Regulation S-K Item 401 is an SEC requirement designed to provide investors with essential background information on the individuals leading a company. This disclosure appears in registration statements, proxy statements, and annual reports (Form 10-K), serving as a primary tool for stockholders to evaluate management quality and board oversight.

Core Requirements of Item 401 Disclosure

Strong disclosure under Item 401 should be clear, consistent, and complete without overstating accomplishments. The foundational requirements include:

- Identification: Companies must provide full proper names and ages (where required) for directors, executive officers, and director nominees.

- Positions and Offices: Disclosure must detail all roles held at the registrant, including specific titles and periods of service.

- Selection Arrangements: Any “arrangements or understandings” involving the selection of a director or officer (such as rights held by a specific security holder) must be disclosed.

- Family Relationships: Relationships by blood, marriage, or adoption (up to the level of first cousin) among directors and officers must be reported.

Reporting Business Experience and Timelines

The “business experience” section is the core of most professional biographies. To avoid common drafting errors, companies should follow these guidelines:

The Five-Year Lookback

Item 401 specifically requires a description of business experience during the past five years, including principal occupations and employment. While companies may include older experience for context, they must ensure the added information is not misleading by omission.

Precision in Drafting

Vague timelines are a frequent point of SEC criticism.

- Use Specific Dates: Best practice is to include the month and year for start and end points of each role.

- Describe Responsibilities: If a title is not self-explanatory, provide a brief description of the person’s actual responsibilities.

Director Qualifications and External Directorships

Beyond internal roles, the SEC focuses on the external professional footprint of directors:

- Public Company Boards: For directors and nominees, companies must disclose other public company directorships held during the past five years.

- Specific Qualifications: Companies must explain the specific skills, attributes, or experience that qualify an individual to serve on the board in light of the company’s specific business and structure.

Legal Proceedings and Integrity

Item 401 requires disclosure of specific legal or regulatory proceedings from the past ten years. This is not a general character statement but a factual account of events material to evaluating a person’s integrity or ability. These disclosures should be dated and purely factual, avoiding advocacy or speculation.

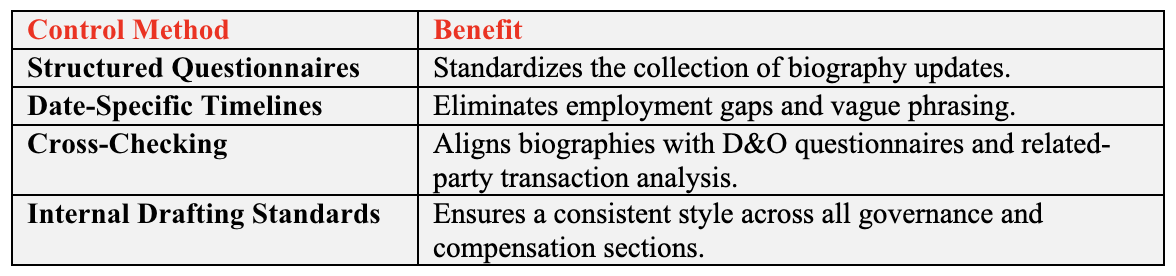

Best Practices for Compliance Controls

To ensure consistency and reduce the risk of SEC comments, companies should implement the following practical controls:

Frequently Asked Questions (FAQ)

What is Regulation S K Item 401?

It is an SEC requirement to disclose background information about directors, executive officers, and director nominees to investors.

Which SEC filings typically include Item 401 biographies?

Registration statements, proxy or information statements, and Form 10 K when Part III information is provided directly rather than incorporated by reference.

What business experience timeframe is required?

A person’s business experience during the past five years, including principal occupations and employment.

How detailed should the job descriptions be?

Detailed enough to explain the nature of the person’s responsibilities when the title or company name does not make the role obvious.

Can a company include experience from more than five years ago?

Yes, but the disclosure should remain balanced and not misleading by omission.

What family relationships must be disclosed?

Family relationships generally include relationships by blood, marriage, or adoption that are not more remote than first cousin.

What board service must be disclosed?

Other directorships of public companies held during the past five years.

What are common drafting mistakes?

Unclear timelines, gaps in employment history, generic director qualification statements, inconsistent inclusion of education, and biographies that read like marketing materials rather than disclosure.

Consult the SEC’s Compliance and Disclosure Interpretations for guidance on complex reporting scenarios.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com