Marketing an initial public offering is not the same as marketing an ordinary product launch. In a U.S.-registered IPO, every communication about the offering must be carefully coordinated because the Securities Act of 1933 strictly regulates offers, sales, publicity, investor outreach, and written materials.

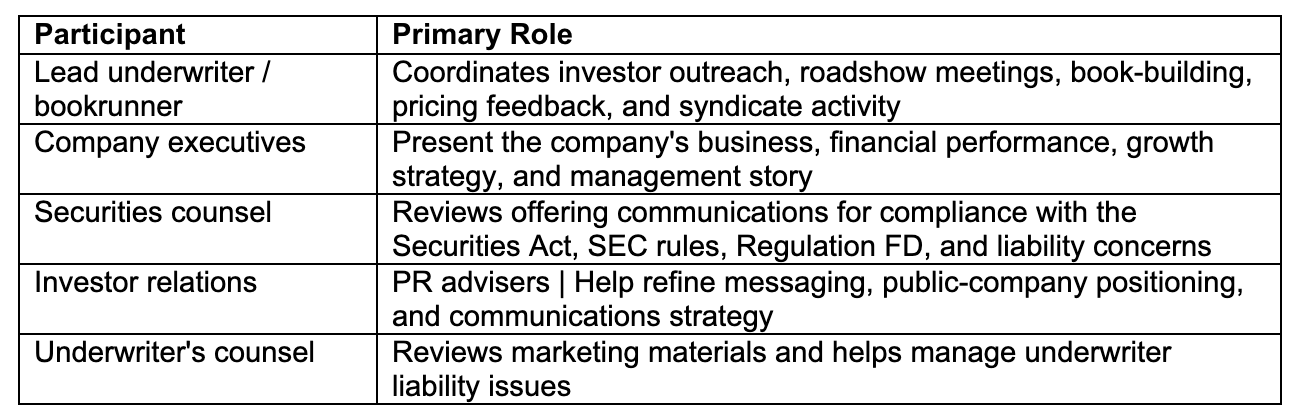

In practice, IPO marketing is usually led by the managing underwriter or lead bookrunner, with participation from company management, investor relations professionals, public relations advisers, and securities counsel. But while bankers may drive the roadshow and investor outreach process, lawyers play a critical role in determining what can be said, when it can be said, and to whom.

IPO Marketing Is a Regulated Process

A company going public cannot simply launch a broad promotional campaign encouraging investors to buy its securities. U.S. securities laws are designed to ensure that investors receive offering information through the registration statement and prospectus, rather than through hype, selective disclosure, or unsupported promotional claims.

This is why IPO marketing is typically controlled through a structured process involving:

The key point is simple: IPO marketing is not free-form advertising. It is a legally supervised securities offering process.

The Default Rule: Silence Is Safer Than You Think

Before getting to the safe harbors that make the process workable, it helps to understand the default. From the moment a company starts seriously preparing for an IPO until the SEC declares the registration statement effective, the company is “in registration” — and the gun-jumping rules apply.

Section 5(c) of the Securities Act generally prohibits any offer to sell a security before a registration statement is filed. After filing but before effectiveness, Section 5(b)(1) restricts written offers to those made through a statutory prospectus that meets the requirements of Section 10. The SEC reads “offer” broadly, sweeping in not just price-and-availability statements but also communications that condition the market by hyping the company, its industry, or its prospects. A CEO interview that drops at the wrong moment, a press release with a little too much swagger, a tweet from a director — any of these can become an exhibit in an SEC comment letter.

Cross that perimeter and the SEC may treat the offending communication as an unlawful offer — an event commonly called gun-jumping — which can delay the deal, force a cooling-off period, or, in serious cases, give buyers a rescission right against the issuer.

The good news is that the rulebook also carves out a series of safe harbors that let an issuer communicate sensibly throughout the process. Two of the most important for IPO marketing are Rule 134 and Rule 163B.

Rule 134: The Permitted “Tombstone-Plus”

Rule 134 is the workhorse safe harbor for offering communications after a registration statement has been filed. It provides that certain limited written communications relating to a registered offering are not deemed to be a “prospectus” for purposes of Section 5(b)(1). In plain terms: if a communication stays within the four corners of Rule 134, the company can put it out without violating the written-offer restrictions.

A few features are worth understanding.

1) It’s only available once a Section 10 prospectus is on file.

Rule 134 does not unlock at the moment the company decides to go public. It requires a publicly filed registration statement containing a preliminary prospectus that satisfies Section 10. A confidential draft submission — common today for emerging growth companies and other issuers using the JOBS Act’s confidential-review process — is not a filing for these purposes. The safe harbor only opens once the registration statement hits EDGAR.

2) The permitted content is enumerated, not open-ended.

Rule 134 reads like a checklist. Among other things, a compliant communication can include:

- The legal identity and business address of the issuer, plus a brief description of the general nature of its business

- The title, amount, and basic terms of the securities being offered

- The proposed offering schedule and a description of marketing events, including road shows

- The names of the underwriters and their roles in the syndicate

- Procedures by which prospective investors can submit indications of interest, including how to request a preliminary prospectus

- For an IPO, the anticipated price range — but only once a prospectus containing that range has been filed

The list is broader than the old “tombstone ad” most people picture, but it is still a list. Anything outside it — projections, qualitative claims about market position, comparisons to peers, anything that smells like salesmanship — is not protected by Rule 134.

3) Required legends and accompanying prospectus rules apply.

Depending on what the communication contains, Rule 134 may require legends pointing recipients to the preliminary prospectus, and certain content (like a request for indications of interest) is only permitted if a Section 10 prospectus accompanies or precedes the communication. The drafting is precise, and the legend requirements are easy to overlook.

In practice, Rule 134 is what lets an issuer issue a launch press release, post the deal on its investor-relations site, and distribute a basic announcement to the wire services without those communications being treated as a prospectus.

Rule 163B: Testing the Waters Before You Dive In

Rule 134 governs what the *market at large* can see. Rule 163B governs a very different kind of conversation: the private, targeted dialogue with sophisticated institutions that helps a company decide whether — and on what terms — to come to market in the first place.

Adopted by the SEC in 2019, Rule 163B extended a JOBS Act privilege previously available only to emerging growth companies and made “testing-the-waters” communications available to every issuer. The rule allows an issuer, or any person authorized to act on its behalf (including underwriters), to engage in oral or written communications with potential investors before or after filing a registration statement, for the purpose of gauging interest in a contemplated registered offering.

The flexibility is meaningful, but the conditions are strict.

1) The audience is limited to QIBs and IAIs.

Communications under Rule 163B may be directed only to qualified institutional buyers, as defined in Rule 144A, and institutional accredited investors, as defined in Regulation D. The issuer must reasonably believe the recipients meet those standards. The SEC declined to prescribe a specific verification method, expecting issuers to use the same approaches they already rely on for Rule 144A and Regulation D offerings. Retail investors are off the table.

2) The communications are still “offers.

Rule 163B exempts these communications from Sections 5(b)(1) and 5(c), but it does not exempt them from the anti-fraud provisions of the federal securities laws. Material misstatements or omissions in a test-the-waters deck can support liability under Section 12(a)(2) and Rule 10b-5. The corollary is that the content of a Rule 163B communication should not conflict with material information in the registration statement when it is ultimately filed. Internal review, version control, and consistency with the draft S-1 are essential.

3) No filing requirement, but expect the staff to ask.

Test-the-waters materials are not free writing prospectuses, and Rule 163B imposes no obligation to file them with the SEC. That said, the SEC staff routinely requests TTW materials during the registration-statement review, particularly for IPOs. Teams should assume the materials will be read by regulators and draft accordingly.

4) Coordination with Regulation FD.

For issuers already reporting under the Exchange Act, Regulation FD remains a live consideration. Selective disclosure of material nonpublic information to QIBs and IAIs in a TTW context can implicate FD unless an exception applies. This usually means working with FD-style protections — confidentiality agreements, careful scoping of the information shared, or other safeguards.

When used well, Rule 163B lets an issuer have honest conversations with anchor investors before committing to a public filing, refine the deal’s positioning, and reduce the execution risk of a launch that the market simply isn’t ready for.

How the Two Rules Fit Together

It’s tempting to think of Rule 134 and Rule 163B as alternatives. They aren’t. They occupy different lanes and frequently operate in parallel.

Rule 163B governs *private, pre-launch dialogue with institutional investors*. It is available before and after the registration statement is filed and is invisible to the public.

Rule 134 governs *public, post-filing communications* about the offering itself. It opens only once the registration statement is on file and is designed for broad dissemination.

A typical IPO uses both. The company and its underwriters may rely on Rule 163B during the months leading up to filing to gauge demand from anchor accounts. Once the registration statement is publicly filed, the company can rely on Rule 134 for its launch press release, the basic deal page on its IR site, and the standard syndicate communications. Throughout, the team continues to police the perimeter — making sure that interviews, social posts, conference appearances, and ordinary-course business communications don’t drift into the territory that the safe harbors don’t cover.

Practical Takeaways for Issuers and Deal Teams

A few principles tend to keep IPO communications out of trouble:

1) Treat “in registration” as a state of mind.

Every public-facing communication, from a recruiting post to a customer webinar, deserves a second look once the IPO is on the calendar. The safe harbors are narrow; ordinary corporate communications safe harbors (Rules 168 and 169) help, but they have their own conditions.

2) Use Rule 163B intentionally, not casually.

Pick the audience deliberately, document QIB/IAI status, control the materials, and make sure what you tell investors is consistent with what will appear in the prospectus.

3) Don’t improvise Rule 134 communications.

The rule reads like a checklist because it *is* a checklist. Build templates with counsel, and resist the temptation to add color.

4) Loop in the underwriters and counsel early on press strategy.

Launch press releases, road-show announcements, and any media engagement should be planned with the deal team, not sprung on them.

5) Assume the SEC will read everything.

TTW decks, press materials, social posts — the staff routinely asks for them during review. Draft as if they will be Exhibit A.

The communications rules are not designed to silence issuers. They are designed to ensure that the prospectus, with its liability framework and its required disclosures, remains the central document on which investors rely. Used well, Rules 134 and 163B give a company room to run a credible marketing process without putting the offering at risk.

This securities law blog post is provided as a general informational service. If you have any questions about this article, Hamilton & Associates Law Group, P.A. is ready to help.

Since 1998, our Founder, Brenda Hamilton, has been a leading voice in corporate and securities law, representing both domestic and international clients across diverse industries and jurisdictions.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com