Recent SEC orders suggest a more practical path to relief for individuals seeking reentry after administrative bars, including penny stock bars, and for professionals seeking reinstatement after Rule 102(e) suspensions.

For years, professionals facing an SEC administrative bar viewed reentry as “practically elusive,” especially when a permanent bar was involved. While relief was technically available, the process was often so slow that sanctions felt career-ending in practice.

However, a recent wave of orders suggests the SEC is adopting a more workable, text-centered approach to requests for relief.

Why the SEC’s Shift Matters

The Commission has recently granted relief across several categories, including:

- Permanent industry bars.

- Penny Stock bars.

- Rule 102(e) suspensions affecting accountants.

Instead of relying on a nearly impossible “extraordinary-circumstances” standard, the SEC is now focusing on supervision, rehabilitation, and investor protection.

The practical consequences are significant. Administrative bars do not operate in a vacuum. They often trigger collateral disabilities that affect offerings, advisory activity, SRO participation, fund service roles, and other forms of market access. Penny stock bars deserve special attention because they can reach well beyond public microcap promotions. They can interfere with capital-raising plans, private placements, and future issuer roles where the applicant is expected to operate outside the classic penny stock market.

The New “Public Interest” Framework

Under Rule 193, the SEC now evaluates whether a proposed association is consistent with the public interest. This allows for a case-by-case, risk-based analysis rather than requiring “extraordinary circumstances.”

The Roadmap to Reentry

According to recent orders like Denha, the SEC looks at several practical factors when considering an application:

- Severity of misconduct: The nature and scope of the original violation.

- Elapsed time: How much time has passed since the order.

- Compliance & Restitution: Whether the applicant complied with the bar and paid all sanctions/penalties.

- Supervisory Structure: The strength and credibility of the proposed monitoring framework.

- Remorse: Evidence of genuine rehabilitation and regret.

Case Spotlights: 2025 Breakthroughs

Recent decisions illustrate how this new openness applies across different securities activities.

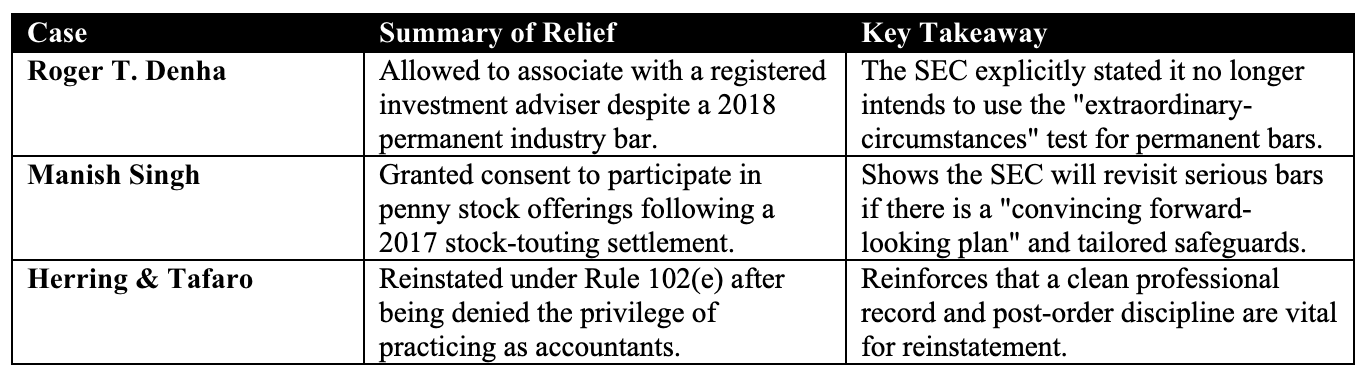

Roger T. Denha

Roger T. Denha is the most important recent order in this area. In April 2025, the SEC allowed Denha to associate with a registered investment adviser despite a permanent industry bar imposed in 2018.

The underlying SEC case found that Denha engaged in fraudulent trade allocation by purchasing securities in an omnibus account and allocating profitable trades to favored accounts after price movement was known. The 2018 order imposed a cease-and-desist order, a broad securities-industry bar, a penny stock bar, disgorgement of $412,230, prejudgment interest of $35,388, and a civil penalty of $169,000.

The application succeeded because it was concrete. Denha proposed a specific role with enhanced oversight, including by a chief compliance officer and an outside compliance firm. The Commission also credited the passage of time, timely payment of the penalty, compliance with the existing bar, charitable activity, and meaningful remorse.

Most importantly, the order states that the Commission no longer intends to use the extraordinary-circumstances test when evaluating applications for reentry from permanent bars.

Manish Singh

In April 2025, the Commission granted Manish Singh consent to participate in penny stock offerings after a five-year penny stock bar. According to the SEC, Singh was paid for stock promotion publications, many of which either failed to disclose compensation or misstated that the authors were not compensated.

Singh agreed to a cease-and-desist order, a five-year penny stock bar with a right to seek reentry, a five-year officer-and-director bar, disgorgement of $1,750,000, prejudgment interest of $151,676.94, and a civil monetary penalty of $1,000,000.

The 2025 relief order is especially important because it shows the SEC is willing to revisit a serious penny stock bar when the applicant demonstrates compliance and a convincing forward-looking plan.

Singh represented that he intended to pursue Regulation D fundraising activity, would use experienced legal, accounting, and financial professionals to review the offerings, and would retain an independent compliance consultant. He also affirmed that he had complied with the penny stock bar, had no subsequent securities-related disciplinary record, and would continue to avoid paid promotional campaigns.

The order shows that the Commission can be persuaded in penny stock bar cases by a tailored, supervised plan designed to avoid the risk reflected in the original order.

Herring and Tafaro

Herring’s original 2021 matter arose from interference with a public company’s request-for-proposal process for selecting an independent auditor. The SEC found that Herring and others at EY compromised auditor independence and caused disclosure violations.

The sanctions included a denial of the privilege of appearing or practicing before the Commission as an accountant, with the right to seek reinstatement after three years, and a $50,000 civil penalty.

Tafaro’s original 2023 matter involved audits of two private funds in which the SEC found improper professional conduct and failures to perform required audit procedures relating to valuation risk. The order denied Tafaro the privilege of appearing or practicing before the Commission as an accountant, with the right to apply for reinstatement after one year.

Unlike the Herring order, the SEC order against Tafaro did not impose a separate personal civil penalty.

The April 2025 reinstatement orders for James G. Herring, Jr. and Sean P. Tafaro show that the Commission is actively processing these requests and granting them where the record supports reinstatement.

For accountants and other professionals, these reinstatement decisions reinforce a simple point: the post-order period matters. Compliance, restraint, and a clean professional record can do far more to support a reinstatement application than broad appeals to fairness.

Understanding the “Collateral Damage” of Penny Stock Bars

Penny stock bars are particularly reaching because they often trigger collateral disabilities. These can interfere with:

- Private placements and Regulation D offerings.

- Capital-raising plans and future issuer roles.

- Exempt financing activity.

The Singh matter suggests that if the requested activity is remote from the original misconduct and strong safeguards are in place, the SEC may be willing to narrow these real-world consequences.

Will the SEC Continue on This Path?

The key April 2025 orders were entered while Mark Uyeda was serving as Acting Chairman, just before Paul Atkins began his tenure as SEC Chairman. That means the recent shift took shape before the new chair was sworn in, but there is no public sign that the Commission has reversed course since then.

No one should assume that every application will be granted. The sample size is still limited, and outcomes remain highly fact-dependent. Even so, the current direction is hard to ignore. Relief from bars and related collateral restrictions now appears genuinely available where the record is strong and the investor-protection rationale is carefully developed.

Conclusion: How to Build a Strong Application

Relief is no longer just a theory, but it is also not routine. Successful applicants are those who present a disciplined proposal rather than a simple plea for mercy.

A winning strategy should include:

- A Limited Role: Propose a specific, restricted return to the market rather than unrestricted access.

- Enhanced Supervision: Connect the oversight directly to the risks of the original misconduct.

- Clean Record: Demonstrate full compliance with all prior sanctions and no subsequent violations.

- Investor Protection Narrative: Explain clearly why the proposed activity does not threaten market integrity.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at (561) 416-8956 or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com