Form 10 Shells occupy a unique niche in the U.S. capital markets. These corporations register a class of securities under the Securities Exchange Act of 1934 (“Exchange Act”) by filing Form 10.

Crucially, this registration occurs without a concurrent public offering under the Securities Act of 1933. While this process makes a company an SEC-reporting issuer, it does not raise new capital. For entrepreneurs, it is a “double-edged sword” providing transparency without automatically creating a public market or exchange listing.

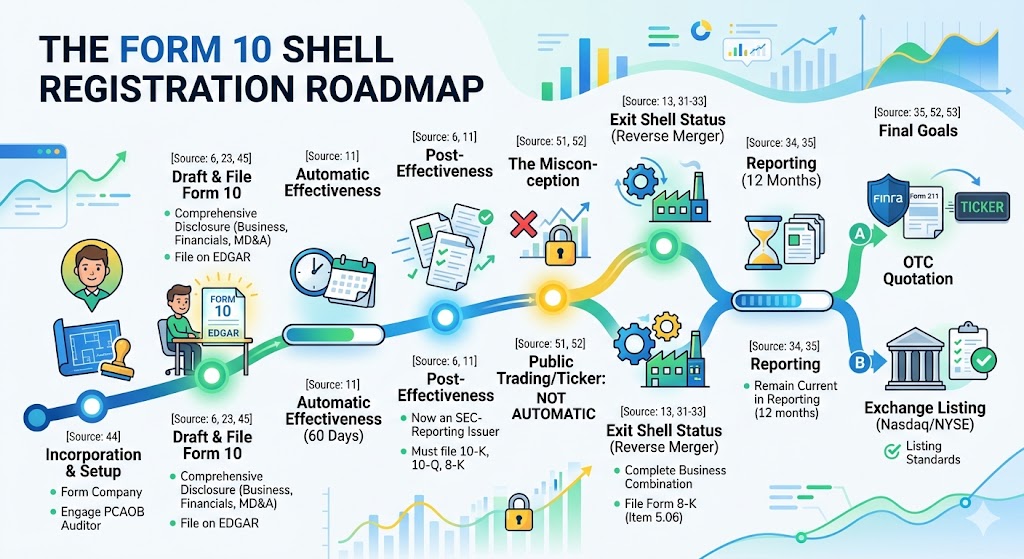

What is a Form 10 Shell?

A Form 10 Shell is defined as a company with:

- Operations: No or nominal operations

- Assets: No or nominal assets, other than cash and cash equivalents.

- Status: It becomes a reporting company by filing Form 10 under Section 12(g) of the Exchange Act.

Note: The filing registers a class of securities (usually common stock) to subject the company to SEC reporting requirements; it does not register securities for sale.

The Registration Process and Timeline

- Effectiveness: Registration typically becomes effective automatically 60 days after filing, unless the SEC accelerates or delays it.

- Immediate Obligations: Upon effectiveness, the issuer must comply with:

- Filing Form 10-K, 10-Q, and 8-K reports.

- Proxy and beneficial-ownership rules.

- Section 16 insider-reporting rules.

- SEC Review: The SEC frequently reviews shell registrations, often commenting on vague business plans, liquidity analysis, or incomplete related-party disclosures.

Strategic Reasons to File Form 10

Companies may choose this path to achieve several goals:

- Transparency: Building credibility through public reporting.

- Reverse Mergers: Preparing the entity for a future business combination.

- Compliance: Meeting requirements under Section 12(g).

- Future Growth: Establishing a reporting history to pave the way for future capital-raising or exchange listings.

Rule 144 and Resale Restrictions

Filing Form 10 does not make restricted securities freely tradable. Under Rule 144(i), shareholders cannot rely on Rule 144 for resales until the following “evergreen” requirements are met:

- The issuer ceases to be a shell and establishes real business operations.

- The issuer files “Form 10 information”.

- At least 12 months have passed since that filing, while the issuer remained current in its reporting.

Transitioning to an Operating Company

To officially exit “shell status,” a company must complete these steps:

- Complete a business combination or acquisition that establishes real operations..

- File a Form 8-K, Item 5.06 containing “Form 10 information”.

- Maintain current SEC reporting for at least 12 months thereafter.

Only after this transition can shareholders rely on Rule 144, and the company can pursue registered offerings or major listings.

Common Misconceptions: Trading and Liquidity

A major misconception is that filing Form 10 automatically results in public trading. It does not.

How Trading Actually Begins:

- OTC Markets: Shares cannot be quoted until a broker-dealer files Form 211 with FINRA. FINRA must then review the issuer’s information and assign a ticker symbol.

- Nasdaq or NYSE: To list on a national exchange, the company must meet strict quantitative (market cap, equity) and qualitative (governance) standards and have a listing application approved.

Risks and the “Clean Shell” Myth

- Regulatory Scrutiny: Form 10 Shells face compliance costs and potential liability under Section 18 and Rule 10b-5.

- The “Clean Shell” Myth: There is no such thing as a “clean” shell based solely on inactivity. Status depends on valid formation, audited financials, and transparent disclosure of all promoters and control persons.

- Form 10 vs. Reverse-Merger Shells: Form 10 Shells are often considered “cleaner” than abandoned public shells because they have clear audit histories and lack the legacy liabilities typical of older entities.

Steps to a Compliant Filing

- Incorporate the entity.

- Engage a PCAOB-registered auditor.

- Prepare comprehensive disclosure (business description, risk factors, MD&A, audited financials)

- File Form 10 on EDGAR.

- Respond to SEC comments and maintain current filings.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com