When Denying Rule 144 Legal Opinions is a Market Manipulation Scheme

Practical guidance on Rule 144 legal opinions, restrictive legend removal, and transfer agent processing, including shell company and 144 legal opinion considerations.

Read More

The “Genius” Plan: Penny Stock Insiders vs. Section 5 (Guess Who Wins)

Officers, directors, and other insiders try to “control” the flow of public sales - sometimes under the banner of Rule 144 -…

Read More

Officers and Directors of Foreign Private Issuers Now Subject to Section 16 Reporting Requirements

Section 16(a) reporting requirements to directors and executive officers of foreign private issuers marks a significant evolution in U.S. securities regulation. The…

Read More

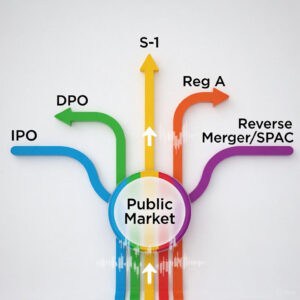

Nasdaq Primary vs. Secondary Direct Listings

A Nasdaq direct listing allows an issuer to list its common equity on the exchange without the traditional underwritten initial public offering…

Read More

Reverse Merger to Go Public: Legal & Regulatory Risks

A reverse merger can be a viable path for a private company to gain a public listing, offering speed, cost efficiency, and…

Read More

Supreme Court Petition in Xeriant v. Auctus Fund: A Defining Moment in the SEC’s War on Toxic Lenders

This article details the Supreme Court petition in Xeriant, Inc. v. Auctus Fund, LLC, which challenges a Second Circuit opinion regarding Section…

Read More

OTC Markets’ Role in Secondary Offerings and Resales

The critical role of OTC Markets in facilitating secondary offerings and resales of restricted and control securities under SEC Rule 144. This…

Read More

Nasdaq Annual Meeting Rules: Q&A Guide

This question-and-answer guide covers the legal and regulatory requirements for Nasdaq-listed companies holding their annual stockholder meetings. The article focuses on the…

Read More