SEC Charges Unregistered Brokers, Jeffrey K. Galvani and Stuart A. Jeffery, for Facilitating $1.2 Billion in Penny Stock Trades

On November 17, 2022, the Securities and Exchange Commission (the “SEC”) charged Jeffrey K. Galvani, Stuart A. Jeffery, and two New York-based entities they controlled with operating as unregistered broker-dealers that facilitated more than $1.2 billion of securities trading, primarily in penny stocks.

The SEC’s complaint alleges that Galvani and Jeffery – both registered brokers at a registered broker-dealer unconnected with this case (Crito Capital LLC, according to FINRA Broker Search) – created GEL Direct Trust, which they managed through its trustee, GEL Direct, LLC.

The GEL entities were not registered with the SEC as broker-dealers. Nonetheless, from 2019 through at least May 2022, Galvani and Jeffery, acting through the GEL entities, executed more than 19,000 trades of more than 300 billion shares of stock of more than 400 issuers (primarily penny stocks) on behalf of approximately 60 customers.

Trades facilitated by GEL generated more than $1.2 billion of trading proceeds for its customers, from which the defendants allegedly received at least $12 million in transaction-based and other compensation.

According to the complaint, the vast majority of GEL’s trading activity related to “the sale of penny stocks that its customers obtained through the acquisition of convertible promissory notes or other forms of microcap financing” — the type of transactions typically linked to toxic lenders that many legitimate brokers might shy away from.

Our records show that one of those customers was Charlie Abujudeh, who was charged by the SEC in July 2021 for fraudulently selling stock in several microcap companies to investors by making misleading statements during high-pressure sales calls and/or email promotions. Abudjudeh was also criminally charged.

The brokerage services GEL allegedly provided included taking possession of customer securities, directing trades to executing brokers, facilitating trade settlements, and disbursing trading proceeds to customers.

The GEL Business Model worked as follows:

- Every new GEL customer was required to fill out an “Account Application” that, among other things, confirmed that GEL would have trading authorization over the customer’s securities.

- Several GEL customers also provided their own documents to GEL confirming their understanding that they were opening a “brokerage account” with GEL and that GEL would provide broker-dealer services.

- After enrolling a new customer, GEL sent a “Welcome Packet” that:

- Listed Galvani and Jeffery as GEL’s Managing Partners;

- Stated that customers would use “the following form to authorize the transfer of assets, currently at another firm, to your brokerage account held at GEL”;

- Provided a “Deposit Checklist” that included general requirements to ensure that customers could transfer their securities to GEL; and

- Required customers to set up an account for GEL to wire their trading proceeds.

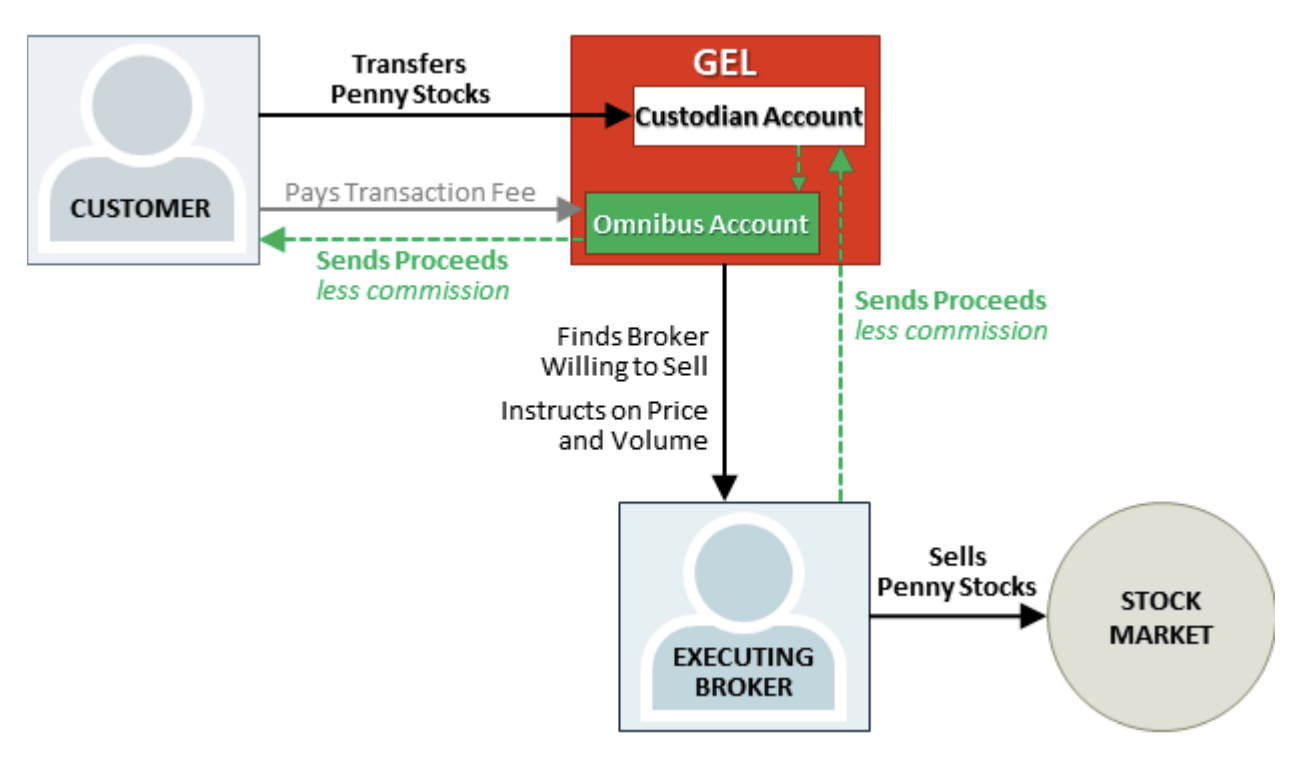

- GEL established omnibus accounts in its name to hold its customer’s trading proceeds and GEL’s fees. Initially, the GEL omnibus accounts were maintained at a trust company, and later at the financial institutions maintaining the custodian accounts described in the following paragraph.

- GEL established custodian accounts in its name at several financial institutions. GEL’s customers, following GEL’s instructions, used electronic transfers to deposit their penny stocks and other securities into the custodian accounts, thereby giving GEL control over the handling and disposition of its customers’ securities.

- GEL further established approximately 20 delivery-versus-payment (“DVP’) brokerage accounts at domestic and offshore brokerage firms. GEL used these DVP brokerage accounts to place trades to sell its customers’ securities.

- GEL found executing brokers who were willing to sell the securities in the market through one of GEL’s DVP brokerage accounts.

- GEL provided trading instructions on behalf of its customers to the executing brokers and directed the executing brokers to sell the securities (these instructions often included directives on price and volume).

- The executing broker then sold the securities based on GEL instructions, typically by placing trades in the U.S. over-the-counter market. After an executing broker sold the securities through one of GEL’s DVP brokerage accounts, the funds settled at one of GEL’s custodian accounts.

- Typically, GEL would transfer the settled funds from the custodian account to a GEL omnibus account.

- GEL then allocated trading proceeds to the omnibus subaccount associated with the customer.

- After GEL directed the funds to the subaccount, GEL followed instructions from its customers for wiring the trading proceeds to the customers’ bank accounts. GEL wired hundreds of millions of dollars in customer trading proceeds to customer bank accounts or to third-party bank accounts on behalf of its customers.

The SEC’s complaint provides the following graphic illustrating a typical transaction:

GEL received multiple types of compensation from its customers, including transaction-based compensation.

- GEL charged each customer a $2,500 monthly account maintenance fee.

- GEL charged its customers a transaction-based fee for each deposit of securities the customer made with GEL for GEL to sell through the executing brokers. The fee was $1,100 per deposit in most instances but varied depending on the type of securities deposited.

- GEL charged a $30 trade-settlement fee each time it completed a trade on behalf of a customer.

- GEL charged rush fees to expedite the review and trading process, and other fees related to brokerage-type services such as a: (i) $150 termination fee, (ii) $35 wire transfer fee, (iii) $250 alternative asset fee, and (iv) $75 Roth conversion fee.

Each month, GEL collected these fees from its customers, which account documents referred to as “commissions.” Between June 2019 and May 2022, GEL received more than $12.4 million dollars in fees from its customers. The fees were paid out to Galvani’s and Jeffery’s personal accounts (at a 50-50 split) from fees deposited in the GEL, GEL Trustee, and other controlled accounts.

The SEC’s complaint, filed in the U.S. District Court for the Southern District of New York, charges Galvani, Jeffery, GEL Direct Trust, and GEL Direct, LLC with violating the broker-dealer registration requirement of Section 15(a) of the Securities Exchange Act of 1934 and charges Galvani and Jeffery as “control persons” of the GEL entities under Section 20(a) of the Exchange Act. The SEC seeks permanent injunctions, disgorgement, prejudgment interest, civil penalties, and penny stock bars against all defendants.

To speak with a Securities Attorney, please contact Brenda Hamilton at 200 E Palmetto Rd, Suite 103, Boca Raton, Florida, (561) 416-8956, or by email at [email protected]. This securities law blog post is provided as a general informational service to clients and friends of Hamilton & Associates Law Group and should not be construed as and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship. Please note that the prior results discussed herein do not guarantee similar outcomes.

Hamilton & Associates | Securities Attorneys

Brenda Hamilton, Securities Attorney

200 E Palmetto Rd, Suite 103

Boca Raton, Florida 33432

Telephone: (561) 416-8956

Facsimile: (561) 416-2855

www.SecuritiesLawyer101.com