Once a company decides to go public, what it says — and where, when, and to whom it says it — comes under a set of federal securities rules that many executives find counterintuitive. The instinct to build excitement ahead of a debut is exactly the instinct these rules are designed to restrain.

This guide explains why the limits exist, what you can and cannot do, the narrow exceptions the rules provide, and the housekeeping that keeps a team out of trouble. It is a roadmap, not a substitute for the case-by-case judgment of your deal counsel, who should be looped in early and consulted before anything close to the line goes out the door.

Why Your Words Suddenly Matter So Much

The governing principle comes from Section 5 of the Securities Act of 1933. In plain terms, a company may not make written offers to sell its stock in an IPO until it has a registration statement on file that contains a prospectus with a price range, and it may not actually complete sales until the SEC declares that registration statement effective. The catch is how broadly the SEC reads the word offer. Regulators treat a wide range of statements — including upbeat commentary about how fast the company or its sector is growing — as part of a selling effort. The concern is that such messaging conditions the market, priming investors with optimism before they have the vetted disclosure in the prospectus that lets them weigh the investment on the merits.

Jumping ahead of these limits has a nickname: gun-jumping. Practitioners often think of the offering in three windows — the period before the registration statement is filed, the waiting period between filing and effectiveness, and the period after the offering becomes effective — because what is permissible shifts as you move through them. A stray statement in the wrong window can carry real consequences.

What can go wrong

- Liability for unvetted statements. Comments that never went through the diligence and disclosure process can expose the company to liability if they prove inaccurate or incomplete.

- A forced pause. The SEC can impose a “cooling-off” period that pushes the timetable back, sometimes at an inconvenient moment in the market window.

- A Section 5 violation. An improper offer can amount to a violation of Section 5 itself, which may give purchasers the right to rescind — that is, to unwind their purchases and demand their money back.

When the Restrictions Begin and End

Heightened care should begin no later than the point at which the company engages its underwriters. But the caution starts even earlier in practice: well before that, executives should steer clear of any public comment or chatter about a possible IPO. The moment an offering is so much as mentioned, most of the protective safe harbors discussed later in this guide become unavailable. For that reason, the single most important habit is simply not to discuss the prospective deal in any communication.

This restrained posture — commonly called the quiet period — continues all the way through the closing of the offering and does not fully lift until 25 days after the offering date, the point at which dealers are no longer required to deliver a prospectus with sales of the shares.

The Baseline: Keep Doing Business as Usual

None of this means a company must go silent. Firms are expected to keep running their businesses and may continue to communicate about their products and operations in the ordinary course, consistent with how they have done so historically. The trouble starts when communications change in volume, tone, or content in a way that lines up with the offering. Because the line between routine business communication and improper conditioning rests on a mix of rules, market practice, and judgment, the right move is to bring counsel in early to shape your communications policy. As a working rule, expect that material public communications during the process — press releases, planned interviews, conference appearances — will be cleared by both company and underwriter counsel before they go out, even when everyone expects them to be fine.

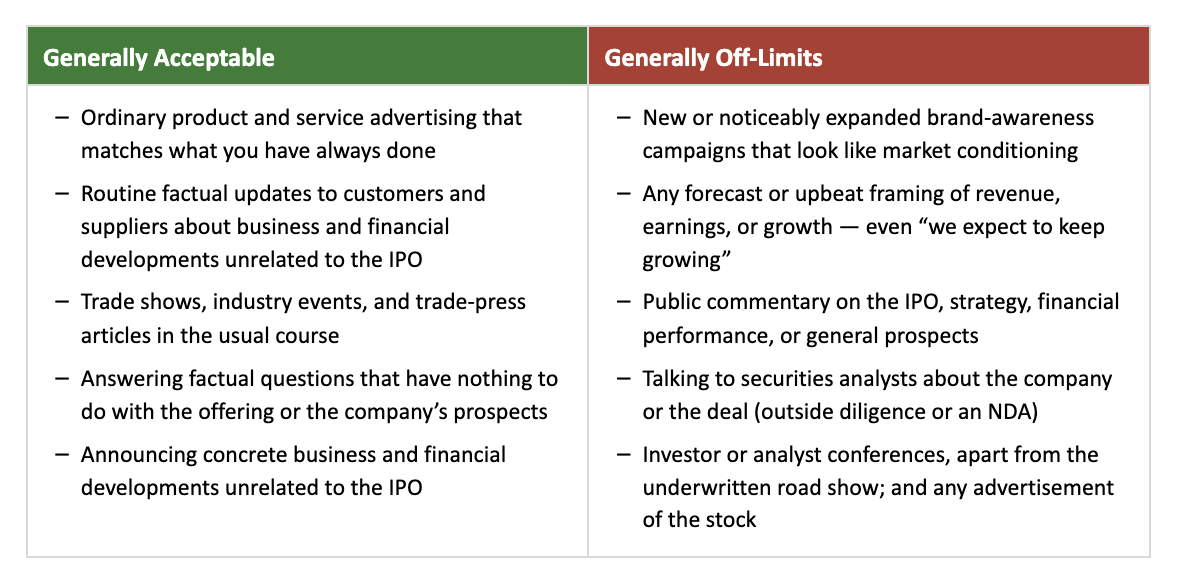

A quick orientation: the two columns

The chart below captures the general shape of the rules. Each item carries the same critical caveat — it must be consistent with the company’s past practice in timing, manner, and content.

One theme is worth underlining because it trips people up: forward-looking optimism is the danger zone. Even a throwaway line like “we expect to continue to grow” is the kind of statement to avoid. Historical fact is far safer ground than any projection.

Digital and Social Media Get No Free Pass

The rules do not care whether a message goes out on letterhead or on a feed. Websites, digital advertising, social posts, and every other online channel are held to the same standard as traditional communications. Treat the company’s entire digital footprint — and the personal posting habits of its people — as part of the same compliance perimeter.

Housekeeping That Keeps You Safe

A handful of straightforward internal policies dramatically reduce the risk of an inadvertent misstep:

- Funnel external contact. Designate one or two senior officers to field all investor and media inquiries, so messaging stays controlled and consistent.

- Stick to facts and routine. Limit communications to factual matters, run the business as usual, and minimize dealings with the press.

- Keep a paper trail. Retain records of press releases, speeches, presentations, and advertising to demonstrate that nothing changed in frequency or substance because of the offering.

- Pre-clear everything outward-facing. Have counsel review public communications before release and approve any interview, speaking slot, or conference appearance in advance.

- Do not ramp up your online presence. Resist the urge to expand the company’s internet footprint during the process.

- Set a posting rule for staff. Adopt a policy barring employees from posting company information online, including on personal accounts, forums, and chat groups.

- Brief the leadership. Make sure directors and senior management, in particular, understand the limits — they are the most likely to be asked, and the most quoted.

- Assume internal notes can leak. Even with security policies in place, internal communications sometimes reach the press; depending on content, a leak can create liability or cause delay.

The Narrow Exceptions

The securities laws do carve out a few situations in which limited communication is permitted. These are genuinely narrow, which limits how useful they are, and each should be relied on only with counsel’s guidance. Here are the ones that come up most often.

Regularly released factual business information (Rule 169)

Rule 169 offers a non-exclusive safe harbor for putting out factual business information. “Factual” is the operative word: the rule covers historical facts about the company, its business or financial developments, and information or advertising about its products and services — but it does not extend to anything forward-looking. To stay inside the harbor, all of the following must hold: the company has a track record of releasing this kind of information in the ordinary course; the timing, manner, and form match its past releases in all material respects; the information is aimed at audiences such as customers and suppliers rather than at investors; and it is put out by the employees or agents who have historically handled such communications. Critically, anything relying on Rule 169 must say nothing about the offering.

Communications more than 30 days before filing (Rule 163A)

Rule 163A creates a safe harbor for most communications made more than 30 days before the registration statement is publicly filed; within that window, they are generally not treated as offers. A few conditions apply: the communication must not reference the IPO; it must come from the company or someone it authorizes (not an underwriter or dealer); and the company must take reasonable steps to keep the communication from being distributed or published during the 30-day run-up to filing. That last point is a classic trap — an interview given comfortably outside the window but published inside it can become a prohibited communication. Note, too, that throughout these rules “filing” means the public filing of the registration statement, not a confidential submission made under the JOBS Act.

Limited-content notices (Rules 134 and 135)

Rules 134 and 135 let a company put out a tightly limited press notice about an offering, but only bare-bones details such as the company’s name and the basic terms of the security. Rule 135 covers a pre-filing notice that the company intends to make a public offering; Rule 134 covers a very limited advertisement after the registration statement is publicly filed. Because the permitted content is so thin, these are seldom used outside special situations — for instance, when a company concludes it needs a notice to flag the offering to customers or suppliers.

Oral offers after filing

Once the registration statement is publicly filed, the company may make oral — as opposed to written — offers. The wrinkle is that the SEC treats almost everything as “written,” including broadcasts, most electronic messages, and broadly distributed or “blast” voicemails. Only genuine real-time speech qualifies as oral: a voicemail left in the course of a live phone call, or a live presentation to an audience, including a live webcast. An on-demand webcast, by contrast, is written. Because the oral category is so confined, companies typically just refrain from making offers of any kind until written offers are allowed.

Written offering materials: the statutory prospectus and FWPs

As the SEC review nears completion and the prospectus is amended to add an estimated price range, that version — the statutory prospectus — can be used to make offers. The company may also use other written materials known as free writing prospectuses (FWPs), but generally only if the statutory prospectus accompanies or has already gone to the recipient. In practice, that means an FWP is hard to distribute broadly except in an electronic form that links directly to the statutory prospectus, or to investors already known to have the latest version. E-mails, faxes, website posts, on-demand webcasts, and blast voicemails are all examples of FWPs.

FWPs usually must be filed with the SEC when used, and because the law treats them as prospectuses, they carry the same liability exposure as the statutory prospectus itself. They are mainly used to push out necessary updates during a road show. Every FWP should be cleared with counsel first — to confirm it carries any required legends, contains nothing it shouldn’t, and is on the underwriters’ radar.

Dealing With the Media

The guiding rule for press contact mirrors the general one: stick to factual business matters handled the way you always have, and never comment on the IPO itself. The FWP framework does provide some shelter from Section 5 problems when a media story results from company participation, but it does not erase the company’s exposure to liability for what the story says. If the company took part — by granting an interview, say — the resulting article can itself be an FWP when published, a so-called media FWP. Unlike an ordinary FWP, a media FWP need not be preceded by a statutory prospectus; but if it qualifies as an FWP, the company generally must file the underlying communication with the SEC unless its substance was already filed. Filed or not, a media FWP is treated as a prospectus, so any material misstatement or omission in it can create liability.

One bright line is worth stating plainly: a company may not pay for, or otherwise solicit, media publicity about the offering, because doing so would trigger an obligation to deliver a statutory prospectus alongside or ahead of the coverage. Since that is rarely workable, the practice should simply be avoided.

Testing the Waters

Since December 3, 2019, any company — not just emerging growth companies — has been permitted to communicate, in writing or orally, with institutions that are qualified institutional buyers or institutional accredited investors, both before and after filing a registration statement. This practice, known as testing the waters, lets a company gauge institutional interest, and it has become a routine part of deal preparation since the concept was first opened to emerging growth companies in 2012. Expect the SEC to ask for copies of any written materials used. Because each underwriting bank runs these activities under its own formal process, coordinate with counsel and the underwriters before any testing-the-waters outreach.

On the Horizon: 2026 SEC Reform Proposals

Everything above reflects the rules in force today, and those rules continue to govern. That said, the framework is under active review, and teams running a process now should keep an eye on a fast-moving reform agenda.

On May 19, 2026, the SEC proposed two sweeping rulemakings — a Registered Offering Reform proposal (Release No. 33-11418) and a companion Filer Status Simplification proposal (Release No. 33-11419) — which the agency has described as the most significant modernization of the registered-offering framework in more than two decades. For communications specifically, the most relevant piece would extend the offering-communication flexibilities now reserved for well-known seasoned issuers (including the pre-filing and free-writing-prospectus accommodations) to a far broader set of companies, with eligibility keyed to being listed on a national exchange rather than to a public-float threshold, through proposed new “eligible listed issuer” categories. The proposals would also, among many other things, broaden access to Form S-3 shelf registration and create an extended IPO “on-ramp.” The public comment periods run into late July 2026, and any final rules — which could differ from the proposals — would not take effect until 2027 at the earliest.

Separately, in late May 2026 the SEC Chairman publicly signaled an appetite to modernize the gun-jumping rules themselves, observing that they have not been meaningfully updated in over twenty years and no longer reflect how companies actually communicate. As of this writing, that is a stated intention rather than a proposed rule, so it changes nothing today — but it suggests the communications landscape described in this guide may look different in coming years. Confirm the current state of play with counsel before relying on any anticipated change.

The Bottom Line

The quiet period is manageable. With early planning and counsel’s input, a company can keep talking to its customers, suppliers, and other constituents in a way that does not meaningfully hamper its business or its sales and marketing — all while avoiding any added risk to the offering. When in doubt about a particular communication, the safest path is the simplest: pause and ask counsel before it goes out.

This blog post is for general educational purposes only. It is not legal advice and does not create an attorney-client relationship. IPO communications rules are fact-specific and should be reviewed with securities counsel before any offering-related communication is made or distributed.

Hamilton & Associates Law Group, P.A. assists issuers with Form S-1 registration statements, SEC comments, going-public transactions, Nasdaq and NYSE listings, OTC Markets matters, direct public offerings, resale registrations and ongoing public-company compliance. Companies considering a registered offering should begin planning well before the desired filing date so audit, disclosure, governance and market-entry issues can be addressed before they delay the transaction.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected].

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com