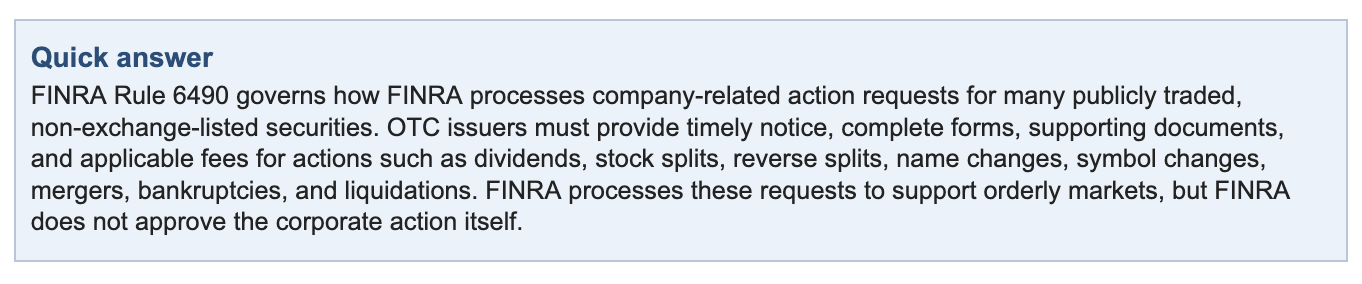

Why Rule 6490 Matters

FINRA Rule 6490 is one of the most important rules for public companies whose securities trade over the counter rather than on a national securities exchange. The rule addresses how FINRA processes company-related actions for OTC securities, including stock splits, dividends, name changes, symbol changes, mergers, acquisitions, bankruptcies, liquidations, and similar events.

Corporate actions can directly affect the way shares are quoted, held, transferred, settled, and displayed in brokerage accounts. For an issuer, a corporate action may be part of a legitimate growth strategy, recapitalization, rebranding, acquisition plan, or restructuring. For shareholders, the same event may change the number of shares owned, the trading symbol used to identify the security, the timing of a dividend, or the practical liquidity of the investment.

Because OTC securities often involve smaller issuers, less analyst coverage, lower liquidity, and less widely distributed public information than exchange-listed securities, accurate and timely processing is critical. A poorly planned corporate action can create confusion for brokers, transfer agents, market makers, clearance firms, investors, and the issuer itself.

What Is FINRA Rule 6490?

FINRA Rule 6490, titled “Processing of Company-Related Actions,” establishes the framework FINRA uses to review and process documentation for corporate-action announcements involving certain non-exchange-listed securities. The rule became effective on September 27, 2010, and FINRA has amended it since then, including an amendment reflected on FINRA’s rule page as effective October 7, 2025.

The rule works alongside Exchange Act Rule 10b-17, which requires issuers of publicly traded securities to provide advance notice of certain record-date-related events. In practice, Rule 6490 is the operational pathway that allows FINRA to receive, review, and process information about covered OTC corporate actions before the information is reflected in market systems.

Rule 6490 does not make FINRA the corporate-law decision maker for the issuer. The company remains responsible for making sure its board approvals, shareholder approvals, charter filings, state-law requirements, SEC reporting, transfer-agent instructions, and public disclosures are complete and lawful. FINRA’s role is to process the documentation related to the market announcement and, where the rule permits, to decline processing if the request is deficient.

Corporate Actions Covered by Rule 6490

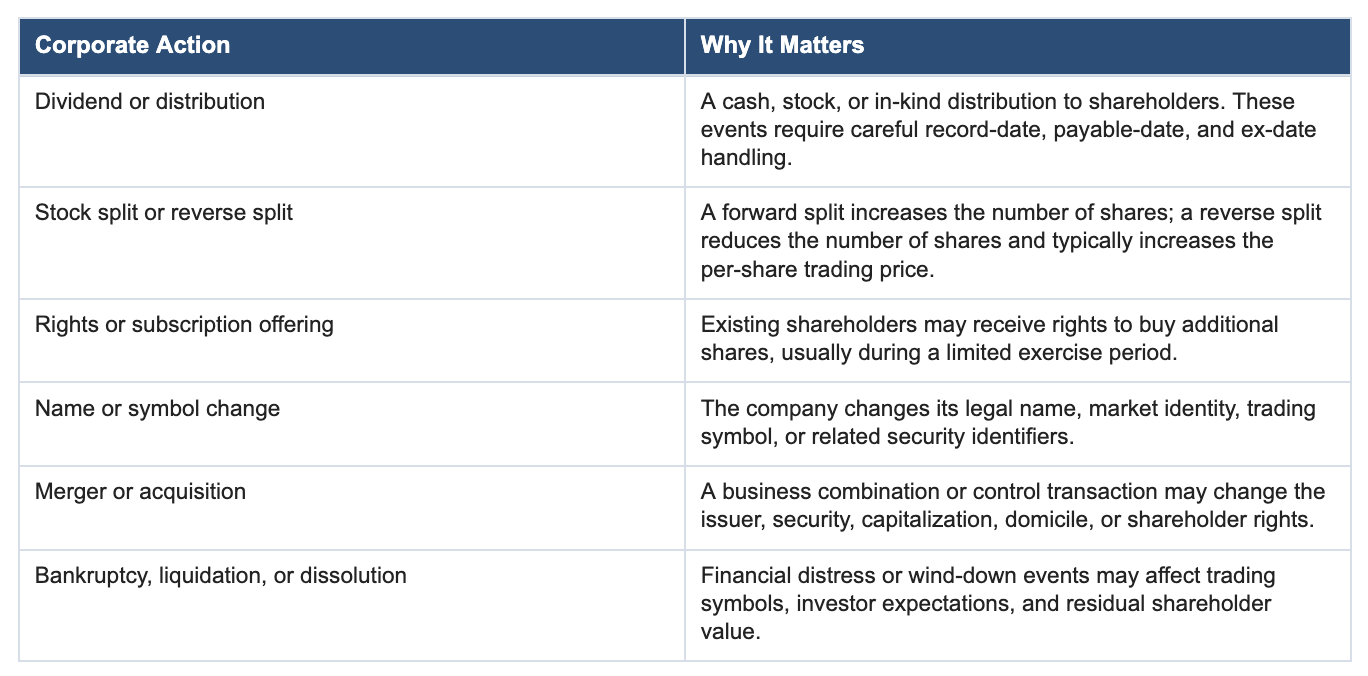

FINRA Rule 6490 applies to two broad categories of company-related actions: actions covered by Exchange Act Rule 10b-17 and other company-related actions that affect OTC securities. Common examples include the following:

Why Corporate Actions Matter to Investors

FINRA’s investor guidance emphasizes that corporate actions may range from routine events, such as a dividend payout, to major events, such as a merger, restructuring, bankruptcy, or liquidation. Even actions that do not make headlines can matter. A trading-symbol change can affect how an investor searches for a security. A stock split can change the number of shares in an account. A reverse stock split can change both the visible share count and the trading price per share.

Investors should pay close attention to OTC corporate actions because the practical impact may not be obvious from a press release alone. For example, a company may announce a new name to reflect a changed business plan, but investors still need to know when the name change will be processed, whether a new CUSIP number is involved, and whether brokerage systems will reflect the change without delay. Similarly, a dividend announcement requires investors to understand record dates, payment dates, and ex-dates.

In liquidation or bankruptcy scenarios, the stakes may be even higher. Common shareholders are typically behind secured creditors and bondholders in the payment priority stack. A company’s securities may continue trading in the OTC market after a bankruptcy filing, but continued trading does not mean common shareholders will ultimately receive value.

FINRA’s Role: Processing, Not Approval

A key point for both issuers and investors is that FINRA does not approve corporate actions. FINRA processes corporate-action announcement requests for eligible OTC securities so that the market receives information needed for quotation, settlement, transfer, and investor-awareness purposes.

This distinction is important because some issuers have historically used press releases, website updates, or social-media posts in ways that could imply FINRA has approved a corporate action. That wording can be misleading. FINRA’s processing function is not a fairness opinion, not a legal opinion, not a confirmation that the action complies with every applicable law, and not an investment endorsement.

The Rule 6490 Notice Deadline

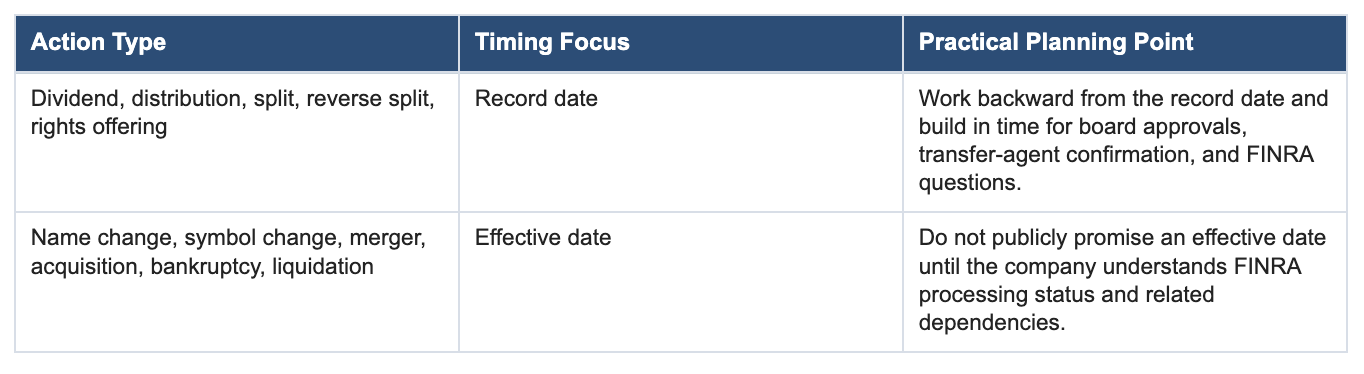

Timing is one of the most common Rule 6490 compliance issues. For actions covered by Exchange Act Rule 10b-17, issuers generally must provide notice to FINRA at least 10 days before the record date. These actions include dividends, distributions, stock splits, reverse splits, rights offerings, and other subscription offerings.

For other company-related actions, such as name changes, trading-symbol changes, mergers, acquisitions, bankruptcies, liquidations, and similar events, Rule 6490 requires a complete submission no later than 10 calendar days before the proposed effective date of the action. A submission that is not complete, properly submitted, and timely may be treated as late and may trigger additional fees or processing delays.

What FINRA Reviews Under Rule 6490

Rule 6490 gives FINRA authority to request additional information or documentation needed to review a submission and verify the accuracy of the information provided. The review is not merely a clerical check. FINRA may ask for backup materials and may determine that a request is deficient if the rule-based grounds are present.

A Rule 6490 package may require different documents depending on the action. Typical materials may include board resolutions, shareholder approvals, charter amendments, state merger filings, transfer-agent verification, CUSIP information, capitalization details, proof of payment, and public disclosure materials. The documents should tell one consistent story. If the board resolution says one thing, the state filing says another, and the FINRA form says a third, processing problems should be expected.

FINRA may also treat a request as lapsed if the requesting party does not sufficiently respond to requests for additional information within the period provided by the rule. In practical terms, issuers should treat FINRA comments as time-sensitive and should centralize responsibility for responses with counsel or another qualified coordinator.

When FINRA May Refuse to Process a Corporate Action

Rule 6490 permits FINRA to determine that a corporate-action request is deficient and should not be processed where non-processing is necessary to protect investors, the public interest, and fair and orderly markets. The rule identifies specific categories of concern, including incomplete or inaccurate documentation, lack of proper authority, reporting-status problems, regulatory or legal proceedings involving relevant parties, information suggesting possible securities-market fraud, and significant uncertainty in settlement or clearance.

- Incomplete documents: Forms, exhibits, approvals, or supporting materials do not match or do not provide enough information.

- Reporting concerns: The issuer is not current in required reporting, where applicable.

- Regulatory or legal issues: Relevant parties are involved in certain regulatory, civil, or criminal matters.

- Fraud-risk indicators: FINRA has information suggesting potentially fraudulent activity related to the securities markets.

- Clearance and settlement uncertainty: The market infrastructure cannot reliably process the security or action.

If FINRA makes a deficiency determination, the issuer or requesting party may have appeal rights, but an appeal does not mean the corporate action will proceed on the issuer’s preferred timeline. The better approach is to reduce deficiency risk before filing.

Fees, Late Fees, and Appeals

Rule 6490 includes non-refundable processing fees and late fees. As reflected in FINRA’s current rule text, timely Exchange Act Rule 10b-17 notifications carry a $200 fee. Late notifications are subject to higher fees depending on how close the filing is to the corporate-action date, including $1,000, $2,000, or $5,000 categories. Voluntary symbol-change requests carry a $500 fee, while initial symbol setup and symbol deletion are listed as no charge. FINRA also lists a $4,000 action-determination appeal fee.

These fees should not be viewed as the only cost of a late or deficient filing. A missed deadline can delay the market announcement, create investor-relations problems, complicate settlement, and force the company to revise a public timeline. For OTC issuers, reputational damage from a failed or delayed corporate action can be more costly than the fee itself.

FINRA Gateway and Electronic Corporate-Action Workflows

FINRA has moved many regulatory and compliance workflows into electronic systems. FINRA describes FINRA Gateway as an integrated platform for managing regulatory and compliance obligations, including filings, reports, requests for information, document requests, and support tickets. For issuers and professionals working on corporate actions, this shift reinforces the need to manage Rule 6490 as a documented workflow rather than a paper exercise.

A practical Rule 6490 workflow should include early login and entitlement planning, clear document ownership, version control, transfer-agent coordination, proof-of-payment tracking, and a process for responding to FINRA comments. The company should also keep a complete internal record of what was submitted, when it was submitted, who approved it, and how any comments were resolved.

Because platform access, entitlements, and submission mechanics can change, issuers should confirm the current FINRA submission procedure before announcing a corporate-action timeline. The legal deadline is only one part of the process; the company also needs practical readiness to submit a complete package through the applicable FINRA system.

Rule 6490 Compliance Checklist for OTC Issuers

- Identify the action. Determine whether the event is a Rule 10b-17 action, another company-related action, or both.

- Confirm the deadline. Use the record date for dividends, distributions, splits, reverse splits, and rights offerings; use the effective date for other company-related actions.

- Gather authority documents. Collect board approvals, shareholder approvals, charter amendments, merger filings, or other authorizing materials.

- Coordinate with the transfer agent. Confirm share counts, CUSIP needs, distribution mechanics, and any required transfer-agent verification.

- Check reporting status. Confirm whether the issuer is current in required SEC, OTC, or other regulatory reporting.

- Prepare consistent disclosures. Make sure press releases, Form 8-Ks or other filings, website updates, and FINRA forms align.

- Budget fees and late-fee risk. Pay applicable fees and avoid timelines that create unnecessary late-fee exposure.

- Respond quickly to FINRA. Centralize comment responses and keep a complete response record.

- Monitor public market updates. Watch FINRA’s Daily List and coordinate with brokers, investors, and market data vendors as needed.

Common Mistakes That Delay OTC Corporate Actions

- Starting too late: The 10-day notice period should be treated as a minimum legal threshold, not as a project plan.

- Assuming FINRA approval: FINRA processing is not approval of the action or endorsement of the company.

- Submitting inconsistent documents: Small discrepancies in dates, ratios, names, authorized shares, or capitalization can cause questions.

- Ignoring CUSIP and transfer mechanics: A new name, symbol, split, or merger may require new identifiers and updated transfer-agent records.

- Announcing dates prematurely: A public effective-date promise can create confusion if FINRA requests additional information.

- Overlooking public-company reporting: Reporting-status problems may become part of a deficiency review.

Investor Takeaways: How to Track OTC Corporate Actions

Investors in OTC securities should not rely solely on promotional announcements or social-media posts. FINRA’s Daily List is an important resource for OTC corporate-action announcements, including ex-dates, new issues, deleted issues, deletions, name changes, symbol changes, updates, and cancellations. Brokerage statements may eventually reflect the event, but investors should understand the timing and implications before assuming the account display tells the full story.

Investors should also be cautious about issuer language suggesting that FINRA has approved a transaction. FINRA’s role is to process corporate-action announcements for certain OTC securities, not to approve the company’s business decision or verify that the action is fair to shareholders.

What is FINRA Rule 6490?

FINRA Rule 6490 is the rule that governs FINRA’s processing of documentation for certain company-related actions involving publicly traded, non-exchange-listed securities. It covers actions such as dividends, stock splits, reverse splits, rights offerings, name changes, symbol changes, mergers, bankruptcies, and liquidations.

Does FINRA approve corporate actions?

No. FINRA processes corporate-action announcement requests for eligible OTC securities. FINRA does not approve the issuer’s business decision, does not provide a legal opinion, and does not determine that the action is fair or advisable for investors.

How much advance notice is required?

For Rule 10b-17 actions, issuers generally must provide notice at least 10 days before the record date. For other company-related actions under Rule 6490, a complete submission generally must be made at least 10 calendar days before the proposed effective date.

What happens if a Rule 6490 filing is late?

A late submission may trigger additional fees and processing delays. It may also interfere with an announced timeline and create issues for shareholders, transfer agents, brokers, and market data systems.

Can FINRA refuse to process a corporate action?

Yes. FINRA may issue a deficiency determination and refuse processing when the rule-based grounds are present and non-processing is necessary to protect investors, the public interest, and fair and orderly markets.

Why do reverse stock splits receive close attention?

Reverse splits can significantly affect share count, price presentation, and investor perception. They may also involve new CUSIP numbers, amendments to charter documents, and detailed transfer-agent coordination.

Conclusion

FINRA Rule 6490 is not just an administrative filing rule. It is a critical part of the OTC market infrastructure that connects issuer corporate decisions to market-facing announcements, brokerage account processing, settlement systems, and investor awareness. For OTC issuers, the safest approach is to plan early, assemble consistent documents, coordinate with the transfer agent, confirm platform access, avoid misleading language about FINRA approval, and respond promptly to any FINRA questions.

For investors, the key lesson is equally practical: a corporate action can materially affect an OTC security even when the event does not receive broad media coverage. Investors should review issuer disclosures, monitor the FINRA Daily List, understand the difference between processing and approval, and be cautious when corporate-action announcements are used as promotional signals rather than clear market information.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com