As summer peaked at the end of July, Meta Materials (MMAT) popped back into the news. What had happened? The company filed a Form 8-K explaining that MMAT, its CEO George Palikaras. and John Brda, the former CEO of Torchlight Energy Resources, the company with which Meta had merged in order to list quickly on the Nasdaq Stock Market, had received Wells notices from the Securities and Exchange Commission.

Wells notices are not good news. The SEC explains them as part of what it calls the “Wells process”:

A Wells notice is a communication from the staff to a person involved in an investigation that: (1) informs the person the staff has made a preliminary determination to recommend that the Commission file an action or institute a proceeding against them; (2) identifies the securities law violations that the staff has preliminarily determined to include in the recommendation; and (3) provides notice that the person may make a submission to the Division and the Commission concerning the proposed recommendation.

Companies and individuals are not required to announce receipt of a Wells notice to shareholders or to the general public, but MMAT chose to do so. Neither are they required to reply making their case to the Commission, but if they wish to, they should make their confidential submissions within the time limit—usually about two weeks—set by the investigators in the notice, or in a subsequent communication. Submissions should not be longer than about 40 pages, and if they are deficient in ways explained in the SEC’s Enforcement Manual, they will be rejected.

A Wells Notice may be a target’s first inkling that he’s under investigation, or he may have had prior contact with Enforcement staff. If the target(s) decide to make a Wells submission, they’d do well to remember what they send will not be privileged and can be used against them. They should, in any case, bear in mind that most Wells notices result in litigation by the Commission against the targets. Research from 10 years ago put the number at about 80 percent.

While it isn’t known exactly why the agency has been investigating MMAT, Palikaros, and Brda, the company offers some information in its 8-K, noting that it has to do with:

… a previously disclosed SEC investigation (the “Investigation”) into, among other things, the merger involving Torchlight Energy Resources, Inc. and Metamaterial Inc. The Wells Notices each state that the SEC staff has made a preliminary determination to recommend that the SEC file a civil enforcement action against the recipients alleging violations of certain provisions of the U.S. federal securities laws. Specifically, the Wells Notice received by the Company states that the proposed action would allege violations of Section 17(a) of the Securities Act; Sections 10(b), 13(a), 13(b)(2)(A), 13(b)(2)(B) and 14(a) of the Exchange Act of 1934 and Rules 10b-5 and 14a-9 thereunder; and Regulation FD.

Section 17(a) of the Securities Act of 1933 makes it unlawful to “employ any device, scheme, or artifice to defraud”, “obtain money or property” by using material misstatements or omissions, or to “engage in any transaction, practice, or course of business which operates or would operate as a fraud or deceit upon the purchaser.”

15 U.S.C. § 78j(b) makes it unlawful “To use or employ, in connection with the purchase or sale of any security registered on a national securities exchange or any security not so registered, or any securities-based swap agreement [1] any manipulative or deceptive device or contrivance in contravention of such rules and regulations as the Commission may prescribe as necessary or appropriate in the public interest or for the protection of investors. The sections of the Exchange Act cited address similar issues. Regulation FD treats questions of full, adequate, and “not misleading” disclosures.

We know what the previously disclosed investigation was, thanks to the company’s earlier filings:

In September 2021, we received a subpoena from the Securities and Exchange Commission, Division of Enforcement, in a matter captioned In the Matter of Torchlight Energy Resources, Inc. The subpoena requests that we produce certain documents and information related to, among other things, the merger involving Torchlight Energy Resources, Inc. and Metamaterial Inc. We are cooperating and intend to continue to cooperate with the SEC’s investigation. We can offer no assurances as to the outcome of this investigation or its potential effect, if any, on us or our results of operation.

Meta Materials, Torchlight Energy Resources, and MMTLP

What is known is that MMAT resolved to move to a U.S. exchange in 2020, though it attracted little interest from anyone but the SEC Enforcement staff until a year or so later. Meta is a Canadian company located in Nova Scotia but is now incorporated in Nevada. Originally called Metamaterial Technologies Inc., in 2020, it changed its name to Metamaterial Inc (META), did a reverse triangular merger with Continental Precious Minerals Inc., and began trading on the Canadian Securities Exchange. Ten months later, it signed a definitive agreement for a business combination with Torchlight Energy (TRCH), a Plano, Texas, oil and gas exploration company listed on the Nasdaq. Torchlight shareholders, including CEO John Brda, would be given a stake in the new company, Meta Materials. MMAT, which describes itself as a disruptive company that invents, designs, develops, and manufactures scalable, sustainable, highly functional materials and intelligent surfaces, had no interest in getting into the oil business, and so Torchlight’s assets would be sold off:

Upon completion of the Transaction, shareholders of Metamaterial are expected to hold an approximate 75% equity interest in the combined company while Torchlight shareholders will retain an approximate 25% equity interest in the combined company, subject to the pre-closing financing described below.

Torchlight shareholders on the record date will be entitled to receive a preferred stock dividend, payable immediately prior to the closing of the Transaction, that entitles them to their pro rata share of any proceeds resulting from any sale of Torchlight’s oil and gas assets that occurs on the earlier of December 31, 2021 or six months from the closing of the Transaction, and, after such time if such sales are not complete, will be entitled to receive a pro rata equity interest in a spin-off entity that holds Torchlight’s remaining oil and gas assets, subject to certain conditions.

But that wasn’t all: Torchlight would also extend two bridge loans in the amount of $500,000 each in exchange for convertible promissory notes, though “[u]pon closing, these two bridge loans, including the aggregate principal and unpaid interest, are to be included in, and credited against, the $10 million pre-closing financing described above, with such notes to be deemed cancelled and paid in full.”

On June 29, 2021, Meta announced that the Series A preferred dividend had been distributed to shareholders of record of TRCH on June 25 (the record date had been June 24). DTC informed Meta that the preferred shares should be formally allocated to individual accounts on or about June 30. Canadian shareholders might experience a delay of a few days. On the day before, June 28, Meta had begun trading on the Nasdaq. The event was proudly announced by Meta’s founding president and CEO, George Palikaros. Brda, the former TRCH CEO, would stay on as an adviser to Meta to manage the disposal of the company’s oil and gas assets.

Torchlight shareholders received 164,923,363 shares of the Series A preferred.

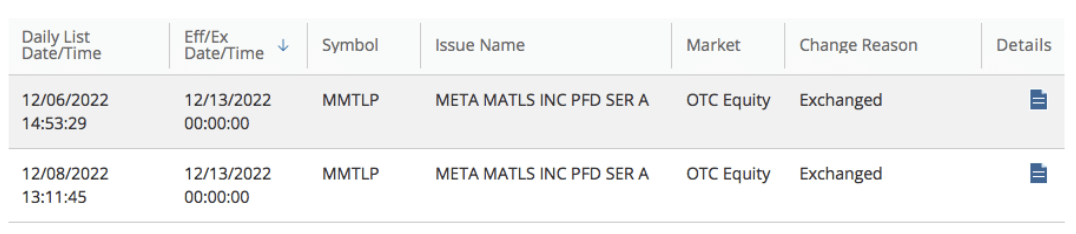

MMTLP entered the picture as the “preferred stock dividend, payable immediately prior to the closing of the Transaction, that entitles them to their pro rata share of any proceeds resulting from any sale of Torchlight’s oil and gas assets” referenced above. It began trading on October 6, 2021, according to FINRA’s Daily List:

It seems not to have been meant to trade at all. Meta did not seek to have it listed on the Nasdaq. The Financial Industry Regulatory Authority later said that a single market maker had asked that it be given a ticker because he had an unsolicited order from a customer. FINRA didn’t find the request unusual and assigned “MMTLP” to the stock. Almost immediately, it began to trade regularly. It did not, however, go crazy. For the next year, it moved between $1 and $2 on low volume, usually trading a few hundred thousand shares each session. Days with volume in excess of one million were rare.

Nothing much happened until early October 2022, when it broke out of its pattern on somewhat higher volume to higher prices. By the end of the month, it was trading above $6, hitting a historic high of $11.65 on November 21.

December 2022: Disaster Strikes

Somewhere along the line, a fairly small number of traders bewitched by dreams of enormous, zip code-changing short squeezes became aware of MMTLP. For reasons not clear to us, they became convinced the preferred had been excessively shorted, and probably shorted naked. In reality there was never enough volume to suggest that any kind of shorts were seriously interested. Yes, the volume created by naked shorting does show on the tape, if it’s present. And although activist short Kerrisdale Capital published a research report critical of MMAT, it did not address the question of MMTLP’s sudden appearance in the marketplace.

Information about MMTLP and its eventual successor was out there for those willing to poke around in the SEC filings. On July 15, 2022, a Nevada company called Next Bridge Hydrocarbons, Inc. filed an S-1 registration statement with the SEC. The filing was directed to holders of MMAT’s Series A preferred; that is, MMTLP shares:

This prospectus (“Prospectus”) is being furnished to you as a Series A Preferred stockholder of Meta Materials, Inc. (“Meta”) in connection with the planned distribution (the “Spin-Off” or the “Distribution”) by Meta to its Series A Preferred stockholders of all the shares of common stock, par value $0.0001 per share (the “Common Stock”), of Next Bridge Hydrocarbons, Inc. (the “Company,” “Next Bridge,” “we,” “us” or “our”) held by Meta immediately prior to the Spin-Off. As of immediately prior to the time of the Distribution, Meta holds 165,523,363 shares of Common Stock, which is 100% of the outstanding shares of capital stock of the Company.

Each share of MMTLP would entitle its holder to one share of Next Bridge stock. It is carefully noted in the Next Bridge S-1 registration statement, however, that “Meta currently owns all the outstanding shares of Common Stock of the Company [Next Bridge], and we have not sought to have the shares of Common Stock traded on any exchange. Accordingly, there is currently no public market for the Common Stock, and there is no current expectation for a public market to develop for the Common Stock.” Next Bridge’s securities would not be publicly traded for the foreseeable future. It should be noted that even though Next Bridge shares are not trading publicly, it submits filings and reports with the SEC which are publicly available.

The prospectus further specifies that “[y]ou will not be required to make any payment, surrender or exchange your shares of Series A Preferred Stock or take any other action to receive your shares of our Common Stock, although your shares of Series A Preferred Stock will be cancelled as of the Record Date.”

Shareholders should have known what was coming, though a firm date for it had not been set: they’d lose their preferred shares and receive an equal number of shares in a company whose securities are not publicly traded. The preferred stock would be cancelled.

FINRA, as it is supposed to do, filed notice of the corporate action—the exchange of MMTLP for Next Bridge stock—on December 6, 2022. It then slightly altered the accompanying note on December 8 and posted that notice as well:

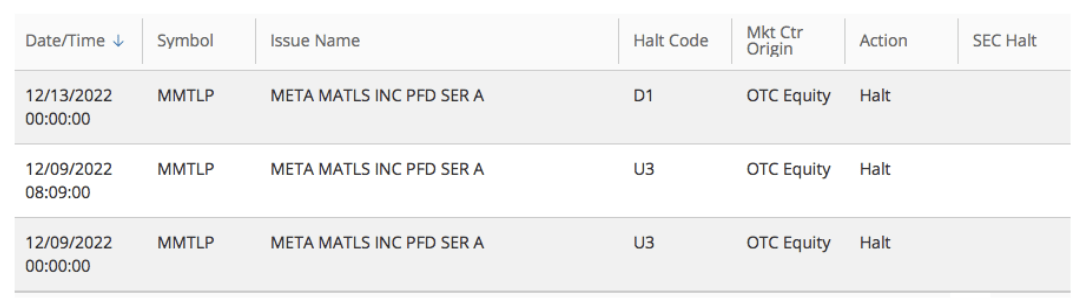

The new note read: “See Daily List of 12/6/2022. Announcement Revised: MMTLP shareholders with settled positions as of 12/12/22 will receive one (1) share of Next Bridge Hydrocarbons, Inc. for every one (1) share of MMTLP held. Purchases of MMTLP executed after 12/8/22 will not receive the distribution. Will not be quoted Ex. Symbol: MMTLP will be deleted effective 12/13/22.” On the next day, December 9, FINRA shut down MMTLP with a U3 trading halt.

A U3 halt is described by FINRA in dramatic terms: “Trading is halted because NASD [now FINRA] has determined that an extraordinary event has occurred or is ongoing that has had a material effect on the market for the OTC Equity Security or has caused or has the potential to cause major disruption to the marketplace and/or significant uncertainty in the settlement and clearance process.” The final notice, from December 13, bears the code “D1,” which informs readers of the stock symbol’s deletion.

What’s important about FINRA’s explanation is that the regulator had deemed that there might be problems with settlement and clearing of stock sold too close to the Monday close, when the MMTLP stock was to be cancelled. Unfortunately, shareholders did not and do not wish to understand that. They were and are convinced Shorty—no doubt working with the help of FINRA—is to blame for their misfortune. They’re now convinced they had the right to trade MMTLP on that Friday and Monday and that the resulting MOASS (“Mother of All Short Squeezes” would show Shorty who was boss. Never mind that even on the final Thursday, there wasn’t enough volume—15,993,578 shares—to account for anything more than hopeful retail buyers.

FINRA Responds

In social media, the SEC and FINRA were accused of manipulating MMTLP, which was seen as a signifier of the corruption of government agencies. (FINRA is not a government agency, but many believe it is.) Shareholders—now shareholders in the non-trading Next Bridge—filed a FOIA request and learned that employees of FINRA and the SEC communicate with each other, and found it to be shocking proof of the extent of their grift.

Finally, on March 16, 2023, FINRA published a FAQ about the corporate action and trading halt, saying with great restraint that it had “received a number of questions” about the matter. The FAQ is well worth reading. The regulator’s explanation of events, and of its own decisions, are sane and convincing. We learn, among other things, about how the MMTLP trading symbol came to be assigned: it was done “upon request by a broker-dealer to facilitate electronic reporting of an executed transaction in the security.” FINRA then explains why it wasn’t necessary for the market maker to file a Form 211.

It confirms that short interest in MMTLP was insignificant. Of relevance for those who improbably insist that a billion or more shares were sold short, “while the total short sale volume for transactions in MMTLP that settled from November 16, 2022, through November 30, 2022, was 7,413,679 shares, the published short interest for MMTLP on settlement date November 30, 2022, was 4,658,068 shares.” The regulator also distinguishes between short interest and short volume, as it has done at greater length on its website.

Cromwell Coulson, head of OTC Markets Group, struck the same note in a series of messages he wrote at X in early February. A point he stressed was:

If there are any remaining short positions, they’re in Next Bridge now; nothing needs to be done about them unless Next Bridge becomes a public company someday. FINRA makes one more very important point, almost casually, saying it’s “considering how it might enhance the usefulness of the short interest information available to investors, which could include changes to the content and frequency of the short interest reporting.” Many market participants have been hoping it would do just that for years.

None of that offers any satisfaction to former MMTLP longs. They’re calling and writing to Congress in the hope of seeing Gary Gensler, SEC chair, and Robert W. Cook, CEO of FINRA, called to account. But as Coulson says, the real problem is that most of the social media gurus don’t know much about market mechanics.

What About the Wells Notices?

As we’ve seen, the Wells notices sent to the company, Brda, and Palikaras stem from an investigation that began in 2021 and had to do with, “among other things,” the merger between Torchlight and Metamaterials Inc.

Around the same time, the Commission was investigating eight social media influencers, all of them active at Twitter and Discord, touting and manipulating exchange-listed stocks. It filed suit on December 14, 2022; we wrote about it at the time. The complaint reveals that Torchlight and MMAT were among the stocks the influencers pumped:

In the course of the scheme, various Defendants often highlighted an anticipated event that would purportedly raise the stock price (a “catalyst”) and encouraged buying and holding the stock until the event, falsely claiming that they too were holding the stock waiting for the catalyst. In the case of TRCH, the catalyst was a purported upcoming merger with another company, Metamaterial Inc. Hennessey claimed that he had discovered that this merger was coming in the course of his due diligence (“dd”) research on the company. Hennessey repeatedly promoted false information about Meta itself (e.g., that it was worth “north of $4.8 billion”) and promoted the purported benefits of the merger. Hennessey also posted about other purported long-term benefits to TRCH stock holders, including a “dividend” that TRCH shareholders would purportedly receive after the merger. Hennessey also claimed that Meta was potentially partnering with Tesla, and that Meta had products that had applications for fighting COVID-19 and thus a “10 billion dollar MARKET CAP POTENTIAL.”

[Emphasis ours.]

Could there be a connection between the two investigations? It seems possible. The Wells notices make clear the SEC’s Enforcement Division has substantially concluded its investigation and believes litigation is indicated. Meta Materials may have other problems as well. Since February, it’s been trading below a dollar. That could result in the threat of delisting by Nasdaq.

In March, Palikaros assured his shareholders that he wouldn’t need to do a split. But his board of directors disavowed his statement in an SEC filing.

There could be more trouble ahead.

To speak with a Securities Attorney about penny stock bars, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected]. This securities law blog post is provided as a general informational service to clients and friends of Hamilton & Associates Law Group and should not be construed as and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship. Please note that the prior results discussed herein do not guarantee similar outcomes.

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com