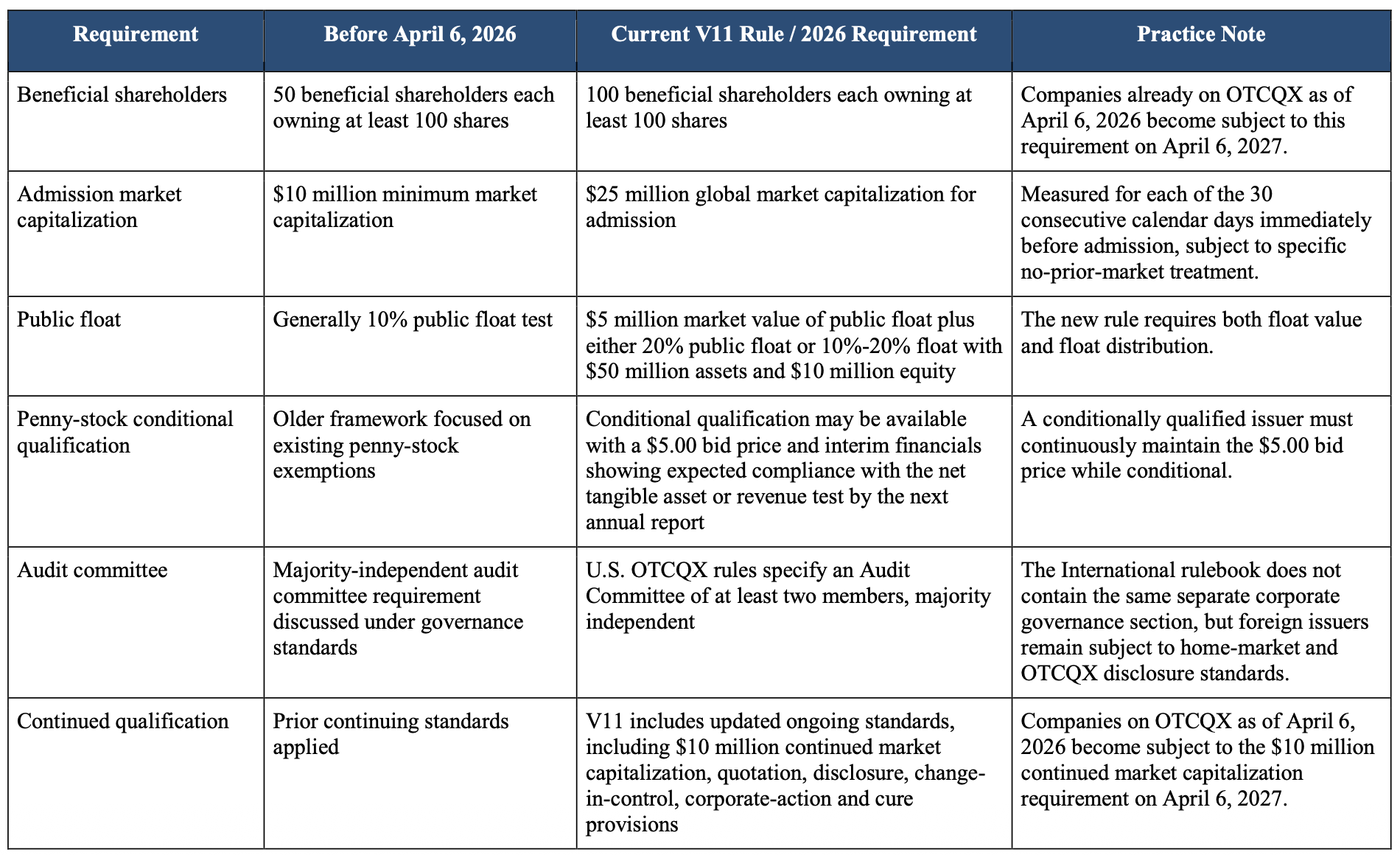

What Changed in the April 6, 2026 OTCQX Rules

The Version 11 OTCQX Rules, effective April 6, 2026, significantly changed the OTCQX analysis. The amendments were not merely administrative. They raised quantitative thresholds, added a market-value component to public float, increased the shareholder distribution requirement, clarified conditional qualification under the penny-stock exemption framework, and added new ongoing standards. As a result, a securities lawyer reviewing OTCQX eligibility in 2026 should not rely on older OTCQX guides that refer to the former 50-shareholder requirement, $10 million admission market capitalization, or prior public-float formulation.

The following chart summarizes the major changes that should be reflected in any current OTCQX eligibility memo or blog article. The chart is a simplified comparison; the detailed requirements appear in the sections that follow.

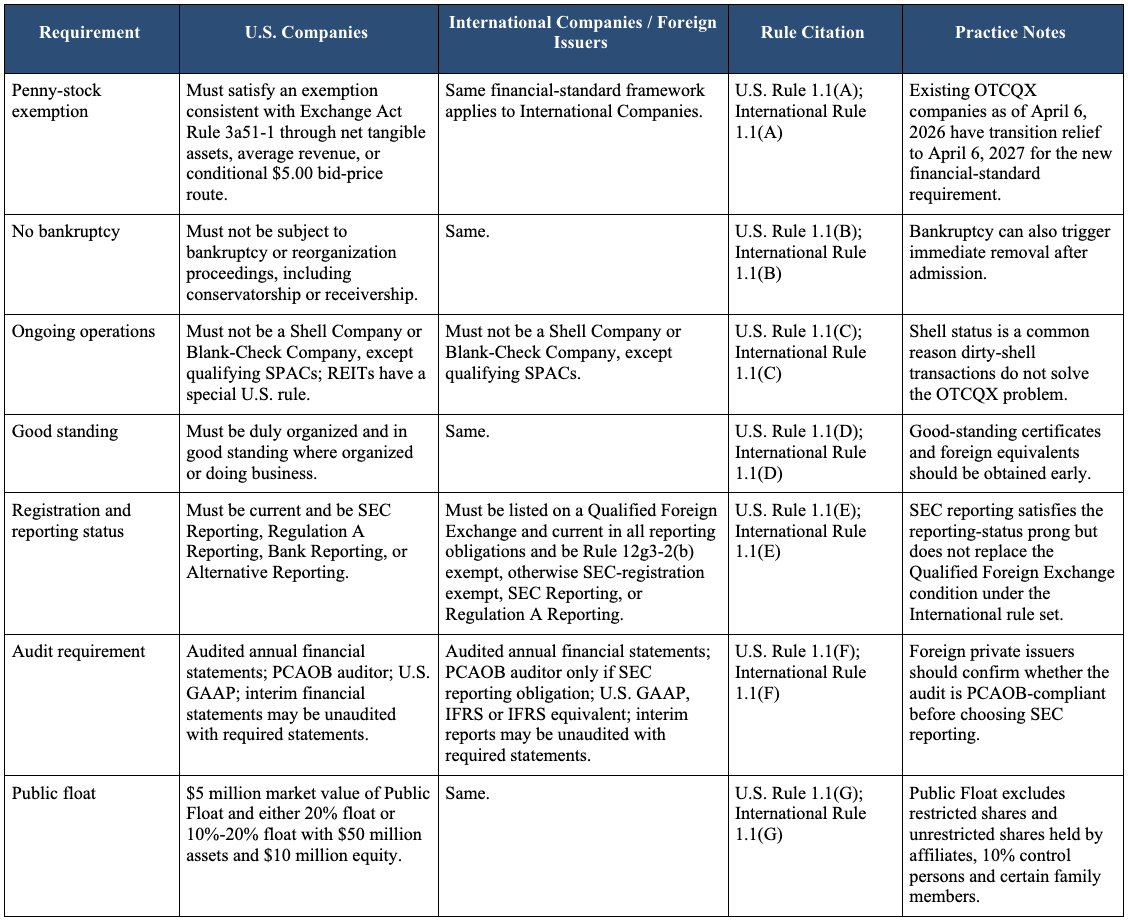

Complete OTCQX Eligibility Checklist

The starting point for any OTCQX analysis is a complete eligibility checklist. The checklist should not be limited to the headline thresholds. A company can satisfy the $25 million market capitalization requirement and still fail OTCQX because it is a shell, lacks a Qualified Foreign Exchange listing, has stale or noncompliant financial statements, does not have enough beneficial shareholders, lacks market-maker support, or cannot provide the required disclosure in English.

The chart below compares the U.S. and International rule sets because many foreign issuers must consider both. A company incorporated outside the United States may still be treated as a U.S. Company under the OTCQX U.S. rules if it is not listed on a non-U.S. exchange and has sufficient U.S. nexus, including trading volume, U.S. holders, U.S. officers or directors, U.S. assets and U.S. administration. Conversely, a company applying under the International rules should be prepared to demonstrate that it is listed on a Qualified Foreign Exchange and current in the reporting obligations of that exchange.

Chart Footnotes to the Master Eligibility Checklist

[1] Public Float means unrestricted shares outstanding after subtracting shares subject to resale or transfer restrictions and unrestricted shares held directly or indirectly by affiliates, officers, directors, 10% control persons and certain family members. A company with many shares outstanding can still fail the Public Float test if most unrestricted shares are held by control persons or insiders.

[2] Beneficial Shareholder means a person who directly or indirectly has or shares voting power or investment power over the security. The 2026 OTCQX requirement is not merely a record-holder test. Issuers should work with their transfer agent, brokers and counsel to determine beneficial ownership support.

[3] A Qualified Foreign Exchange is a non-U.S. exchange appearing on the OTC Markets Group List of Qualified Foreign Exchanges, as amended from time to time. Common Asian exchanges that have appeared on OTC Markets qualified exchange lists include HKEX, Tokyo Stock Exchange, Singapore Exchange, Korea Exchange, Taiwan Stock Exchange, Taipei Exchange, Bursa Malaysia, Stock Exchange of Thailand, Indonesia Stock Exchange, Philippine Stock Exchange, Shanghai Stock Exchange, Shenzhen Stock Exchange, Bombay Stock Exchange and National Stock Exchange of India. The list should be checked before filing because it can change.

[4] Conditional qualification is not a general waiver. Under the V11 rules, it is tied to the $5.00 minimum bid price and interim financial reports demonstrating that the company is expected to meet the net tangible asset or average revenue standards as of its next annual report.

[5] PCAOB audit requirements differ between U.S. and International issuers. International Companies are exempt from the PCAOB requirement unless they have an SEC reporting obligation. Regulation A Reporting Companies receive an initial eligibility exception only; subsequent annual audits must use a PCAOB-registered auditor.

[6] The OTCQX International Rules do not contain a separate OTCQX International Premier tier in Version 11. References in older articles or legacy charts to OTCQX International Premier should be updated or removed.

[7] The market-maker phase-in allows one market maker at admission or within three business days after admission if the company applies with an Initial Review, but two market makers must publish proprietary priced quotes within 90 days of admission.

[8] Existing companies on OTCQX as of April 6, 2026 generally received transition relief to April 6, 2027 for the new financial-standard requirement, the 100-beneficial-shareholder requirement and the $10 million continued market capitalization requirement.

[9] Corporate action notices should be analyzed under Exchange Act Rule 10b-17, FINRA Rule 6490 and the applicable OTCQX continued qualification standards. Name changes, symbol changes, stock splits, reverse splits, dividends, mergers, acquisitions and changes in the nature of securities can involve timing, fee and processing issues.

Penny Stock Exemption and Conditional Qualification

The penny-stock exemption is one of the most important OTCQX requirements and one of the most frequently misunderstood. OTCQX is designed to exclude penny stocks, shell companies and companies in bankruptcy. For broker-dealer purposes, the analysis begins with Exchange Act Rule 3a51-1, which defines penny stock and identifies exclusions. OTC Markets incorporates the concept by requiring an OTCQX applicant to meet one of the specified exemptions consistent with that rule.

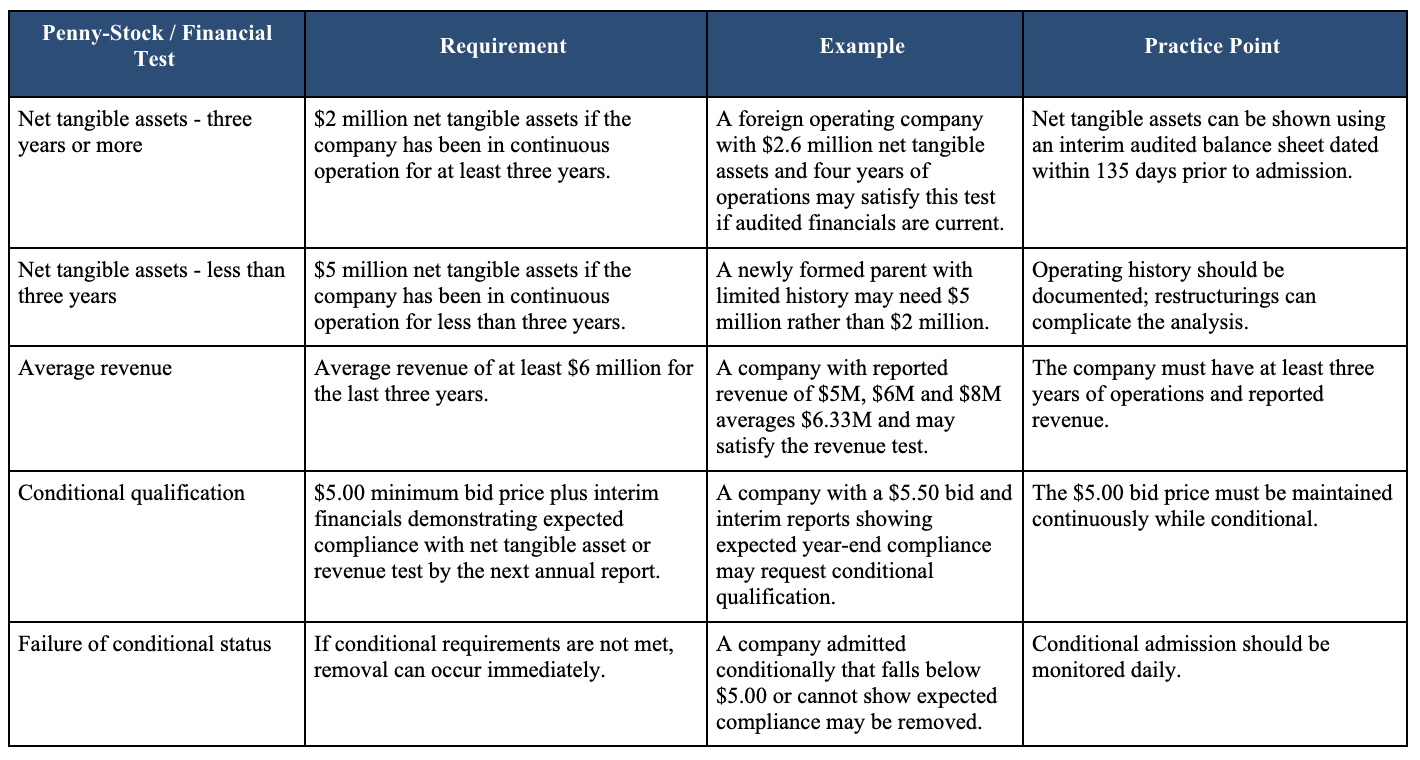

Under the 2026 OTCQX framework, the principal financial tests are net tangible assets and average revenue. A company may qualify if, based on audited financial reports dated within 15 months of admission, it reports net tangible assets of at least $2 million if it has been in continuous operation for at least three years, or at least $5 million if it has been in continuous operation for less than three years. Alternatively, it may qualify by reporting average revenue of at least $6 million for the last three years. For the revenue test, the company must have at least three years of operations and reported revenue.

The V11 rules also recognize a conditional path. A company that does not currently satisfy the net tangible asset or revenue tests may qualify conditionally until publication of its next annual report if each class of securities to be traded on OTCQX has a minimum bid price of $5.00 and the company provides interim unaudited financial reports demonstrating to OTC Markets Group’s satisfaction that it will satisfy the applicable net tangible asset or revenue test as of the next annual report. A company admitted conditionally must continuously maintain the $5.00 minimum bid price for each class of securities qualified for OTCQX while it remains conditional.

The conditional path should not be viewed as a cure for weak fundamentals. It is better understood as a timing bridge for a company that is close to meeting the financial criteria and can document expected compliance. Counsel should not advise a company to pursue OTCQX on the assumption that OTC Markets will disregard the financial tests. OTC Markets retains discretion, and the company must requalify under the actual financial tests when the next annual report is published.

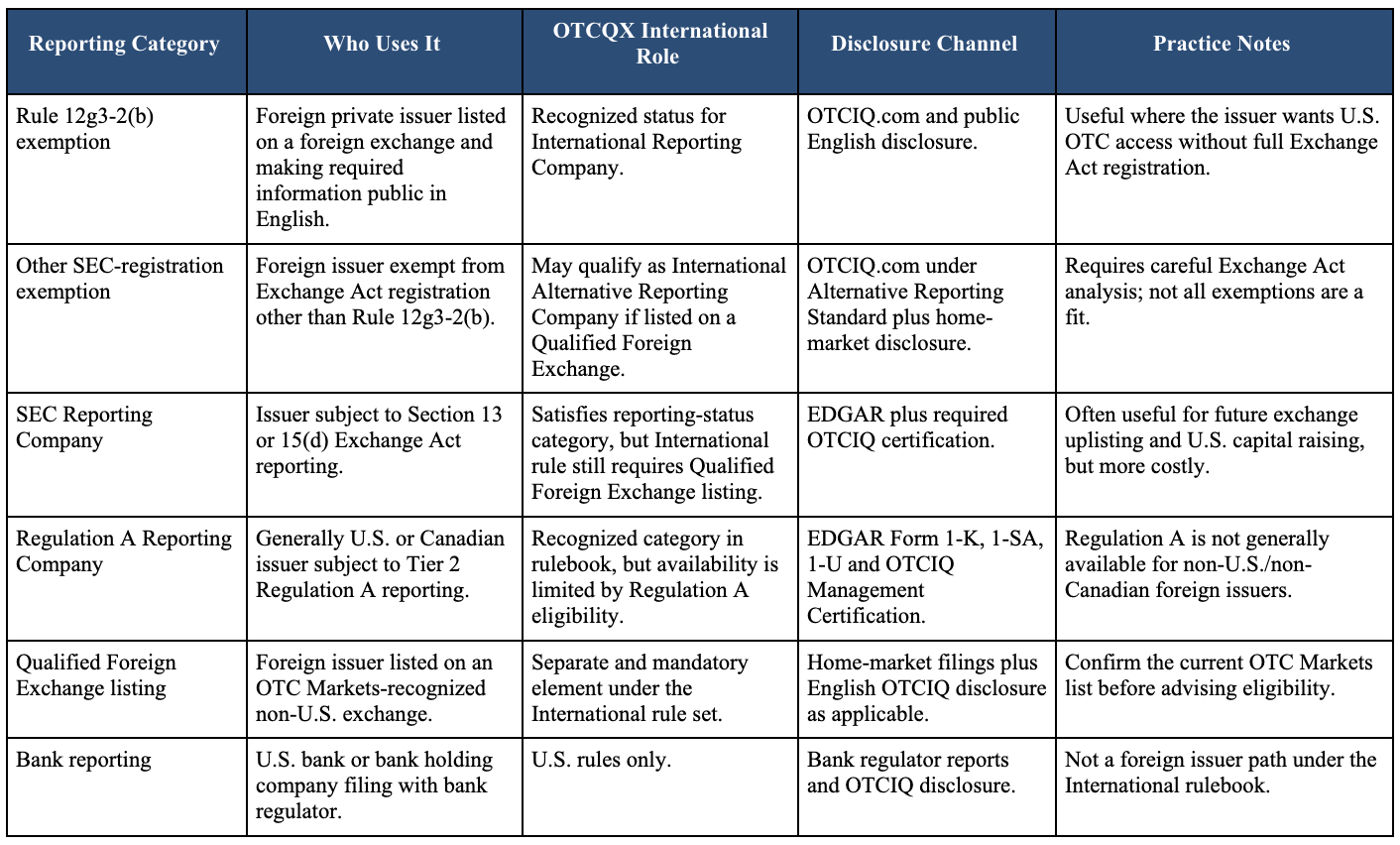

Registration and Reporting Status for Foreign Issuers

Foreign issuers frequently focus on financial thresholds but overlook registration and reporting requirements. Under the OTCQX International Rules, the company must be listed on a Qualified Foreign Exchange and current in all reporting obligations, and it must fall within one of the recognized reporting categories. The categories include Rule 12g3-2(b), another exemption from SEC registration, SEC reporting, or Regulation A reporting.

Rule 12g3-2(b) is important because it allows qualifying foreign private issuers to maintain a U.S. OTC trading market without registering a class of securities under Exchange Act Section 12(g), provided that the issuer makes specified English-language information publicly available. A foreign issuer that relies on Rule 12g3-2(b) should not treat the exemption as a passive status. The issuer must remain current with its home-market disclosure and ensure the required information is publicly available in English.

Some foreign issuers voluntarily become SEC Reporting Companies by registering a class of securities under the Exchange Act or filing reports under Section 15(d). SEC reporting can provide greater U.S. investor familiarity and may be useful for a later Nasdaq or NYSE American uplisting. It also brings significant cost, timing and liability considerations, including SEC periodic reporting, Form 20-F, Form 6-K and, depending on structure, Securities Act registration statement considerations.

Regulation A reporting is relevant only for a narrower subset of foreign-related issuers because Regulation A is generally available only to U.S. and Canadian issuers that meet the eligibility conditions. A non-Canadian foreign company should not assume Regulation A is available. When a foreign company is organized in Canada or uses a U.S. issuer structure, Regulation A may be part of the capital formation and OTC strategy, but the analysis should be performed before building the offering and trading plan.

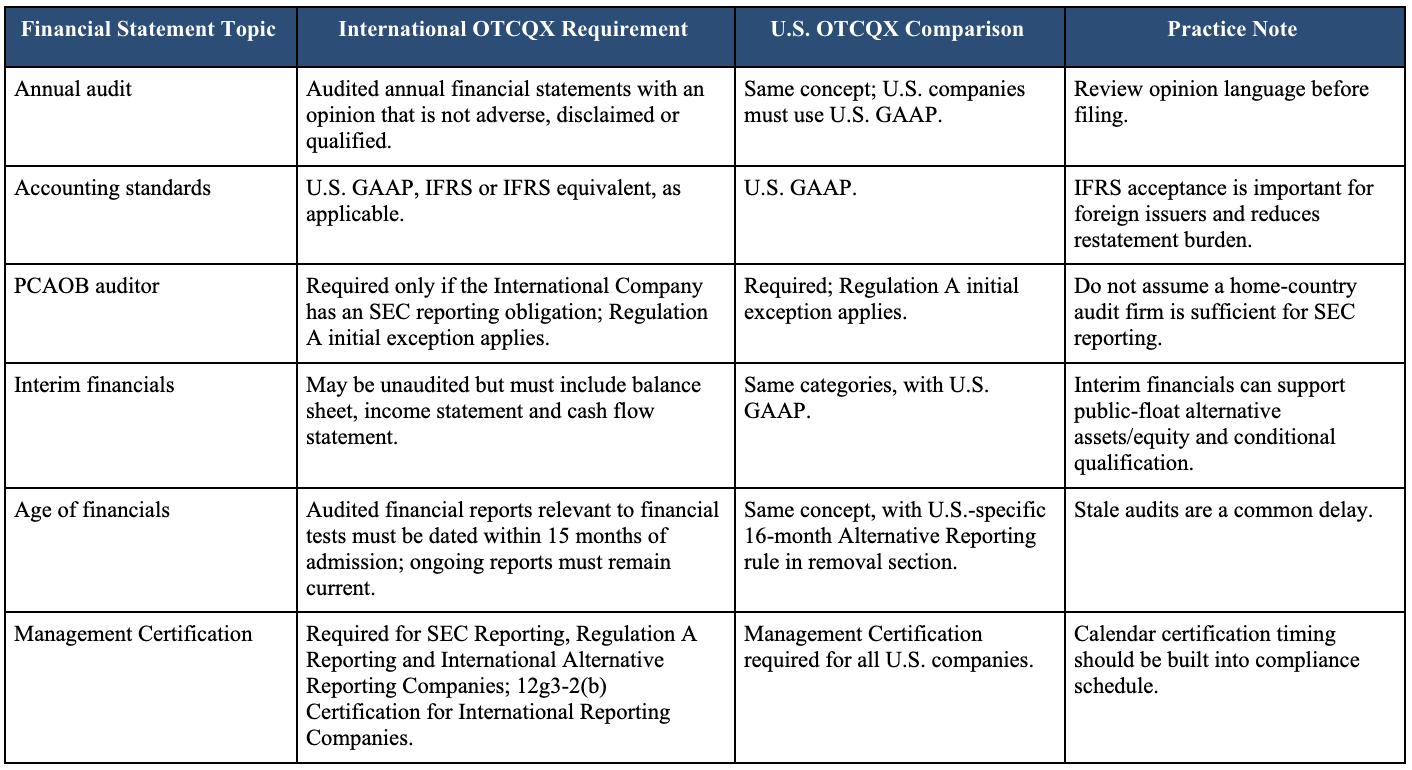

Financial Statements, PCAOB Audits and IFRS

Financial-statement readiness is often the longest lead-time item in an OTCQX project. For International Companies, annual financial statements must be audited and must include an audit opinion that is not adverse, disclaimed or qualified. Periodic financial statements may be prepared under U.S. GAAP, IFRS or IFRS equivalent, as applicable. Interim financial reports may be unaudited, but they must include a balance sheet for the most recent interim period, an income statement for the most recent interim period, and a statement of cash flows for the most recent interim period and the comparable period of the preceding 12 months.

The PCAOB requirement turns on the issuer’s status. International Companies are exempt from the PCAOB auditor requirement unless the company has an SEC reporting obligation. This distinction is critical. A foreign issuer that is not SEC reporting and relies on home-market disclosure may use a non-PCAOB auditor if the audit otherwise meets the rule. But if the issuer is an SEC Reporting Company, the auditor must be PCAOB-registered. Regulation A Reporting Companies receive an initial eligibility exemption only; subsequent annual audits must be PCAOB-compliant.

Counsel should review the audit opinion itself, not just confirm that audited financial statements exist. An adverse opinion, disclaimer or qualified opinion will not satisfy the OTCQX audit requirement. The age of the financial statements also matters. Under the penny-stock financial tests, audited financial reports must be dated within 15 months of admission, and ongoing audited reports must remain current under the continued qualification and removal rules.

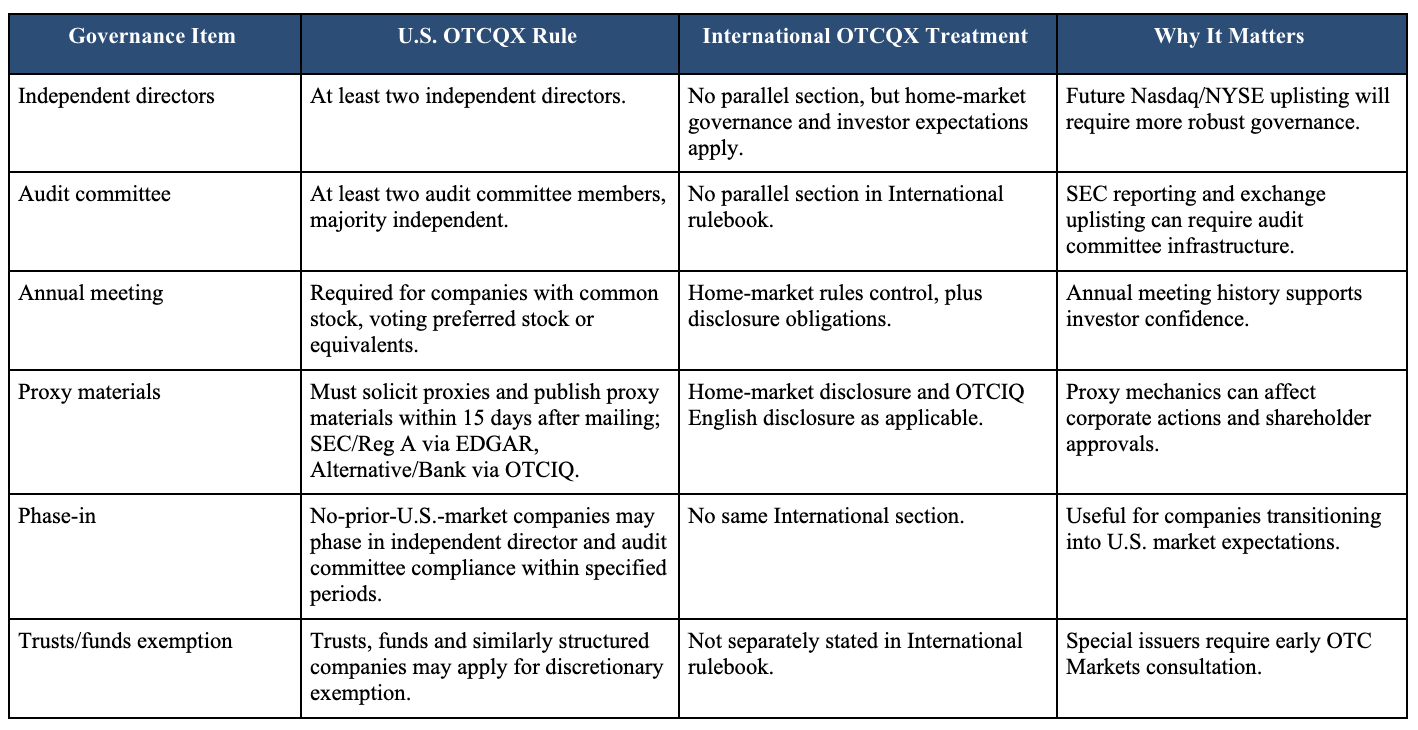

Corporate Governance and U.S. Comparative Standards

The U.S. OTCQX rules include a dedicated corporate governance section. U.S. companies must have at least two independent directors and an audit committee of at least two members, a majority of whom are independent directors. Companies with common stock, voting preferred stock or their equivalent must hold annual shareholder meetings and make annual financial reports available to shareholders at least 15 calendar days before the meeting. A company required to hold an annual meeting must solicit proxies and publish proxy materials within 15 calendar days after mailing.

The International OTCQX rulebook does not contain the same separate governance section. That does not mean governance is irrelevant for foreign issuers. A foreign issuer must remain in compliance with home-market rules, provide required disclosure, respond to regulators and maintain the credibility needed for OTC Markets review. In practice, foreign issuers seeking U.S. investors should consider adopting governance practices that are understandable to U.S. investors even when not strictly required by the International rulebook.

Governance planning is especially important if OTCQX is part of a Nasdaq or NYSE American uplisting strategy. A company that waits until the uplisting stage to recruit independent directors, form committees, prepare charters, adopt insider-trading policies and build disclosure controls may lose time. For many foreign issuers, the best approach is to use OTCQX as a controlled transition period during which the company builds U.S.-style governance progressively.

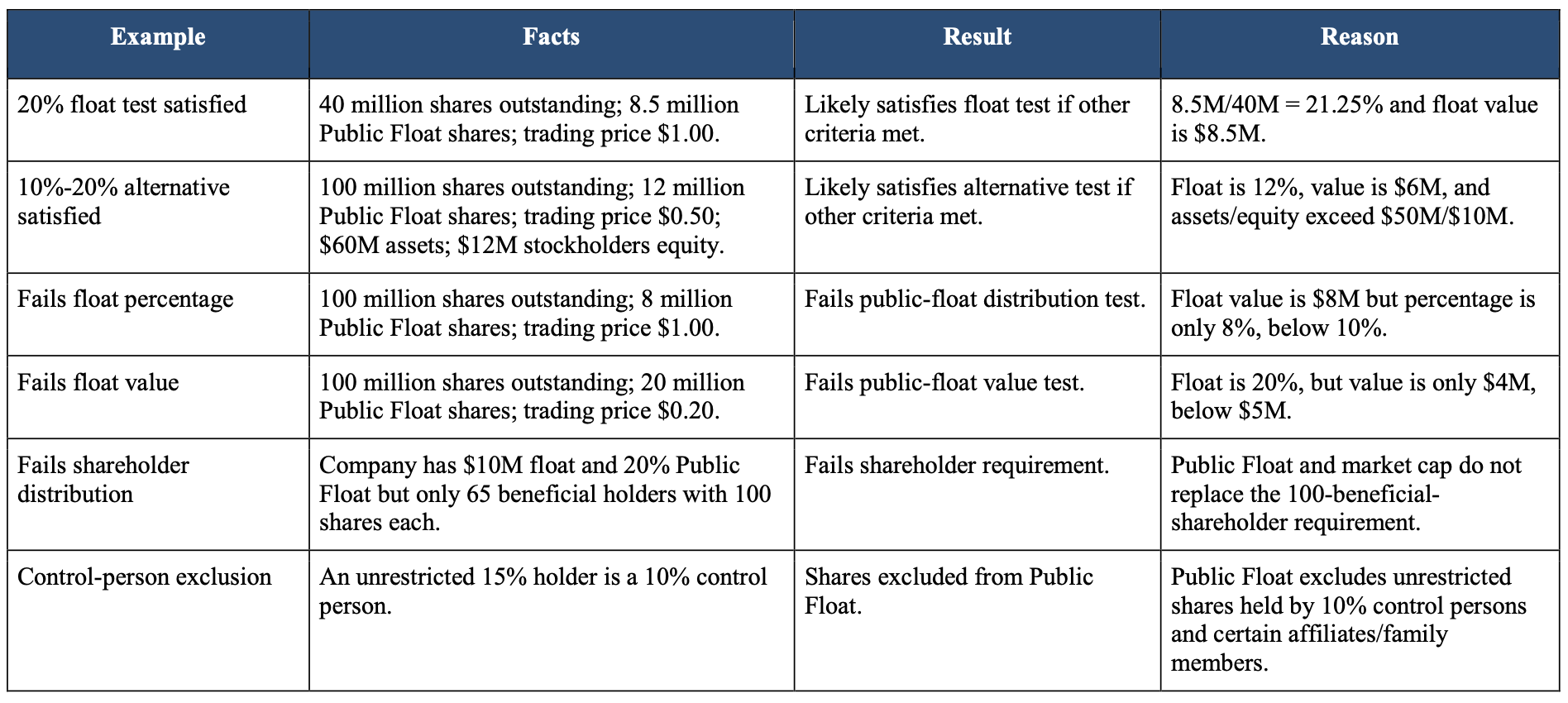

Public Float, Shareholder Distribution and Market Capitalization

The April 2026 rules make public float a two-part test. Each class of securities to be traded on OTCQX must have a market value of Public Float of at least $5 million and must satisfy a distribution test. The distribution test can be satisfied by having Public Float of at least 20% of the total class of securities outstanding. Alternatively, the company may have Public Float between 10% and 20% if it also has total assets of $50 million and stockholders’ equity of $10 million. The additional assets and equity criteria may be satisfied using unaudited interim financials.

The float calculation is not the same as the number of shares that are nominally unrestricted at the transfer agent. Public Float excludes shares subject to resale or transfer restrictions and unrestricted shares held directly or indirectly by affiliates, including officers, directors and 10% control persons, as well as certain family members. As a result, a company with a large number of issued shares may fail the public-float test if public ownership is concentrated in insiders or control persons.

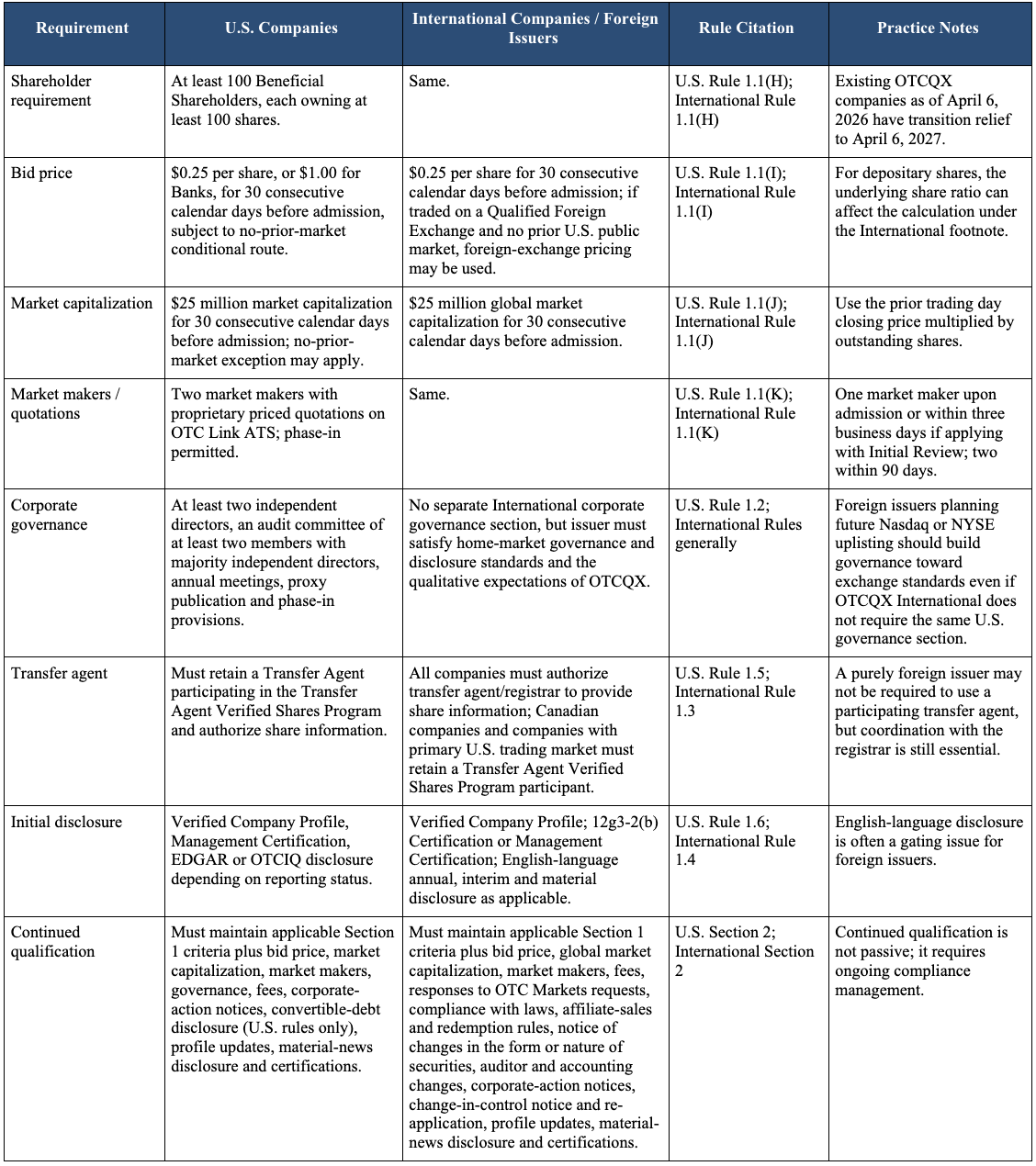

The shareholder requirement is separate. Each class of securities to be traded on OTCQX must have at least 100 beneficial shareholders, each owning at least 100 shares. This is often described as a round-lot concept, but the rule uses beneficial shareholders and 100-share ownership. Foreign issuers should reconcile registered holders, broker positions, depositary arrangements and beneficial ownership records early in the process.

Market capitalization is also a standalone requirement. International Companies must have global market capitalization of at least $25 million on each of the 30 consecutive calendar days immediately preceding admission. For ongoing qualification, the company must maintain global market capitalization of at least $10 million for at least one of every 30 consecutive calendar days, with transition relief for companies already on OTCQX as of April 6, 2026.

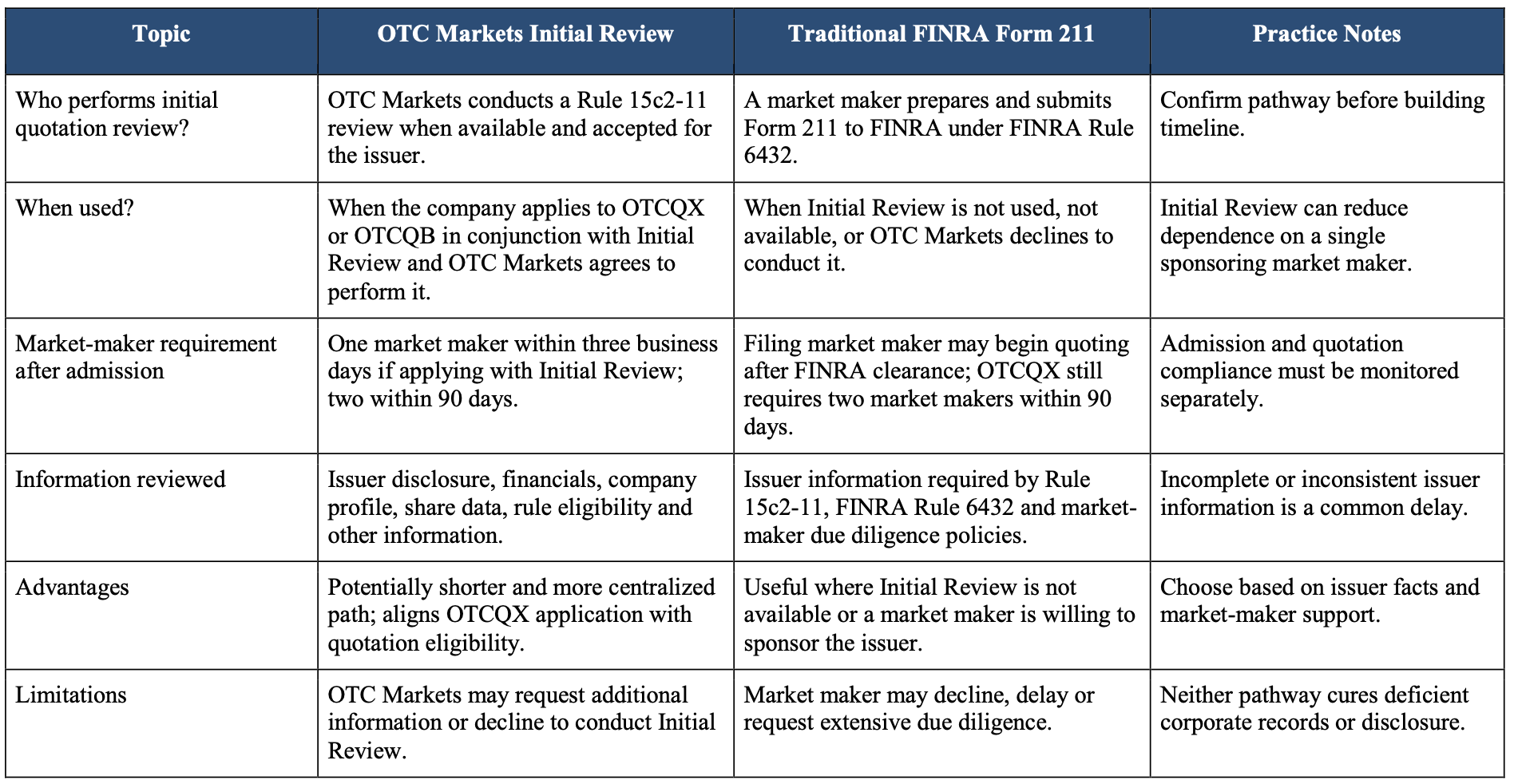

Market Makers, Rule 15c2-11, Initial Review and Form 211

Quotation is not the same as eligibility. A company may satisfy OTCQX standards but still needs broker-dealer quotation eligibility and market-maker participation. The OTCQX rules require proprietary priced quotations published by two market makers in OTC Link ATS. The company may phase in this requirement by having one market maker publish proprietary priced quotes upon admission, or within three business days of admission if the company is applying in conjunction with an Initial Review, and two market makers within 90 days of admission.

Rule 15c2-11 is the federal broker-dealer rule that governs when a broker-dealer may initiate or resume quotations for securities not listed on a national securities exchange. In a traditional Form 211 process, a market maker reviews issuer information, compiles required documentation and submits Form 211 to FINRA under FINRA Rule 6432. FINRA then reviews the submission before the market maker can begin publishing quotations.

OTC Markets’ Initial Review can materially change the process. If an issuer applies to OTCQX or OTCQB in conjunction with an OTC Markets Initial Review for quotation eligibility under Rule 15c2-11, the company may be able to avoid a separate traditional market-maker Form 211 submission. If OTC Markets does not conduct the Initial Review, or if the issuer does not apply in conjunction with that review, the issuer will need to rely on a market maker to prepare and submit the Form 211 package to FINRA.

The practical importance cannot be overstated. Market makers are not required to sponsor every issuer that asks. They may impose their own internal thresholds, request due diligence, require a legal opinion, ask for transfer-agent confirmations and decline companies with shell history, promotional history, questionable share issuances, stale financial statements or unclear control-person positions. A foreign issuer planning OTCQX should identify the quotation pathway early rather than waiting until the application is otherwise complete.

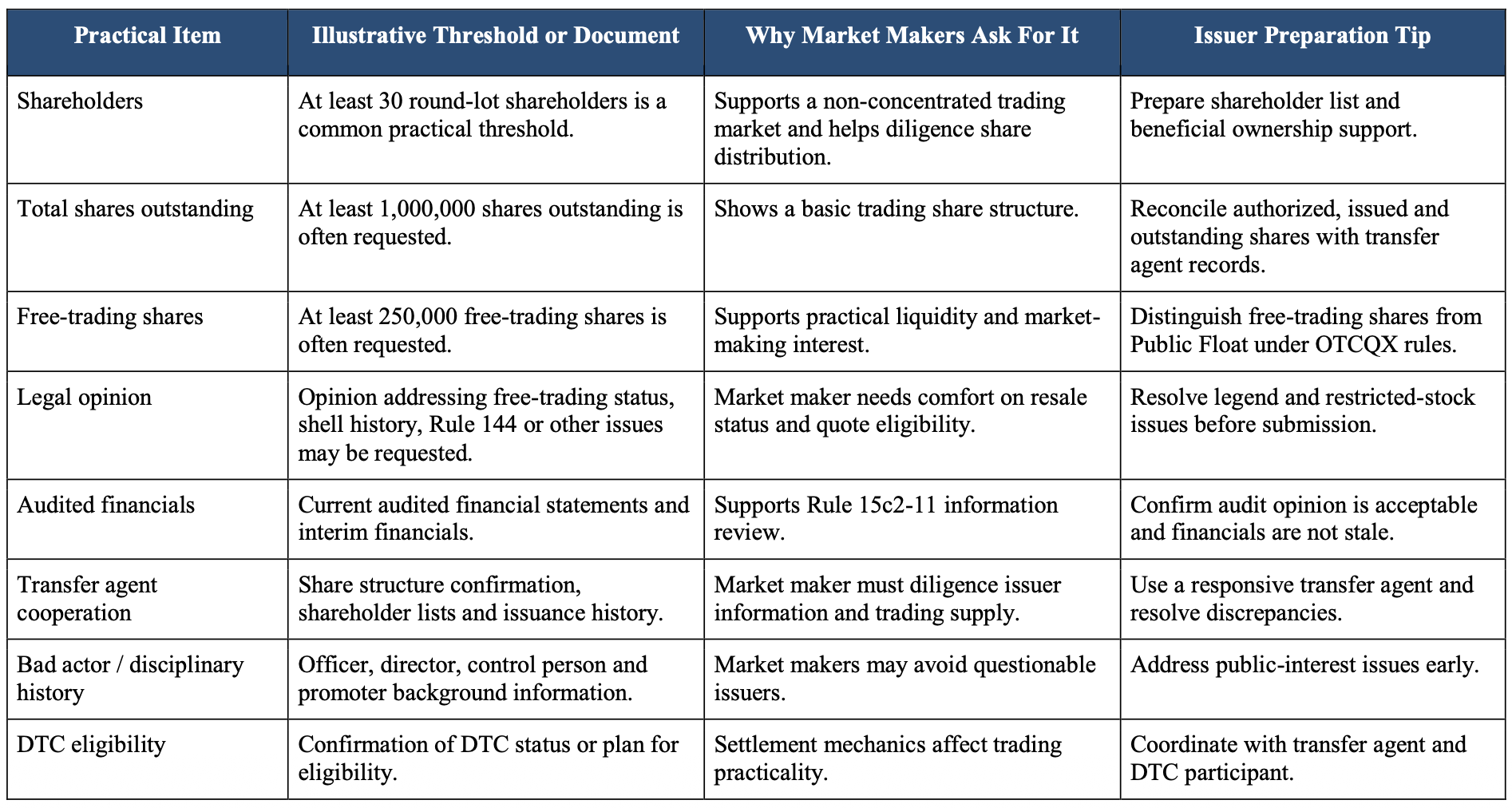

Practical Market-Maker Requirements

In addition to formal OTCQX and Rule 15c2-11 requirements, market makers often apply internal policies before agreeing to submit or support a quotation. These thresholds are not FINRA rules and are not OTCQX admission standards. They are practical considerations that can affect whether a market maker is willing to proceed. The issuer should confirm the current requirements with the market maker handling the matter.

Transfer Agent Requirements and the Verified Shares Program

Transfer-agent readiness is an operational requirement, not an administrative afterthought. For U.S. Companies, OTCQX requires the company to retain a transfer agent that participates in the Transfer Agent Verified Shares Program and to authorize the transfer agent to provide OTC Markets Group, upon request, information concerning the company’s securities, including authorized shares, issued and outstanding shares and share issuance history.

For International Companies, all companies must authorize their transfer agent or registrar to provide OTC Markets Group with securities information upon request. Canadian companies and companies with a primary trading market in the United States must retain a transfer agent that participates in the Transfer Agent Verified Shares Program. For a purely foreign issuer, the exact transfer-agent mechanics may differ, but OTC Markets still needs reliable share information.

Foreign issuers using depositary receipts, foreign registrars or home-market settlement systems should begin the transfer-agent and share-data work early. Common problems include inconsistent outstanding share numbers, unresolved restricted legends, missing issuance records, old share certificates, incomplete corporate actions, deposits held through nominees and difficulty obtaining beneficial holder support. These issues can delay both OTCQX admission and market-maker review.

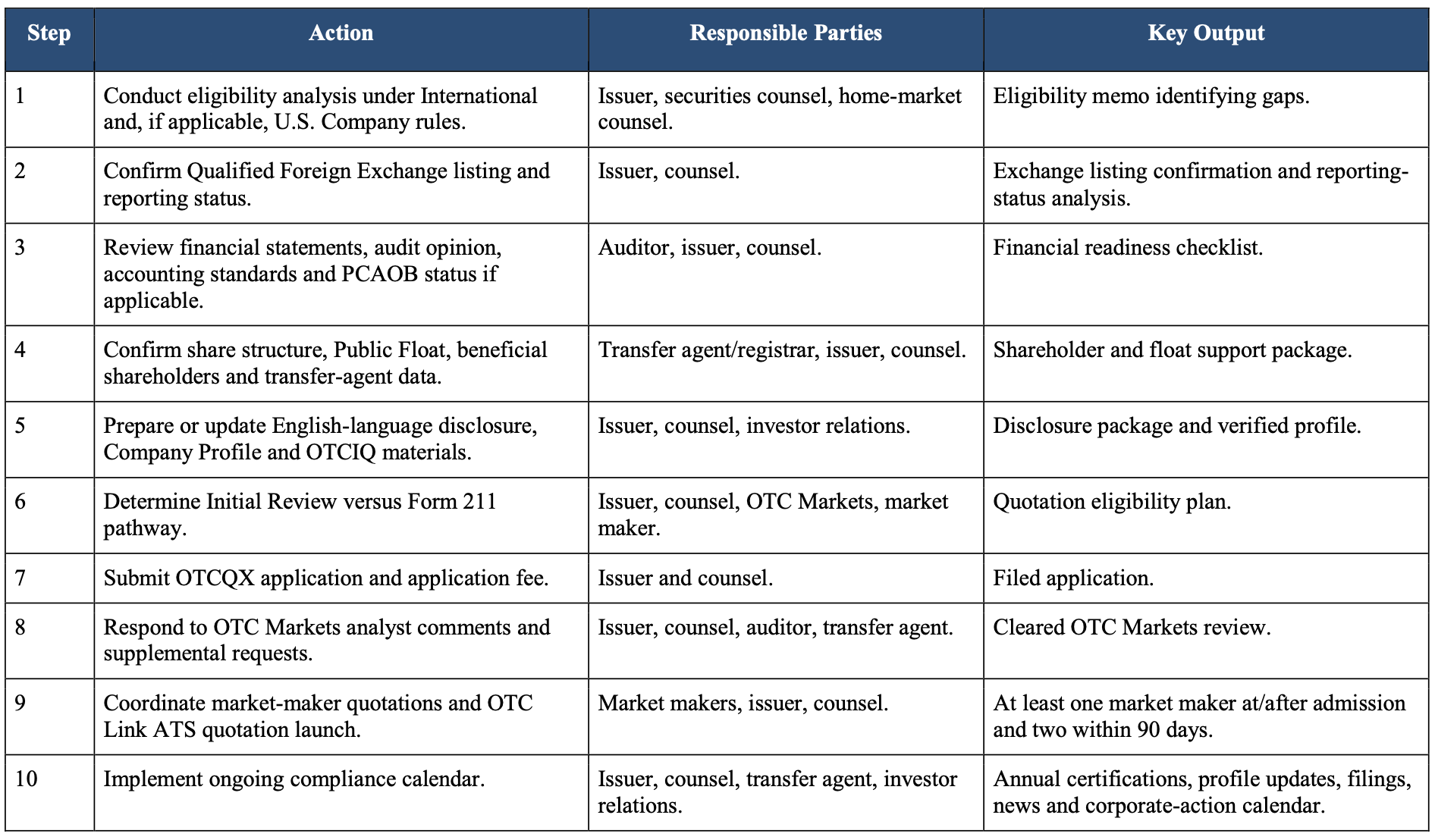

Step-by-Step OTCQX Application Process

A successful OTCQX application is usually a project rather than a single filing. The work begins with eligibility analysis and continues through application preparation, disclosure review, quotation eligibility, market-maker coordination and post-admission compliance. Foreign issuers should assign responsibility among management, securities counsel, auditors, transfer agent or registrar, home-market counsel, investor relations and any market-making or depositary participants.

The application package should be built from verifiable records. OTC Markets may request additional items during review, and inconsistencies can cause delays. A company that begins with clean corporate records, complete capitalization records, current financials, English disclosure, confirmed reporting status and an identified quotation pathway will usually have a more predictable timeline.

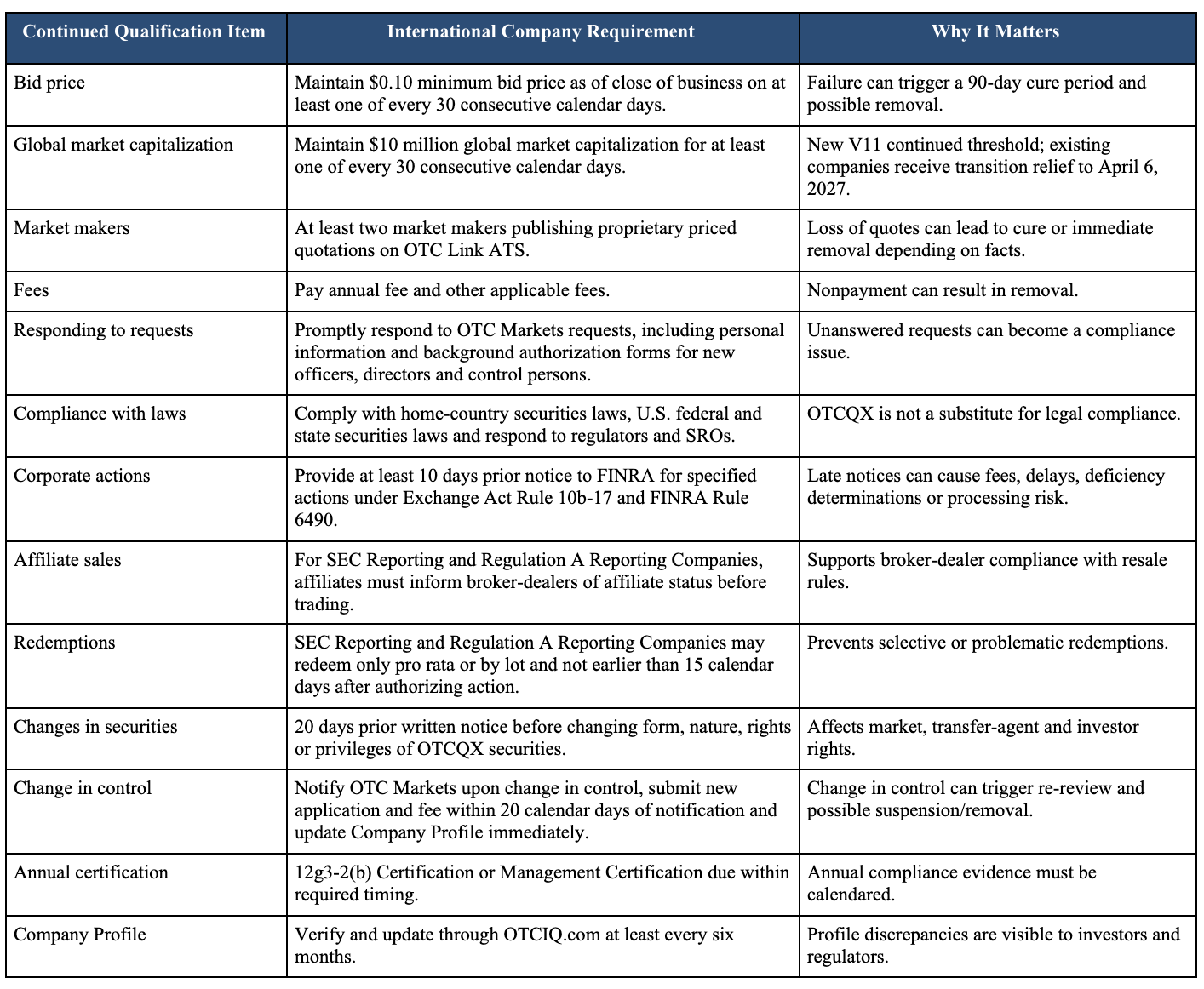

Continued Qualification and Ongoing Disclosure

OTCQX compliance does not end when trading begins. The Version 11 rules require the company to maintain compliance with applicable admission criteria and additional continued qualification requirements. For International Companies, the company must maintain a minimum bid price of $0.10 per share as of the close of business on at least one of every 30 consecutive calendar days, maintain global market capitalization of at least $10 million for at least one of every 30 consecutive calendar days, have at least two market makers publishing proprietary priced quotations on OTC Link ATS, pay annual fees, respond promptly to OTC Markets Group requests and comply with applicable securities laws.

The continued standards also cover corporate actions, affiliate sales, redemption requirements, changes in the form or nature of securities, changes in auditors, accounting changes and changes in control. A company must provide at least 10 days’ prior notice to FINRA of certain corporate actions, including dividends, stock splits, reverse splits, name changes, mergers, acquisitions, dissolutions, changes in the nature of securities, bankruptcies and liquidations. A company must provide 20 days’ prior written notice to OTC Markets Group before changing the form, nature, rights or privileges of securities traded on OTCQX.

Ongoing disclosure obligations depend on the issuer’s reporting category. International Reporting Companies must remain current and fully compliant with Rule 12g3-2(b) and publish required English-language information through OTCIQ.com. International Alternative Reporting Companies must publish required home-market reports and OTCQX Disclosure Guidelines information in English through OTCIQ.com and publish a Supplemental Report-Catch All form annually. SEC Reporting Companies must file Exchange Act reports on EDGAR. Regulation A Reporting Companies must file required EDGAR reports and quarterly Form 1-U information where applicable.

Material news also matters. An OTCQX company is expected to promptly release news or information reasonably expected to materially affect the market for its securities and to act promptly to dispel unfounded rumors that result in unusual market activity or price variations. Company profile maintenance is a separate obligation; the company must verify and update its Company Profile through OTCIQ.com at least once every six months.

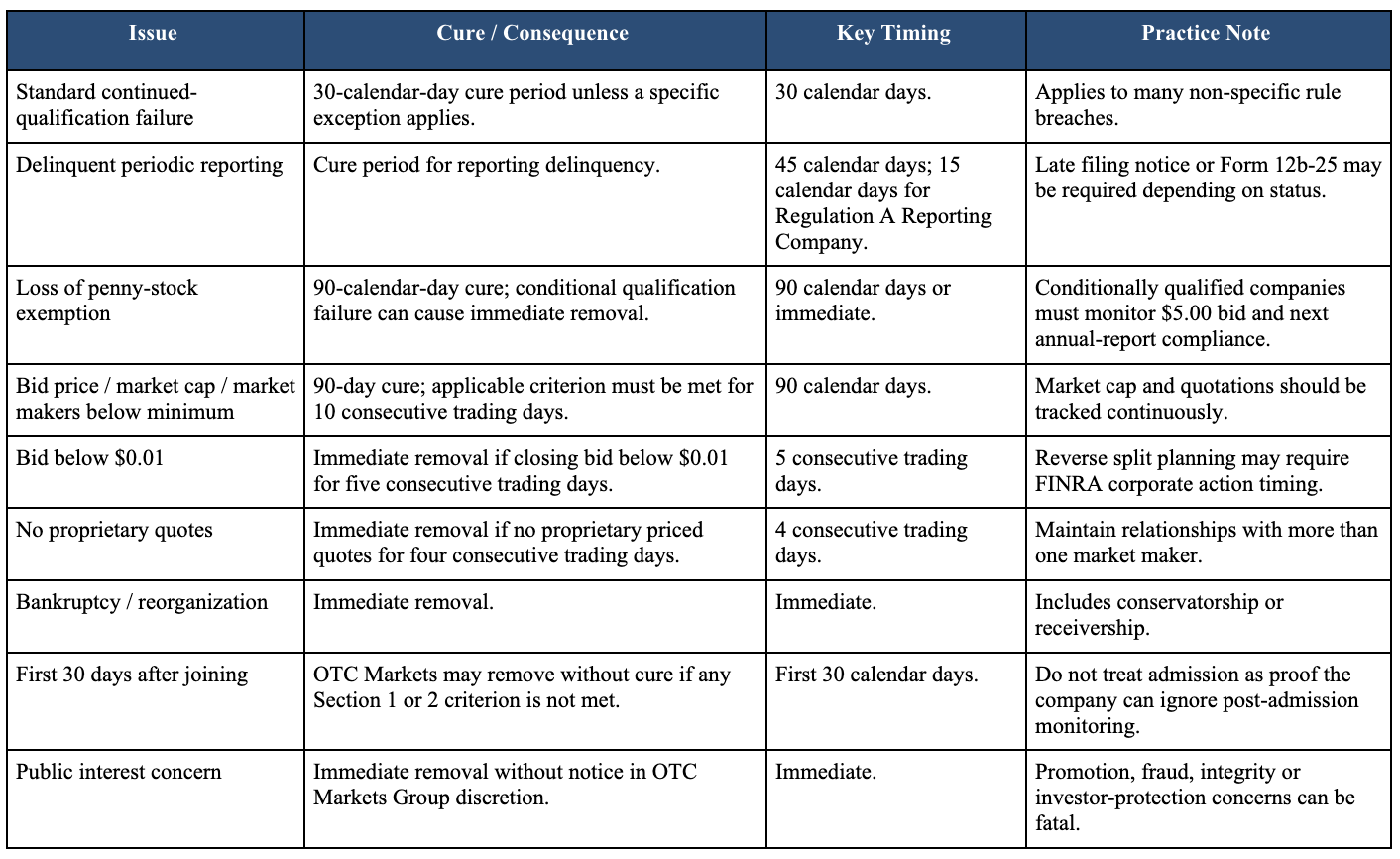

Cure Periods, Suspension, Removal and Requalification

The removal provisions should be read before a company applies, not after a deficiency occurs. OTC Markets Group may remove a company from OTCQX for failure to meet a continued qualification requirement, nonpayment of fees or failure to comply with other OTCQX obligations. The standard cure period is 30 calendar days, but several specific exceptions apply. Reporting delinquency generally receives 45 calendar days, with a shorter 15-calendar-day cure period for Regulation A Reporting Companies under Rule 15c2-11. Loss of a penny-stock exemption generally receives 90 calendar days, but failure of conditional qualification can result in immediate removal.

Certain events can result in immediate removal. If the closing bid price falls below $0.01 for five consecutive trading days, the security can be removed immediately. If there are no proprietary priced quotes for four consecutive trading days, the security can be removed immediately. Bankruptcy or reorganization proceedings can also result in immediate removal. In addition, OTC Markets Group may remove securities immediately and without notice if continued inclusion would impair the reputation or integrity of OTC Markets Group or be detrimental to investors.

Requalification is possible in some cases. A company removed from OTCQX within the past 180 calendar days may request readmission in writing if it meets all admission requirements, has not undergone a change in control, loss of proprietary quote eligibility or other material change since removal, and was not removed for nonpayment of fees. If the company has been removed for more than 180 days or does not meet those conditions, it must submit a new application, application fee and annual fee.

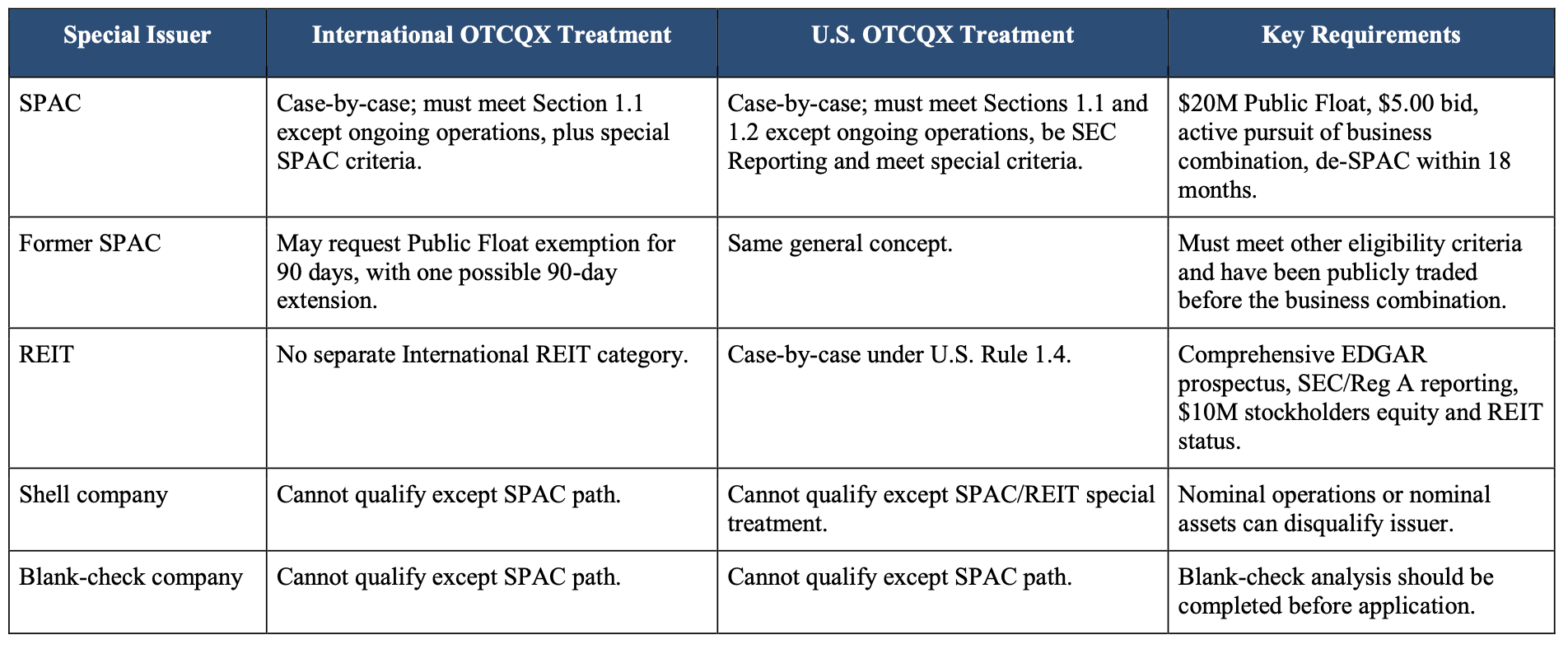

SPACs, REITs and Special Issuer Categories

OTCQX generally excludes shell companies and blank-check companies, but the rules contain special treatment for SPACs. Under the International Companies rules, OTC Markets Group may consider on a case-by-case basis a SPAC with substantial cash or investments and no prior operating history. The SPAC must satisfy OTCQX eligibility requirements other than the ongoing operations requirement and must satisfy additional requirements, including at least $20 million in market value of Public Float, a $5.00 bid price for 30 consecutive calendar days before admission and active pursuit of a business combination. A SPAC admitted to OTCQX must enter into an agreement with a target company and complete a de-SPAC transaction within 18 months of initial quotation in the over-the-counter market, consistent with Rule 15c2-11.

A former SPAC that has completed or is in the process of completing a business combination may request an exemption from the Public Float requirement. If granted, the qualifying company may trade on OTCQX for 90 calendar days before being required to comply with the Public Float requirement, and may be granted one additional 90-day extension at OTC Markets Group’s sole discretion.

REIT treatment appears in the U.S. OTCQX rules and is included here because it is part of the complete OTCQX framework. OTC Markets may consider a REIT with no operating history but a comprehensive prospectus filed on EDGAR. The REIT must meet the U.S. eligibility and governance requirements other than ongoing operations, must be an SEC Reporting Company or Regulation A Reporting Company, must report stockholders’ equity of at least $10 million in its most recent audited financial statements or qualifying pro forma financial statements filed on EDGAR, and must maintain REIT status under the Internal Revenue Code. The International rulebook does not contain a parallel REIT category.

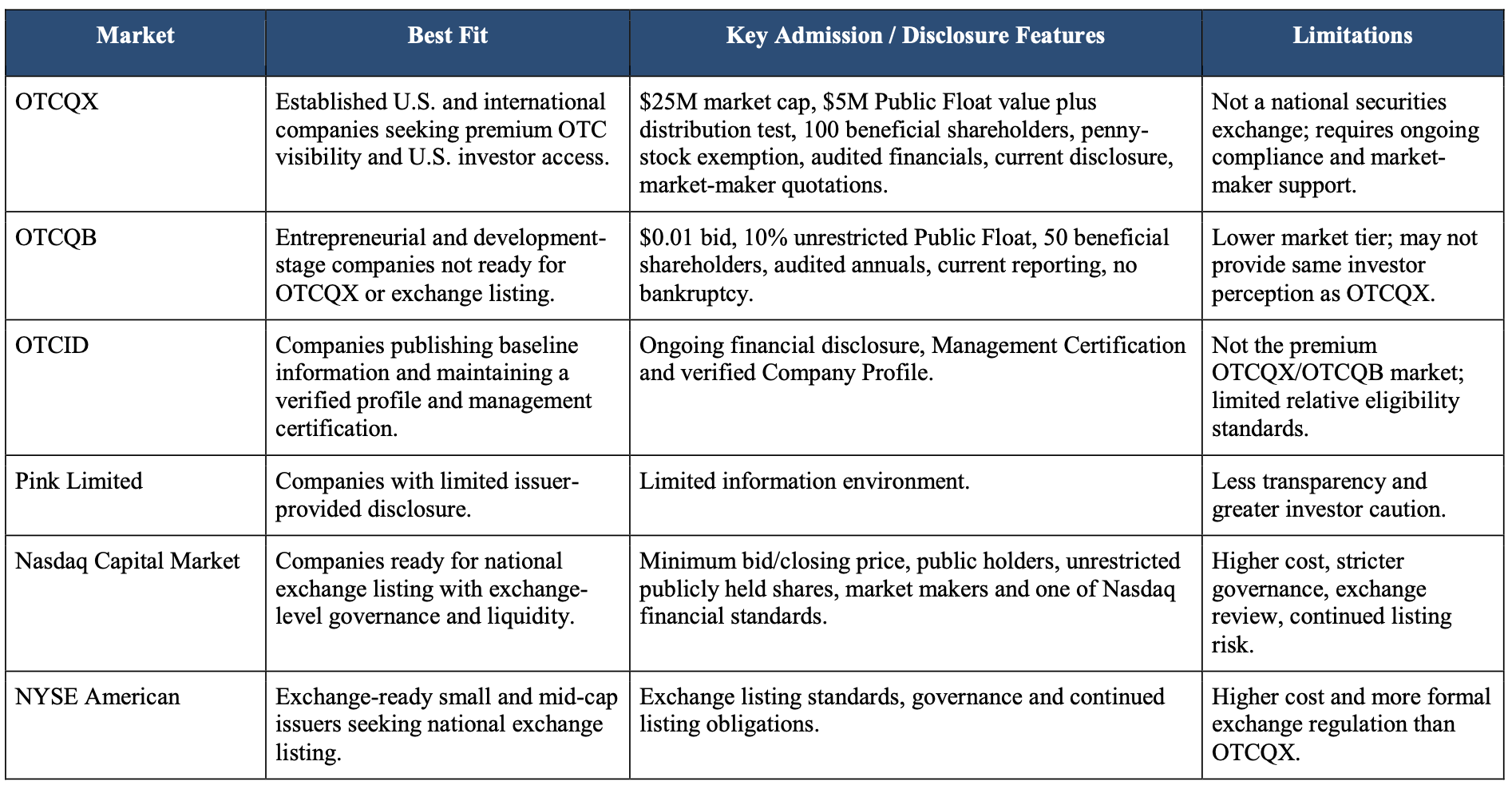

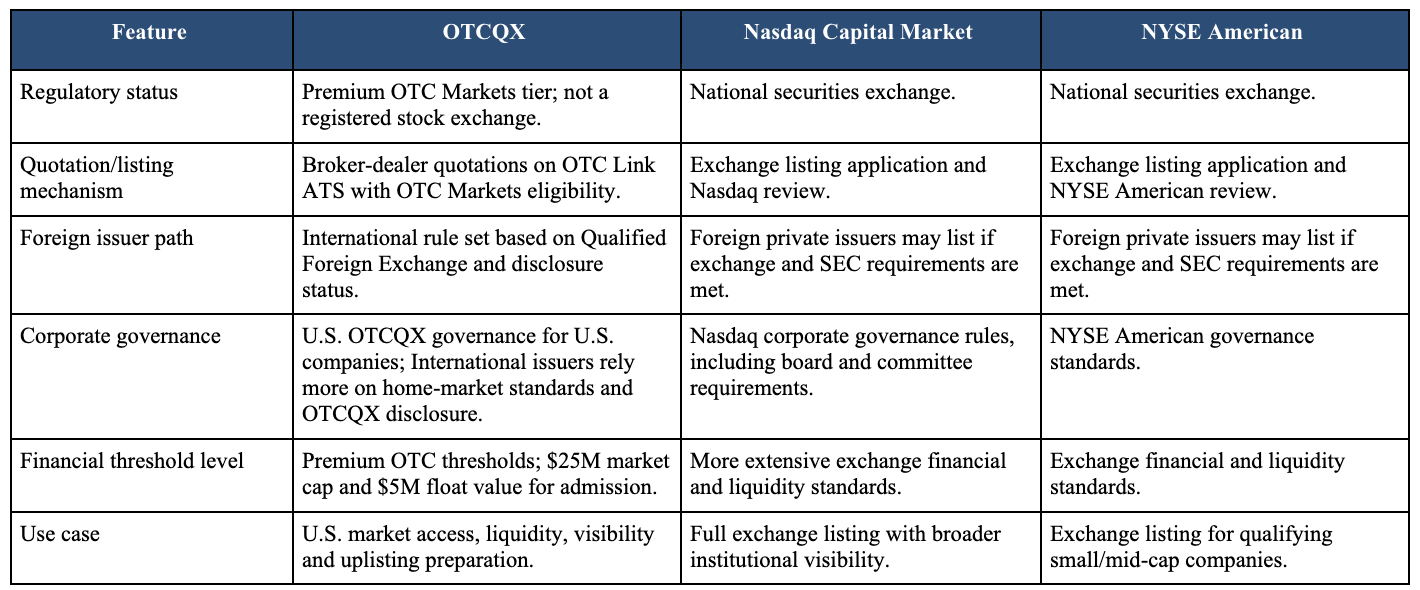

Comparison Charts: OTCQX, OTCQB, OTCID, Nasdaq and NYSE American

Comparison charts are helpful, but they should not be used as a substitute for a legal eligibility review. OTCQX, OTCQB and OTCID are not national securities exchanges. They are OTC Markets tiers with their own admission, disclosure and quotation standards. Nasdaq and NYSE American are national securities exchanges with separate exchange listing, corporate governance, disclosure and continued listing rules. The chart below is designed for strategic planning, not final eligibility advice.

The OTCQB and OTCID information below is included because companies that cannot satisfy the 2026 OTCQX requirements may need to consider another OTC Markets tier. OTCQB standards are lower than OTCQX but still require current reporting, audited annual financial statements, $0.01 bid price, 10% unrestricted Public Float, 50 beneficial shareholders each owning at least 100 shares and no bankruptcy (verified against OTCQB Rules V6, also effective April 6, 2026). OTCID is a baseline disclosure market rather than a premium eligibility market.

OTCQX vs. Nasdaq Capital Market and NYSE American

OTCQX is often described as a stepping-stone to Nasdaq or NYSE American, but the standards are not interchangeable. Nasdaq Capital Market initial listing rules require a company to meet all general initial listing requirements and at least one financial standard, including requirements relating to bid or closing price, unrestricted publicly held shares, round-lot holders, market makers, trading volume if already OTC, and stockholders’ equity, market value of listed securities or net income. NYSE American uses its own company guide and qualitative review. Exchange uplisting also generally requires a stronger governance framework, higher public float, transfer-agent and DTC readiness, SEC reporting, underwriter or financial advisor involvement in some transactions, and active exchange review.

The practical point is that OTCQX can help prepare a company for exchange listing, but it does not guarantee exchange eligibility. A foreign issuer that views OTCQX as a bridge should design its corporate structure, financial reporting, board composition, shareholder distribution, investor relations and public disclosure program with the future exchange target in mind.

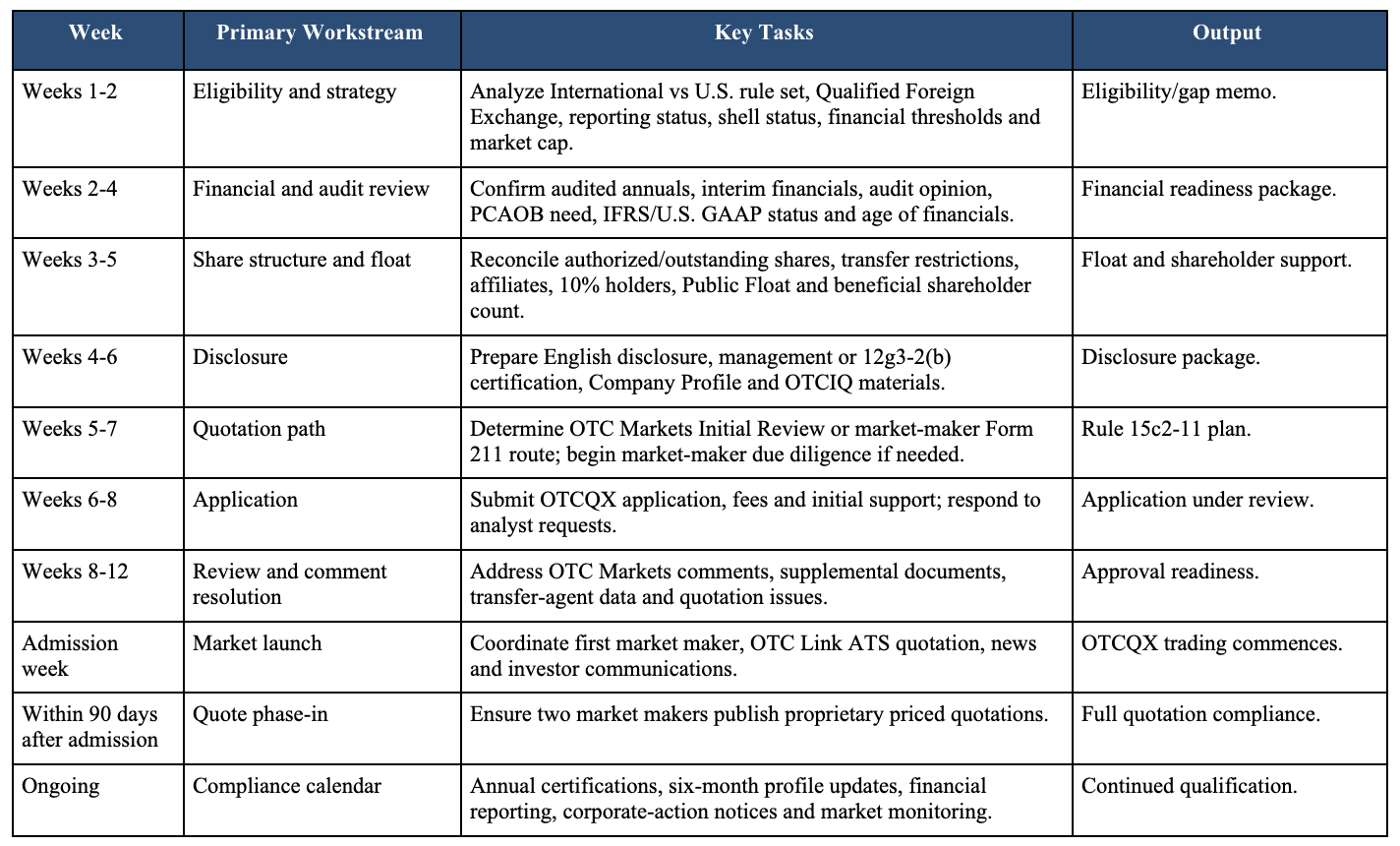

Practical Timeline

The timeline for OTCQX depends on the issuer’s starting condition. A foreign issuer with current audited financial statements, a clean home-market disclosure record, a Qualified Foreign Exchange listing, sufficient market capitalization, clear Public Float, more than 100 beneficial shareholders, cooperative transfer agent or registrar, English disclosure and an identified Initial Review or market-maker pathway may move faster. A company with stale financials, uncertain float, old corporate actions or no market-maker interest can take significantly longer.

The following timeline assumes that the issuer is already foreign-listed and is working toward OTCQX admission in an organized process. It is intentionally conservative because cross-border disclosure, transfer-agent coordination and quotation review often take longer than management expects.

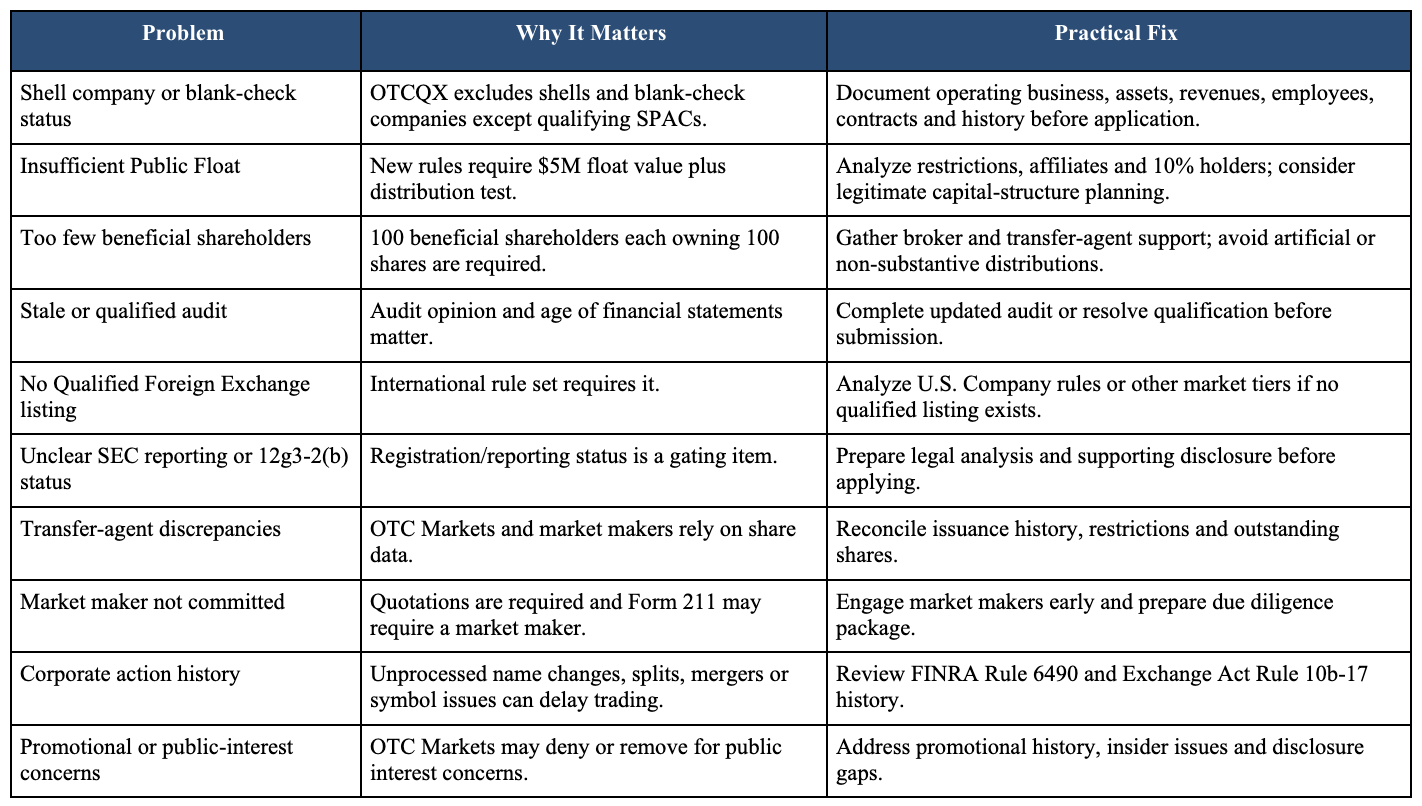

Common Reasons OTCQX Applications Are Delayed or Denied

Most OTCQX delays are predictable. They arise because the company begins the application before it has confirmed eligibility or because management assumes that a successful home-market listing automatically solves U.S. trading requirements. OTCQX review is narrower than an SEC registration review, but it still requires reliable disclosure, financial statements, share data, market-maker support and rule compliance.

The most serious problems usually involve shell status, undisclosed control persons, questionable share issuances, stale or unacceptable audits, inadequate public float, insufficient shareholder distribution, lack of a Qualified Foreign Exchange listing, unsupported Rule 12g3-2(b) status, unresolved corporate actions, transfer-agent discrepancies or promotional history. Foreign issuers should also expect questions if English-language disclosure is incomplete or if home-market filings do not clearly describe the company’s business, capitalization, management and financial condition.

Frequently Asked Questions

Can a foreign issuer qualify for OTCQX in 2026?

Yes, if it meets the International Companies requirements, including a Qualified Foreign Exchange listing, current reporting obligations, an eligible reporting or exemption status, penny-stock exemption, audited financials, public float, shareholder distribution, bid price, market capitalization, market-maker quotation and disclosure requirements.

Is OTCQX a national securities exchange?

No. OTCQX is a premium market operated by OTC Markets Group. It is not Nasdaq, NYSE or NYSE American and is not a registered stock exchange.

Does a foreign issuer have to be listed on a Qualified Foreign Exchange?

Under the OTCQX International Companies rules, yes. The company must be listed on a Qualified Foreign Exchange and current in its reporting obligations. A foreign-incorporated company without such listing must analyze whether it is treated as a U.S. Company under the U.S. OTCQX rules or whether another tier is available.

Can SEC reporting satisfy the reporting-status requirement?

Yes, SEC Reporting Company status is one of the recognized reporting-status categories. However, under the International rule set, it does not replace the separate Qualified Foreign Exchange listing requirement.

Can a shell company qualify for OTCQX?

No, shell companies and blank-check companies do not qualify, except that SPACs may be considered under special rules.

Can a SPAC qualify for OTCQX?

Yes, on a case-by-case basis if it has substantial cash or investments, satisfies the applicable OTCQX criteria except ongoing operations, meets special Public Float and bid-price requirements and is actively pursuing a business combination.

Can a Regulation A issuer qualify for OTCQX?

Yes, a Regulation A Reporting Company can be an eligible category, but Regulation A is generally available only to U.S. and Canadian issuers that meet the Regulation A eligibility requirements.

What is the minimum OTCQX bid price for foreign issuers?

The admission bid price is $0.25 per share for each of the 30 consecutive calendar days immediately before admission. For securities traded on a Qualified Foreign Exchange with no prior U.S. public market, foreign exchange pricing may be used.

What is the OTCQX market capitalization requirement?

For International Companies, the issuer must have global market capitalization of at least $25 million for each of the 30 consecutive calendar days before admission. Continued qualification requires $10 million global market capitalization for at least one of every 30 consecutive calendar days.

What is the OTCQX Public Float requirement?

Each class must have at least $5 million market value of Public Float and either at least 20% Public Float or 10%-20% Public Float with $50 million total assets and $10 million stockholders equity.

How many shareholders are required?

Each class of securities to be traded on OTCQX must have at least 100 beneficial shareholders, each owning at least 100 shares.

What is a beneficial shareholder?

A beneficial shareholder is a person who directly or indirectly has or shares voting power or investment power over the security.

Do foreign issuers need PCAOB audits?

Only if the International Company has an SEC reporting obligation. International Companies without SEC reporting obligations are exempt from the PCAOB auditor requirement under the OTCQX International rules.

Can IFRS financial statements be used?

Yes. International Companies may prepare periodic financial statements under U.S. GAAP, IFRS or IFRS equivalent, as applicable.

Are interim financial statements required?

Interim financial reports may be unaudited but must include a balance sheet, income statement and statement of cash flows for the required periods.

Do foreign issuers need two market makers?

Yes. OTCQX requires proprietary priced quotations by two market makers on OTC Link ATS, with phase-in permitting one market maker upon admission (or within three business days of admission if applying in conjunction with an Initial Review) and two within 90 days.

When is Form 211 required?

If the issuer does not apply in conjunction with an OTC Markets Initial Review for Rule 15c2-11 quotation eligibility, or if OTC Markets declines to conduct the Initial Review, the issuer generally must rely on a market maker to submit Form 211 to FINRA.

What is OTC Markets Initial Review?

Initial Review is OTC Markets Group’s review of issuer disclosure and information under Rule 15c2-11 to determine whether the securities are eligible for public broker-dealer quotations.

How long does OTCQX approval take?

Timing varies. A clean foreign issuer may move more efficiently, but cross-border disclosure, transfer-agent issues, audit review, float analysis and quotation eligibility can extend the process. A practical planning window is often several weeks to several months.

What happens after OTCQX approval?

The issuer must maintain market makers, bid price, market capitalization, current disclosure, certifications, Company Profile updates, corporate-action notices, fee payments and other continued qualification requirements.

What happens if the company drops below the continued market capitalization requirement?

The rules provide a 90-day cure period for market capitalization deficiencies, during which the company must meet the applicable criteria for 10 consecutive trading days.

What corporate actions require attention?

Dividends, stock splits, reverse splits, name changes, mergers, acquisitions, dissolutions, changes in the nature of securities, bankruptcies and liquidations can require FINRA notice and OTC Markets coordination.

Can a company be removed immediately?

Yes. Immediate removal can occur for bid below $0.01 for five consecutive trading days, no proprietary quotes for four consecutive trading days, bankruptcy and public-interest concerns, among other circumstances.

Is there still an OTCQX International Premier tier?

No separate OTCQX International Premier tier appears in the April 6, 2026 Version 11 OTCQX Rules for International Companies. Older references should be updated.

Should a foreign issuer choose OTCQX or OTCQB?

OTCQX is the premium tier and requires higher market cap, float, shareholder and financial standards. OTCQB may be more appropriate for earlier-stage issuers that cannot satisfy OTCQX.

Is OTCID a substitute for OTCQX?

No. OTCID is a baseline disclosure market, not the OTCQX premium market. It can be useful for companies that need to provide current information but do not yet meet OTCQX or OTCQB standards.

Can OTCQX help with future Nasdaq uplisting?

Yes, it can help build trading history, U.S. visibility, disclosure discipline and investor familiarity, but it does not guarantee Nasdaq or NYSE American eligibility.

Who should manage an OTCQX application?

Management, securities counsel, home-market counsel, auditors, transfer agent or registrar, market makers and investor relations should coordinate from the beginning. OTCQX is a multidisciplinary project.

This article is general information and not legal advice. OTCQX eligibility, Rule 15c2-11 quotation, Form 211, securities-law status, home-market compliance, transfer-agent requirements and corporate actions should be reviewed based on the issuer’s specific facts.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com