The United States Supreme Court is once again poised to reshape the securities enforcement landscape. With its agreement to hear a case addressing the scope of the Securities and Exchange Commission’s disgorgement authority, the Court is expected to resolve a growing circuit split that has created uncertainty for regulators, issuers, and securities professionals. Coupled with the Court’s recent decision limiting the SEC’s use of administrative law judges, these developments represent a significant recalibration of federal securities enforcement.

Key Takeaways for Investors and Market Participants

- Disgorgement that does not return money to harmed investors risks becoming punitive rather than protective.

- The Supreme Court may require proof of investor harm before disgorgement can be imposed.

- A narrower disgorgement standard could reduce overreach in SEC enforcement actions.

- Jury trial rights and constitutional safeguards are playing an increasing role in securities enforcement.

- Investors benefit most when enforcement remedies prioritize restitution over revenue generation.

Background: The Evolution of SEC Disgorgement Authority

Disgorgement has long been a central enforcement remedy used by the SEC to deprive alleged wrongdoers of ill-gotten gains. Historically, courts permitted disgorgement as an equitable remedy even though it was not explicitly authorized by statute. That changed in part with the Supreme Court’s 2020 decision in Liu v. SEC, which affirmed that disgorgement could be awarded as equitable relief, but only if it adhered to traditional equity principles. “When disgorgement fails to compensate investors, it ceases to be equitable and begins to look like punishment by another name.”

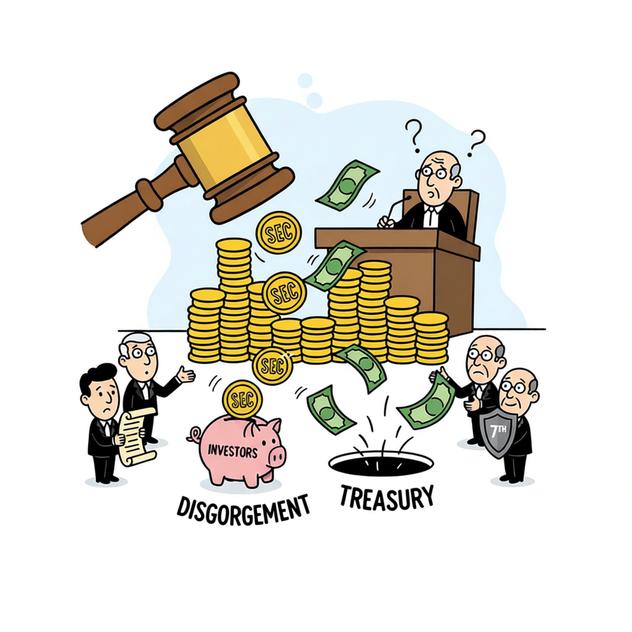

Why Disgorgement Without Investor Compensation Is Fundamentally Unfair

A central criticism of modern SEC disgorgement practice is that, in many cases, disgorged funds are not returned to harmed investors but instead are deposited into the U.S. Treasury. When disgorgement is divorced from investor compensation, it resembles a civil penalty while avoiding the procedural protections that normally accompany punitive sanctions. This outcome directly conflicts with the SEC’s core mission of investor protection. “An enforcement remedy that enriches the Treasury but leaves investors whole only in theory undermines public confidence in securities regulation.”

Requiring defendants to surrender profits where no investor suffered a quantifiable loss raises serious fairness and proportionality concerns. Equity has historically focused on restoration, not deterrence for deterrence’s sake. Allowing disgorgement without investor harm transforms the remedy into a tool of punishment, contradicting the SEC’s stated purpose and stretching equitable principles beyond recognition.

The Circuit Split on Investor Harm Requirements

Following Liu, federal courts diverged on whether the SEC must prove that investors suffered actual pecuniary harm to obtain disgorgement. The Second Circuit has taken the position that disgorgement is improper absent proof of investor losses, reasoning that equitable relief must be restorative rather than punitive. By contrast, the First and Ninth Circuits have held that disgorgement remains permissible so long as it is limited to a defendant’s net profits, even if direct investor losses are difficult to quantify or prove.

Impact of SEC v. Jarkesy on Enforcement Proceedings

In SEC v. Jarkesy, the Supreme Court held that defendants facing SEC civil penalties for securities fraud are entitled to a jury trial under the Seventh Amendment. This decision reinforces the principle that when enforcement remedies operate as punishment, constitutional protections must apply. The case further highlights why disgorgement that functions like a penalty cannot escape scrutiny simply by being labeled equitable. “If disgorgement walks like a penalty and talks like a penalty, constitutional safeguards should follow.”

What Comes Next for SEC Enforcement

Taken together, the Supreme Court’s recent and pending decisions signal a broader trend toward limiting agency enforcement discretion and reaffirming investor-focused remedies. If disgorgement is to survive as an equitable tool, it must meaningfully benefit investors rather than serve as a substitute revenue stream for the government. Market participants should monitor these developments closely and reassess compliance and enforcement risk accordingly.

This securities law blog post is provided as a general informational service to clients and friends of Hamilton & Associates Law Group. It should not be construed as and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship.

If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com