When a private company decides to go public, it faces several potential pathways—each differing in structure, cost, timing, dilution, and control. This comprehensive guide explains and compares the four primary methods: Initial Public Offering (IPO), Direct Public Offering (DPO), Reverse Merger, and Regulation A+ (“Mini-IPO”). The discussion includes regulatory structure, procedural steps, financial impact, and strategic considerations for issuers seeking access to U.S. capital markets.

Overview of the Public Market Pathways

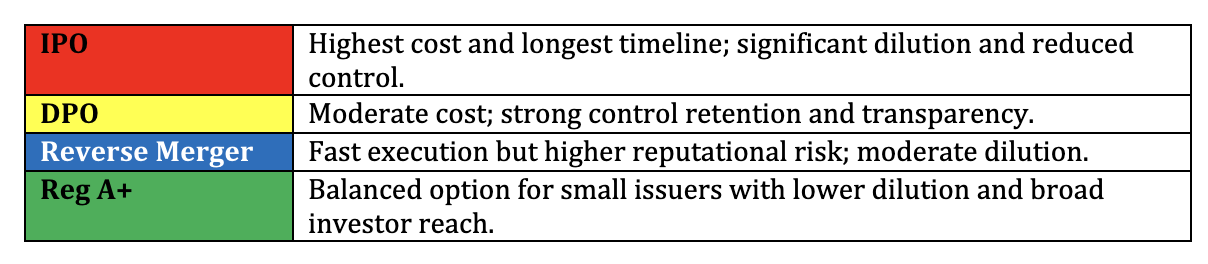

The decision to go public should align with the company’s maturity, capital needs, governance readiness, and tolerance for regulatory oversight. The chart below provides a high-level summary of the four primary routes to becoming a public company.

- IPO: Full SEC registration and underwritten offering for exchange listing.

- DPO: Self-underwritten SEC registration without underwriter commissions.

- Reverse Merger: Acquisition of a public shell followed by Exchange Act registration.

- Regulation A+: Exempt “Mini-IPO” under the JOBS Act, allowing broad investor participation.

Initial Public Offering (IPO)

An IPO involves registering securities on Form S-1 under the Securities Act and engaging one or more underwriters to sell shares to investors. The process begins with due diligence and audits, followed by SEC review and a marketing roadshow. Once declared effective, the shares are listed on a national exchange such as the Nasdaq or the NYSE.

IPOs provide access to institutional investors and can dramatically enhance valuation, but they are also the most expensive and time-consuming route to the public markets.

Structure and Process

- Engage underwriters and securities counsel.

- Prepare audited financial statements under PCAOB standards.

- Draft Form S-1 with detailed disclosures under Regulation S-K.

- Undergo SEC comment review and revise until effectiveness.

- Conduct investor roadshow and pricing. 6. Complete exchange listing and begin trading.

Costs and Timing

- Total cost: $2–5 million.

- Typical timeline: 6–12 months.

- Underwriter commission: 5–7% of gross proceeds.

- Exchange listing and legal fees: $150K–$300K.

Advantages

- Maximum capital access.

- Institutional investor participation.

- Enhanced liquidity and credibility.

- Uplift in brand visibility and analyst coverage.

Disadvantages

- High costs and extensive regulatory burden.

- Potential loss of founder control.

- Market volatility risk during the SEC review.

- Ongoing quarterly reporting obligations.

Direct Public Offering (DPO)

A Direct Public Offering is a self-underwritten registered offering in which the issuer sells shares directly to investors. The company files Form S-1 with the SEC, secures effectiveness, and may later obtain a ticker symbol through FINRA Form 211 for OTC quotation. DPOs are less costly and allow management to retain control over pricing, allocation, and communications.

Key Features

- No underwriter commissions.

- Management-driven marketing.

- Can be followed by OTC or exchange listing.

- Requires a sponsoring market maker for public quotation.

Costs, Timing, and Control

- Cost: $300K–$800K.

- Timing: 3–6 months.

- Control: Full management control with lower dilution (10–20%).

Reverse Merger

In a reverse merger, a private company acquires a public shell company and assumes its reporting status. The private company’s shareholders exchange their shares for a controlling interest in the public entity. This route offers speed and reduced upfront costs but carries regulatory and reputational risks.

Process and Legal Mechanics

- Identify and conduct due diligence on a clean public shell.

- Negotiate a merger agreement and share exchange.

- File Super 8-K with Form 10-level disclosure within four days.

- Request FINRA corporate actions (name, symbol, and CUSIP changes).

Risks and SEC Scrutiny

Reverse mergers attract high SEC oversight due to prior abuse of shell structures. Issuers must ensure audited financials, clean corporate histories, and full post-merger disclosure.

Regulation A+ (“Mini-IPO”)

Regulation A+, created under the JOBS Act, allows companies to raise up to $75 million from both accredited and non-accredited investors. Offerings are qualified by the SEC on Form 1-A and are divided into Tier 1 and Tier 2 levels.

- Tier 1: Up to $20 million; subject to state review.

- Tier 2: Up to $75 million; pre-empted from Blue Sky laws under NSMIA.

Advantages and Limitations

- Lower costs and regulatory burden than a full IPO.

- Broad investor access.

- Can be marketed online (“testing the waters”).

- Tier 2 requires ongoing reporting (Forms 1-K, 1-SA, 1-U).

Comparative Analysis: Cost, Timing, Dilution, and Control

The table below summarizes the practical distinctions among the four going-public methods, considering costs, regulatory review, dilution, and founder control.

Strategic Considerations

Choosing the right pathway requires aligning the company’s size, funding goals, investor profile, and governance readiness. Early-stage companies often prefer DPOs or Reg A+ offerings, while established issuers seeking institutional participation gravitate toward IPOs.

Reverse mergers remain suitable for acquisition-driven issuers needing rapid access to public status, provided the shell is fully compliant.

Compliance and Post-Going-Public Obligations

Regardless of the method chosen, issuers must comply with SEC reporting requirements under the Exchange Act, maintain DTC eligibility, and ensure accurate and timely filings. Required filings include Form 10-K, Form 10-Q, Form 8-K, and beneficial ownership filings on Forms 3, 4, and 5. Tier 2 Reg A+ issuers must also file Forms 1-K and 1-SA annually and semiannually.

Illustrative Case Studies

- IPO Example: Technology company raised $100M, 30% dilution, 10-month timeline.

- DPO Example: Regional bank raised $12M, 15% dilution, 4-month timeline.

- Reverse Merger Example: Renewable energy firm completed merger, $400K cost, 8-week closing.

- Reg A+ Example: Consumer brand raised $30M, 12% dilution, and later uplisted to Nasdaq.

Common Pitfalls and Best Practices

- Using non-PCAOB auditors or incomplete audits.

- Inadequate disclosure or promotional activity during the quiet period.

- Acquiring shells with hidden liabilities.

- Failing to maintain current public information for Form 211 approval.

- Ignoring governance and internal control readiness.

Best practices include early engagement of experienced securities counsel, maintaining meticulous records, and adopting comprehensive disclosure controls and procedures.

Conclusion

Each path to the public markets—IPO, DPO, Reverse Merger, and Regulation A+—offers distinct advantages depending on company objectives. IPOs provide scale and liquidity but require greater cost and control sacrifice. DPOs and Reg A+ offerings deliver flexibility and founder autonomy. Reverse mergers offer speed but necessitate heightened due diligence.

The optimal strategy balances capital requirements, control retention, market perception, and regulatory readiness. With careful planning and guidance from experienced counsel, any of these pathways can effectively position a company for growth and investor confidence in the public markets.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com